Anthony and Liz are both 62 and retired. They have been investing since 1982 and have accumulated a portfolio worth £1.4m invested across 21 holdings.

Anthony says: "We have seen some ups and downs over that period and tried various investment strategies but nothing works consistently."

The couple are influenced by The Zulu Principle , a book written by English accountant and investor Jim Slater that advises investors to concentrate on an approach, such as buying growth shares or asset situations, or to concentrate on a particular sector. That way, Mr Slater says, you will become relatively expert in your chosen area.

Anthony says: "We are gently moving from relying mostly on numbers to taking more notice of the story. We aim to make a better assessment of the risk than the other people investing in the share we buy. We want to make sure the perceived risks are balanced by potential rewards. We try to avoid price/earnings ratios above 25.

"We keep a proportion of our assets in shares. We tend to gently reduce the total invested in the summer and increase it again in October, although always keeping in mind the October 1987 crash.

"As our portfolio has grown, investing in a relatively small number of shares has meant that each investment has become larger and the value in each shareholding is sometimes worrying. However, we believe that holding too many shares doesn't reduce risk and makes tracking company performance difficult and we believe it is better to accept the risk than not to invest.

"Theoretically we should be investing internationally but there doesn't seem to be any way of identifying markets that are likely to rise faster than London.

"I track the shares daily and investigate any significant daily movements and I spend about three hours a week thinking about stock market investments.

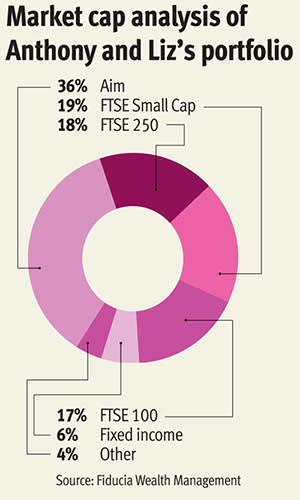

"We aim to beat the FTSE 100 and the FTSE 250 indices on average over the long term. We could consider tracking the portfolio against the Alternative Investment Market (Aim) or the small companies index but it's probably more effort than it's worth.

"Investment performance is our primary goal but the impact of tax, including inheritance tax, does influence our choices so we use self-invested personal pensions (Sipps), individual savings accounts (Isas) and hold some Aim shares. However, we do not do spread betting or hold venture capital trusts (VCTs) or enterprise investment schemes (EISs)."

The couple are thinking of increasing their investment in shares where they hold less than £80,000. They intend to sell the FTSE 100 tracker and increase their investment in momentum shares. They are also interested in investing ethically, avoiding investments in tobacco, fossil fuels and weapons.

Self-invested personal pensions and individual savings accounts

Beat FTSE 100 and FTSE 250 over long term

Anthony and Liz's portfolio

| Holding | Value | % |

|---|---|---|

| BP Marsh & Partners (BPM) | £62,384 | 4 |

| Carillion (CLLN) | £56,222 | 4 |

| Dart Group (DTG) | £143,583 | 10 |

| 4imprint Group (FOUR) | £88,111 | 6 |

| Globo (GBO) | £38,781 | 3 |

| HSBC FTSE 100 UCITS ETF (HUKX) | £92,404 | 7 |

| ITV (ITV) | £76,422 | 5 |

| Marston's (MARS) | £40,414 | 3 |

| NMC Health (NMC) | £107,737 | 8 |

| Optimal Payments (OPAY) | £139,069 | 10 |

| Phoenix Group Holdings (PHNX) | £52,984 | 4 |

| Photo-Me International (PHTM) | £100,232 | 7 |

| Persimmon (PSN) | £79,403 | 6 |

| Redde (REDD) | £59,163 | 4 |

| Trifast (TRI) | £74,930 | 5 |

| Tarsus Group (TRS) | £58,368 | 4 |

| 32Red (TTR) | £48,966 | 3.5 |

| Coventry 6.092% Permanent Interest Bearing Shares (CVB) | £13,210 | 1 |

| Provident Financial 7% Guaranteed Bonds 14/4/2020 (PFG7) | £25,047 | 2 |

| Balfour Beatty Cum Pref shares 10.75% (BBYB) | £23,700 | 2 |

| Nationwide 6% PIBS call 15/12/16 (NANW) | £20,250 | 1.5 |

| TOTAL | £1,401,380 | 100 |

Source: Investors Chronicle as at 9 September 2015

LAST THREE TRADES

Polo Resources (sell), Camkids (sell), Brit Insurance (sell).

YOUR HIGH-RISK APPROACH

Ian Forrest, investment research analyst at The Share Centre says:

In order to beat the FTSE 100 and 250 indices over the longer term, it is usually necessary to invest more in small and medium-sized companies focused on growth, often including some on Aim.

Going for a higher return normally means accepting a higher level of risk. Choosing Aim shares is more risky due to the lower barrier for acceptance on to the market and the lower level of disclosure required. While the story and the numbers are both important I would also recommend scrutiny of the management, since it can have a greater influence on the performance of smaller companies compared to larger ones. It can be quite an exciting ride with some doing very well while others fall away steadily, like Polo Resources (POL) and Camkids (CAMK), for example, so you have to get comfortable with that degree of volatility.

Your strategy is unusual in that generally people who are retired or approaching retirement prefer to lower the risk level in their portfolios as they depend more on their investments for income and do not have the benefit of employment income.

Sticking to a relatively small number of long-term stocks has the benefit that you become very familiar with them, but it does have some downsides. Firstly, it can mean that you have too great a proportion of your portfolio in one stock or sector, which increases the risk level. Secondly, it can mean that you are missing out by not having exposure to other sectors which may be doing better than those you currently hold. I agree that holding a large number of stocks makes tracking their performance difficult so I would suggest not going much above 20 holdings at any one time.

In recent years it has not been beneficial for private investors to reduce their shareholdings in the summer and then increase them in October. One risk with that strategy is that the market may move the wrong way and you find yourself buying back in at a higher level. The only sure thing is that you increase your dealing costs.

Tim Stubbs, investment manager at Fiducia Wealth Management says:

Your investment portfolio is extremely concentrated, dominated by just one asset class and one geography; we note that around three-quarters of your portfolio consists of smaller or midsized UK equities. Such a high concentration exposes you to significant risk.

To show why, we find it pays to imagine a set of worst-case events that could potentially disrupt your current investment structure. First, you are very vulnerable to stock market slumps, not least as your positions are generally smaller cap and therefore potentially prone to larger swings in price than larger-cap equity indices. On the back of a six-year bull run, we would be cautious about investing almost all of your monies into equities.

Second, you have invested in the shares of 17 domestic companies (and an additional four smaller holdings in permanent interest-bearing shares or preference share equivalents). Your largest four stock holdings represent around a third of your investment portfolio by value, worth just under £500,000 of your total £1.4m. In a bad-luck scenario, if one or more of these four companies were to face unforeseen company-specific problems, your portfolio could be significantly affected by non-market-related losses. Regardless of one's ability to pick stocks, more is left to chance when the fortunes of a very small number of companies becomes critical to your success.

Paul Derrien, investment director, Canaccord Genuity Wealth Management, says:

The portfolio is certainly higher risk, there is little in the way of a balance of asset classes, and approximately £80,000 of fixed-interest in a £1.4m portfolio is doing little to balance any risks. So I would assume that you are perfectly comfortable with this, have additional cash that you could invest, and the funds in fixed interest could be used to purchase additional equities if you felt the timing was good - though I note that the maturities of the fixed interest are short, the yields are strong and they are very attractive in terms of return profiles. If risk is potentially an issue then consider increasing the number of asset classes that have strong return profiles not correlated with equity.

The risk level is also potentially increased by the liquidity of the assets invested in - in other words, how easy they may be to buy and sell. While in good markets modest additions and sales to all of the investments would be possible, over £550,000 of the equity investments are in companies with limited liquidity. This would make any complete sale, given the size of the investments you have, possibly difficult to enact and in a falling market (or following some bad company news) potentially very difficult with prices moving sharply against you. Again I sense that this is a risk that you appreciate, but I would be wary of sizeable holdings in fairly illiquid holdings.

It looks like you have a well-researched, thought out, and well managed equity portfolio that looks to have outperformed over the years. You express a wariness of markets (1987), yet take quite a significant element of risk with the limited liquidity in a number of investments and the overall exposure to equity. As long as you are comfortable with this level of risk there is not a requirement for any drastic action. However given the size, and liquidity issues of a number of the holdings, I would look keep a lid on the size of the investments that you have and improve the overall diversification by adding some thematic and geographical equity holdings. This will reduce the risk of not being able to exit much of the portfolio in a swift fall in equity markets and will not add significantly to your research workload.

IMPROVING YOUR DIVERSIFICATION

Mr Forrest says:

To gain exposure to international markets it is not necessary to buy shares on foreign stock markets. One of the great advantages that British investors have is that the London market offers us the opportunity to invest in companies with operations all over the world. Many FTSE 100 companies derive most of their income from overseas and a large proportion comes from trading in fast-growing emerging economies. Another option would be to look at funds that specialise in overseas investment since they have the time and expertise to engage in the extensive research required to find attractive assets abroad.

Mr Stubbs says:

All your eggs are in the UK basket. Given high levels of government and household debt in the UK economy and a productivity challenge, one could equivalently argue that you should consider seeking investments in nations with superior fundamentals.

At Fiducia, we create internationally diversified portfolios that feature multiple asset classes including infrastructure, private equity, hedge funds, absolute returns, commodities and property, alongside developed market and emerging-market equities. UK equities currently represent no more than 12 per cent of any of our portfolios.

To provide a couple of examples as to the benefits of diversification, we note that the only asset class to generate positive returns since markets started turning down in April has been UK commercial property. Some funds in the IA Targeted Absolute Return sector, such as the City Financial Absolute Equity fund (GB00B2PX1C62) which is a key holding within our portfolios, have been able to generate strong gains on the back of falling markets. This fund uses an equity long/short strategy and aims to achieve a positive absolute return for investors over rolling 36 month periods.

You should reduce the importance that any single asset class or geography can have on your overall wealth and seek to gather as many unrelated returns streams as possible.

Consider a core-satellite approach to managing your investment monies.

For example, if the bulk were invested into a wide range of global asset classes, forming the 'core' portfolio (perhaps £1m+), first and foremost this would spread your eggs among a greater number of baskets. Depending on your preferences, the remainder could then be invested in a smaller 'satellite' portfolio of individual UK stocks, which you could manage in line with your existing approach.

Adopting a core-satellite approach in this fashion could significantly reduce many of the concentrated risks that you are exposed to through your existing portfolio. However, it would also allow you to continue managing a stock portfolio in a manner that you are comfortable with and enjoy, providing a reasonable blend of target outcomes.

Mr Derrien says:

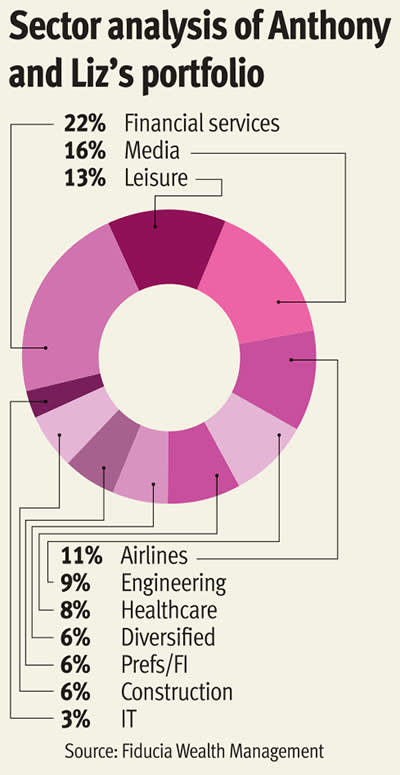

Diversification covers a number of areas, but with 17 equity holdings you have sufficient as there is little duplication of sectors. Ideally you might have a few more but, as you mention, it becomes increasingly time consuming to track all the companies.

Where I would consider enhancing the portfolio and reducing risk, would be through both global and thematic equity markets. You feel that you should be investing internationally, so I would consider using both the monies invested in the HSBC tracker and some top slicing of strong performing equities, to add a couple of funds to your portfolio. You could use specific geographical funds such as Europe (although I would still look for one with the potential for currency hedging whilst QE continues), or more generally through a global equity fund. Thematically, there remain opportunities in technology, healthcare and infrastructure. Investment trusts can offer good opportunities to pick up exposure to these themes and regions often at a discount to NAV; especially given the recent market movements.

*None of the above should be regarded as advice. It is general information based on a snapshot of the reader's circumstances.