Before the credit crunch, property prices in 'grotty' inner London were catching up with prices in the capital's core and investors raved about 'convergence'. Since the crunch, investors have cared only for quality, and property prices in central London have soared clear of prices in the rest of the city.

- New Hong Kong equity partner

- Greenwich development could be kick-started

- Shares trade far below book value

- Focus on London residential

- Opaque valuations

- Big debt pile

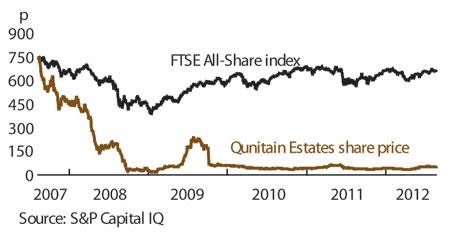

The company to suffer most from this abrupt reversal is Quintain (QED), which owns two of London's largest regeneration sites, around the Millennium Dome in north Greenwich and beside Wembley Stadium in north-west London. It found itself cut off from the capital markets and, with limited cash flow to finance its ambitious schemes, has been living a hand-to-mouth existence.

But that looks set to change. The share price has risen by nearly two-thirds since its June lows, thanks largely to a turn in Quintain's fortunes. On 18 June, it announced a joint venture to redevelop Greenwich peninsula with a Hong Kong company, Knight Dragon. The name implies a curious ambivalence, but the joint venture, Quintain Knight Dragon - which is headed by Dr Henry Cheng Kar-Shun, chairman of New World Development, a listed conglomerate with a market capitalisation of about £6.4bn - looks more white knight than fiery dragon.

Yes, the UK developer is giving up much of its equity in Greenwich. Yet, in exchange, it has secured not just cash and management fees it can redeploy at Wembley, but - crucially - £300m in development finance for Greenwich. The peninsula's long-stalled regeneration can now finally move forward.

QUINTAIN ESTATES & DEVELOPMENT (QED) | ||||

|---|---|---|---|---|

| ORD PRICE: | 57p | MARKET VALUE: | £277m | |

| TOUCH: | 56.5-57p | 12-MONTHHIGH: | 57p | LOW: 33p |

| DIVIDEND YIELD: | nil | TRADING PROPERTIES: | £21.3m | |

| DISCOUNT TO NAV: | 46% | |||

| INVESTMENT PROPERTIES: | £1.10bn | NET DEBT: | 94% | |

| Year to 31 Mar | Net asset value (p) | Pre-tax profit (£m) | Earnings per share (p) | Dividend per share (p) |

|---|---|---|---|---|

| 2009 | 121 | -129.1 | -39.1 | nil |

| 2010 | 120 | -10.2 | -3.3 | nil |

| 2011 | 116 | -48.1 | -6.7 | nil |

| 2012 | 110 | -43.5 | -6.8 | nil |

| 2013* | 106 | -29.5 | -4.1 | nil |

| % change | -4% | - | - | - |

Normal market size: 6,000 Matched bargain trading Beta: 1.0 *Peel Hunt estimates | ||||

Another advantage of the deal is that it validates Quintain's valuations to a degree. One reason the company's share price still languishes far below book value is that investors don't believe the book. Unlike most developers, Quintain does not hold its projects at cost as 'trading properties', but uses a discounted cash-flow model to revalue them as 'investment properties'.

Keith Crawford, property analyst at broker Peel Hunt, has calculated that the Knight Dragon deal prices the Greenwich assets at a 13 per cent discount to Quintain's holding value. Using a 2010 sale to Brent Council to write down the development land at Wembley along similar lines, he comes up with a 91p "floor" to Quintain's net asset value (NAV). That's 19 per cent below the adjusted NAV of 112p that Quintain reported for March, but also implies that the shares trade at a 37 per cent discount.

That gap looks too wide now that Quintain has more cash to spend at both Greenwich and Wembley, which, as residential-led schemes in well-connected London locations, have enormous potential. Residential land values have risen strongly in London and show no sign of stopping. The government is desperate to 'get Britain building', so local authorities may be willing to cut their demand for affordable homes, which has proved a major obstacle in Greenwich. Dr Cheng clearly believes in the opportunity.