You might think that the most obvious of these implications is that stock markets are inefficient so it should be easy to find underpriced shares. Even if the premise is correct, however, the inference doesn't follow. The thing about irrationality and bounded knowledge is that they afflict all of us. The belief that others are stupid and we are not is an example of the most ubiquitous of cognitive biases: overconfidence.

Instead, I suspect there's a different reason for investors to take incompetence seriously: it means we shouldn't put our faith in company bosses.

Consider two longstanding anomalies. One is that, as Harvard University's John Campbell has shown, companies that are in financial distress tend to deliver bad subsequent returns. This is odd. The risk of a company going bust is a big and partly systematic one - it is greater in an economic downturn when our other assets are doing badly - and investors should be rewarded for taking this risk. But they are not.

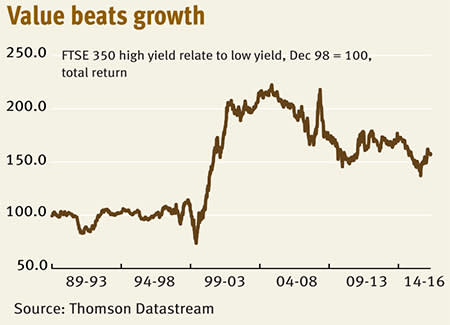

The other anomaly is that growth stocks underperform. In the last 20 years, the FTSE 350 low-yield index has underperformed its high-yield counterpart, delivering total returns of 5.2 per cent per year, compared with the ones of 7.8 per cent. This is especially weird because long-term interest rates have collapsed during this time, and this should have boosted growth stocks by reducing the discount rate applied to future cash flows.

These anomalies might be related. Both are consistent with the possibility that investors overestimate management skill and so pay too much for it. They overestimate the ability of bosses to turn around failing companies. And they overestimate their ability to expand companies in the face of what are often considerable diseconomies of scale. The upshot is that investors pay too much for such companies.

In fact, we have other evidence that investors overestimate management competence. Researchers at MSCI and at the University of Utah have found that high chief executive pay is associated with worse equity returns. This is also consistent with people overestimating bosses' ability and so paying too much for it.

Psychologists have a phrase for this. They call it the fundamental attribution error - our tendency to attach too much importance to individual personalities and pay too little attention to environmental or structural factors.

This might sound iconoclastic. But it's not. I'm just repeating the thoughts of wiser men. The late Peter Drucker, one of the most influential of all management scientists, said: "No institution can possibly survive if it needs geniuses or supermen to manage it." And Warren Buffett has said that a good business is one that could be safely run by your idiot nephew.

But what sort of business is that? It's one that has what Mr Buffett has called a "moat" - something that protects the business from competition and gives it a degree of monopoly power. This might be big powerful brands such as Coca-Cola, Unilever or Diageo. Or it might be high capital requirements, which utilities and big oil stocks have.

Such quasi-monopoly power gives managers less to worry about and so reduces their chances of screwing things up. Yes, strong companies can be brought down by really bad decisions, which are often large takeovers: think of RBS and GEC. But if a business is well-established, it can be run by your idiot nephew - at least if he is lazy enough not to want to make a big change.

The companies of which this is true are generally defensives; they have size, brand power and well-established routines that allow them to survive averagely incompetent management. Because investors have tended to under-rate the importance of these structures, they have paid too little for defensive stocks down the years, which is one reason why they have generally done so well.

Perhaps, therefore, several stock market anomalies - the underperformance of distressed and growth stocks and outperformance of defensives - all have their root in investors overrating management skill and underrating good structures. The "great man" theory isn't only dubious history, it's also a poor basis for an investment strategy.