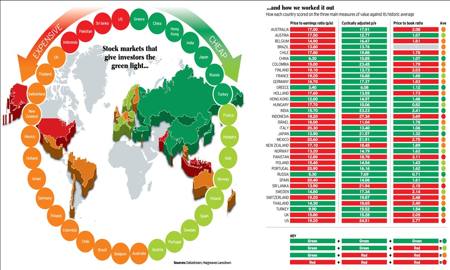

What is the best way of finding out which national equity indices offer good value? I ask this having seen the eye-catching graphic below from Hargreaves Lansdown, a British brokerage firm. It shows the valuations of almost three dozen developed and emerging stock markets from around the world. Each market is colour-coded according to its relationship to its past price/earnings ratio, its ten-year cyclically-adjusted price/earnings ratio (CAPE) and its price/book ratio (PB).

Hargreaves' world view

Based on these criteria, Hargreaves says that China, Greece, Hong Kong, India, Japan, Russia and Turkey are looking cheap right now. By contrast, it reckons that Indonesia, Pakistan, Sri Lanka, and the US look dear. But is comparing national indices’ present valuations to their past valuations really the most meaningful way of making this call?

The reason that I have my doubts here is because of some of the messages given out by Hargreaves’ chart. Based on its cyclically adjusted price/earnings ratio of 21.57, Japan is said to be cheap. Three emerging markets - Columbia, India and Mexico – have even higher CAPEs than this, and yet are also rated as being cheap. At the same time, Israel is flashes up as being expensive based on its CAPE of 11.0, along with Pakistan on 18.8.

There is at least one obvious pitfall in this approach. Comparing today’s valuations with the past is likely to be misleading if the past was distorted. In the case of Japan, for example, today’s CAPE valuation is plainly much more modest than it was in the past. However, the data set is skewed by the enormous bubble of the 1980s, which took CAPE up to an eye-watering 84.5. It then took some two decades for this to drop below 30, a level that is still very high compared to other markets.

It’s a similar story when we turn to the price/book ratio. Indian equities are valued at 2.41 times the net asset value of the firms behind them, while Dutch equities trade on just 1.73 times. And yet, the former is scored as being cheap, while the latter is rated as being dear. This seems counterintuitive, to say the least. My instinct would be to buy the cheapest markets rather than those that merely look cheap against their own histories.

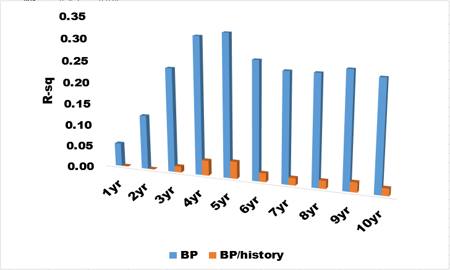

The acid-test here should surely be how effective each metric is at signalling future returns. I have therefore tested the predictive power of the raw level of CAPE and that of CAPE against its own history. The S&P 500 makes an especially suitable guinea-pig here, as we have CAPE data stretching back more than a century. For most other markets around the world, by contrast, CAPE can only be calculated from the early 1980s.

The accompanying table shows how much of the S&P’s real total returns have been explained – in the statistical sense – by the level of CAPE and CAPE compared to its own history. The study covers the period between 1900 and 2004. In every case, the simple level of CAPE had more predictive ability than CAPE compared to its historic average, albeit not dramatically so. The longer the look-ahead period, the more useful CAPE was in foretelling returns.

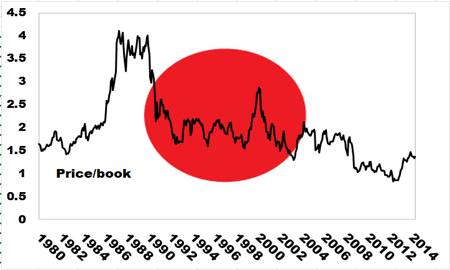

Japan's price/book

I then did the same for the price/book ratio. In this case, I switched my focus to the Japanese market, for which my data-set begins in 1980. The results were even more decisive than for CAPE. The straight price/book explained as much as one-third of subsequent returns over a five-year horizon. Price/book value compared to its own history, meanwhile, was only able to explain around 4 per cent of subsequent returns at best.

Metrics' explanatory power

Datastream

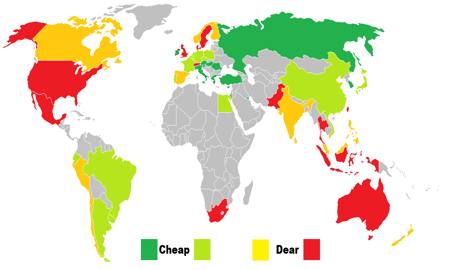

Rather than pick markets based on their valuations today compared to their own histories, my preferred approach is to go for those which are cheap compared to other markets. In the accompanying chart and table, I show world valuation according to three metrics: the dividend yield, price/book value and CAPE. Cheapness is classified according to the combined rankings of each market on all three metrics.

Where in the world to find value

| CAPE | Dividend Yield | Price/book | |

| GREECE | 5.7 | 0.4 | 1.3 |

| CYPRUS | 1.7 | 2.2 | 0.3 |

| KOREA | 13.9 | 1.2 | 1.1 |

| AUSTRIA | 11.6 | 2.8 | 1.1 |

| ITALY | 12.5 | 2.5 | 1.2 |

| TURKEY | 13.1 | 1.8 | 1.6 |

| HUNGARY | 10.1 | 3.6 | 0.9 |

| SINGAPORE | 12.9 | 2.9 | 1.4 |

| RUSSIA | 6.5 | 4.4 | 0.8 |

| IRELAND | 14.1 | 1.0 | 1.8 |

| ROMANIA | 11.7 | 3.5 | 0.9 |

| KUWAIT | 10.6 | 3.2 | 1.6 |

| SLOVENIA | 11.7 | 4.0 | 0.7 |

| ISRAEL | 10.0 | 3.1 | 1.8 |

| NETHERLAND | 13.5 | 2.2 | 1.8 |

| HONG KONG | 13.4 | 2.9 | 1.5 |

| PORTUGAL | 15.0 | 2.8 | 1.6 |

| BRAZIL | 11.6 | 4.1 | 1.4 |

| MALTA | 10.1 | 5.1 | 1.3 |

| EGYPT | 8.8 | 3.4 | 1.9 |

| CHINA | 11.7 | 4.9 | 1.2 |

| ARGENTINA | 13.9 | 1.5 | 2.5 |

| BELGIUM | 15.4 | 2.0 | 1.9 |

| JAPAN | 22.6 | 1.8 | 1.4 |

| POLAND | 13.1 | 3.8 | 1.5 |

| FRANCE | 15.9 | 2.9 | 1.6 |

| CZECH REP. | 10.8 | 5.6 | 1.4 |

| GERMANY | 16.4 | 2.5 | 1.8 |

| SPAIN | 13.8 | 4.0 | 1.7 |

| TAIWAN | 16.6 | 2.8 | 2.1 |

| FINLAND | 13.3 | 3.7 | 2.1 |

| NORWAY | 14.3 | 4.3 | 1.7 |

| PERU | 15.2 | 2.9 | 2.2 |

| SRI LANKA | 17.0 | 2.8 | 2.1 |

| CHILE | 17.2 | 3.2 | 1.7 |

| INDIA | 19.1 | 1.7 | 2.7 |

| CANADA | 19.0 | 2.7 | 2.1 |

| PHILIPPINE | 24.1 | 1.6 | 2.6 |

| NEW ZEALAN | 16.3 | 3.8 | 1.8 |

| MALAYSIA | 17.8 | 2.8 | 2.2 |

| LUXEMBURG | 16.9 | 3.2 | 2.1 |

| DENMARK | 27.8 | 1.7 | 2.7 |

| UK | 17.6 | 3.2 | 2.1 |

| MEXICO | 19.3 | 2.1 | 2.9 |

| AUSTRALIA | 15.6 | 4.3 | 2.1 |

| THAILAND | 16.9 | 3.1 | 2.5 |

| US | 23.4 | 1.9 | 2.9 |

| SWEDEN | 17.3 | 3.5 | 2.1 |

| INDONESIA | 22.2 | 2.3 | 3.7 |

| PAKISTAN | 12.9 | 4.8 | 3.0 |

| SOUTH AFRI | 18.8 | 3.1 | 2.9 |

| SWITZ | 20.2 | 2.9 | 2.6 |

| COLOMBIA | 21.3 | 4.4 | 1.8 |

| VENEZUELA | 25.6 | 4.9 | 3.9 |

Datastream

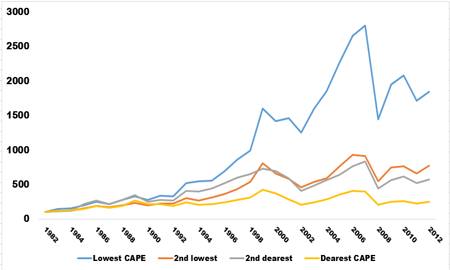

Over time, buying a basket of up to six of the lowest-valued developed equity indices has produced winning returns. The accompanying chart shows the effect of buying into a basket of the cheapest world markets based on CAPE at the start of each year. Since 1982, this approach would have produced an annualised price-only return of 12.1 per cent a year, compared to 8.2 per cent for developed stocks in general.

Datastream

Clearly, then, there is a case for skewing one’s holdings towards cheaper CAPE markets over time. The ongoing dilemma for investors is how to reconcile the good returns implied by low CAPEs in Europe and parts of the emerging world with the poor returns hinted at by the high CAPE of the US market, the largest and most influential of them all. I shall address this in an article before long.