KCOM (KCOM) has committed itself to annual dividend growth of 10 per cent to March 2016, which means investors can expect a 6.9 per cent yield from the stock next year supported by the strong cash flows from its mature telecoms business. Meanwhile, management is looking to address issues at the group's racier managed services operation in order to unleash its growth potential.

- Large forecast yield

- Strong cash generation

- Exposed to ‘big data’ trend

- Shares are cheaply rated

- Growth remains sluggish

- Stretched dividend cover

We feel KCOM offers an enticing combination of businesses. Its KC division is a mature, highly cash-generative telco centred in Hull and East Yorkshire. It accounts for about 30 per cent of group revenues but 70 per cent of cash profits, and delivered a first-half cash-profit margin of 54 per cent. Meanwhile, the KCOM division is a national managed-services provider that offers communications, hosting, cloud-based and consulting services. While issues with KCOM's legacy 'voice' business have been holding back this division's overall performance, it is tapping into soaring demand for data and connectivity, giving it excellent long-term growth potential.

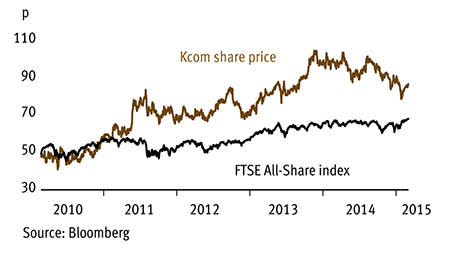

The upshot of this combination of operations has been steady profits and healthy margins. Adjusted operating profit rose 4.4 per cent to £28.5m in the six months to the end of September, and the group's cash-profit margin widened from 20.2 per cent to 20.9 per cent. Nevertheless, KCOM's shares trade at just 11 times broker finnCap's forecast EPS for the year to the end of March 2016. That's a sharp discount to its telecom peers. They also offer a lofty 6.4 per cent forecast yield, rising to 6.9 per cent in 2016, based on management's dividend-growth commitment.

The KC division looks stable and stands to benefit from the rapid roll-out of high-speed fibre broadband. It expects to reach 45,000 homes and businesses by the end of March. Customer adoption is already ahead of the national average, spurring a £5 rise in monthly average revenue per user.

Meanwhile, buoyant demand for Kcom's bundled telecoms products, broadband and fibre is starting to offset falling demand for voice services. The division recently inked a five-year deal with HM Revenue & Customs to implement web chat and cloud services at one of the UK’s largest call centres, spanning 8,000 advisers across 16 sites.

KCOM's strategy has centred on rapidly diversifying and differentiating its offerings. For instance, KCOM now offers a suite of consultancy, hosting, implementation and maintenance services, and specialises in highly complex projects. However, a declining legacy 'voice' business has taken the shine off some of this progress. The group is investing heavily to accelerate growth, though, and first-half capital spending rose 59 per cent to over £21m as it expanded its fibre network, upgraded its IT systems and targeted specific customers. KCOM's net debt should not be a worry, as it is currently around the £100m target mark. And a £200m credit facility through to June 2019 should secure funding and provide firepower for organic investments and acquisitions.

| KCOM (KCOM) | ||||

|---|---|---|---|---|

| ORD PRICE: | 85p | MARKET VALUE: | £439m | |

| TOUCH: | 85-86p | 12-MONTH HIGH: | 106p | LOW: 79p |

| FORWARD DIVIDEND YIELD: | 6.9% | FORWARD PE RATIO: | 11 | |

| NET ASSET VALUE: | 15p* | NET DEBT: | 130% | |

| Year to 31 Mar | Turnover (£m) | Pre-tax profit (£m)** | Earnings per share (p)** | Dividend per share (p) |

|---|---|---|---|---|

| 2012 | 387 | 51.1 | 7.1 | 4.0 |

| 2013 | 373 | 50.0 | 7.7 | 4.4 |

| 2014 | 371 | 49.9 | 7.5 | 4.9 |

| 2015** | 342 | 51.8 | 8.0 | 5.4 |

| 2016** | 343 | 49.9 | 7.7 | 5.9 |

| % change | +0 | -4 | -4 | +9 |

**finnCap forecasts, adjusted PTP and EPS figures Normal market size: 5,000 Matched bargain trading Beta: 0.24 *Includes intangible assets of £116m, or 22p a share | ||||