The main fear among investors right now concerns America’s fiscal cliff, the combination of automatic tax rises and spending cuts that threatens to plunge the US economy into recession in 2013. While the issues are beyond the remit of this column, I do expect Washington's feuding politicians to reach a compromise and avoid this dreadful outcome. But there is clear potential for equity wobbles meanwhile.

FTSE revival

I have been impressed with how effectively the indices have been scaling the cliff-face in recent days. The main US indices, as well as the FTSE and DAX have continued the rally that got underway on Monday 19 November, in line with my daily recommendations. From trough to peak, the Nasdaq 100 has gained as much as 6.6 per cent, while the FTSE had added 4 per cent at its best.

The Nasdaq's progress had got me especially excited. I always like to see the technology-heavy index at the forefront of moves upwards in the markets. It's a sign of healthy risk-appetite on the part of buyers, and therefore sustainability. By twice opening above the highs of the previous day, it formed two 'gaps' on its daily chart, a common feature of early-stage rallies in this index.

S&P hits a wall

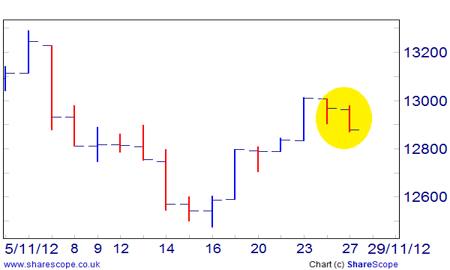

However, the indices have since shown signs of stalling and then reversing. The S&P 500 has so far proven unable to break decisively beyond its 55-day exponential moving average, one of the key lines that I use to determine the medium-term trend. On Tuesday 27 November, the Dow gave a repeat sell-signal on its swing-chart, with the S&P and Nasdaq following suit the next day.

Dow sell-signal

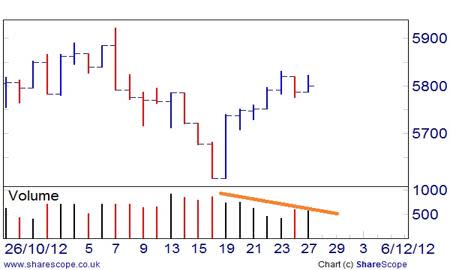

Today's wall of worry also contains technical bricks. Disbelievers among my fellow chartists have highlighted the lack of volume accompanying the move off the lows. As I pointed out last week, the S&P's initial jump saw fairly few shares changing hands, and the situation deteriorated thereafter. Only on down-days have volumes really picked up.

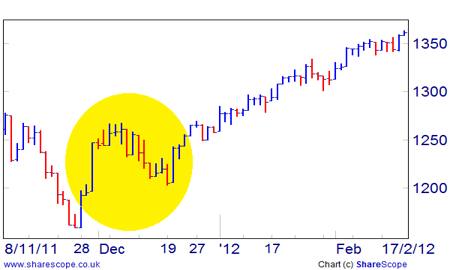

Perhaps we are due a repeat of the sort of action that we saw roughly this time last year. After an initial rally off the early November lows, the indices went downwards and sideways, before the traditional end-of-year rally kicked in. The trigger for that rally was the European Central Bank's liquidity splurge. This year, I reckon the trigger could come from a resolution of the 'fiscal cliff' issue.

2011 all over again?

Speaking of seasonal trading, it is important to remember that the end-of-year rally tends to be exactly that, rather than something that begins as soon as the first office parties take place. On average, the S&P has often weakened in the middle 10 days of December, before spurting higher in the Christmas week and into the New Year.

While it is slightly disappointing that the latest rally has wobbled so early, I am certainly not giving up on the case for a strong end to the year and a decent start to 2013. Reaching new bull-market highs on the S&P, FTSE and other indices may now be a tall order in 2012. But I've every confidence we’ll see them in early 2013.