The UK housebuilding sector has been through numerous boom to bust cycles. After many of the country’s big builders were brought to the edge of collapse during the financial crisis of 2008-09, the past few years have been much kinder to the companies and their investors.

During the past five years, shareholders in housebuilders have enjoyed stellar returns as share prices have soared and big dividends have been paid out. However, during the past year clouds have appeared over the sector and total returns to shareholders have turned sharply negative, even though profits and dividends have continued to increase.

History tells us that the fortunes of housebuilding companies will eventually turn downwards, but that predicting when that will happen is very difficult. However, by studying the sector’s financial performance, it is possible to get an insight into what current share prices are telling us about the future. You can then take a view as to whether you want to buy, sell or stay clear.

Housebuilding economics

Understanding how housebuilders make money is the key to weighing up the future prospects of the sector. The key variables are:

■ Average selling prices – these are a function of house prices generally, but are also determined by the mix of properties sold. There are differences in selling prices between flats and houses, affordable and private properties and across different areas of the country.

■ The cost of land – a crucial determinant of a builder’s eventual profit. The right location at the right price is key. In recent times builders have been increasing the amount of land bought without planning permission – known as strategic land – as it is cheaper and can give them higher future profits.

■ Build costs – essentially wages and building materials. A shortage of skilled labour has been pushing up building costs.

■ The number of properties sold – the more properties that are built and sold then the more revenue can be generated to cover fixed costs.

Below is a table built from Taylor Wimpey's (TW.) annual reports since 2007 (table 1). It shows you how it has achieved a profit or a loss from each housing plot sold. If you study this carefully, you can learn a great deal about what makes a housebuilder tick.

What this table tells you is how very dependent a builder’s profits are on rising sales prices. Let’s look at the period between the end of 2013 and the middle of 2016 for Taylor Wimpey. Let’s start with the cost per plot first. This has increased by £24,400 from £152,100 to £176,500. Land costs and other costs haven’t changed much. Build costs have accounted for all of the increase.

Some of these build cost increases will have come about due to changes in the types of properties built – bigger houses will cost more – but the cost of skilled labour such as bricklayers and plasterers has been going up due to shortages. These cost increases haven’t mattered too much because average selling prices have been going up at a faster rate. They have increased by £47,000 since 2013, with profit per plot increasing by nearly £23,000. Without these price increases it would have been difficult to make as much progress in terms of profits.

Table 1: Taylor Wimpey – Profit per plot (£000s)

| 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | H12016 | |

|---|---|---|---|---|---|---|---|---|---|---|

| Avg Selling price | 188.1 | 171 | 160 | 171 | 171 | 181 | 191 | 213 | 230 | 238 |

| Less: | ||||||||||

| Land cost | 46.7 | 47.5 | 34.9 | 38.1 | 35.5 | 39.4 | 41.2 | 45.1 | 42.4 | 40.3 |

| Build cost | 101.3 | 107.1 | 106.2 | 104 | 100.2 | 101.5 | 105 | 113 | 121.9 | 129.4 |

| Other costs | 16.4 | 20.1 | 7.2 | 6.5 | 6.5 | 6.4 | 5.9 | 5.3 | 6 | 6.8 |

| Total costs | 164.4 | 174.7 | 148.3 | 148.6 | 142.2 | 147.3 | 152.1 | 163.4 | 170.3 | 176.5 |

| Profit per plot | 23.7 | -3.7 | 11.7 | 22.4 | 28.8 | 33.7 | 38.9 | 49.6 | 59.7 | 61.5 |

| Margin | 12.60% | -2.16% | 7.31% | 13.10% | 16.84% | 18.62% | 20.37% | 23.29% | 25.96% | 25.84% |

Now look at what can happen when average selling prices fall as they did between 2007 and 2009.

House prices can change quickly, but costs do not tend to change as fast. Falling house prices can therefore decimate a builder’s profits. But there’s another impact to take note of as well. You will notice that the land cost per plot falls significantly between 2008 and 2009 from £47,500 to £34,900. This isn’t due to Taylor Wimpey stumbling across lots of cheap land – although land prices fall a lot more than house prices when the market turns down – but because it has to write down the carrying value of its land on its balance sheet.

For housebuilders, land is the same as stocks of goods for a retailer. Their value has to be shown at the lower of cost or market value. The price of land is determined by the price of houses that can be sold on it. What effectively happens is that builders work backwards from the selling price of the house, take away the building costs and an acceptable profit margin and what it left over is the price of land. So when house prices fall the price of land falls by a lot more in percentage terms. This has been borne out during the most recent house price falls in the early 1990s and 2008-09.

Look at table 2 below to see what I mean. A housebuilder is making a 20 per cent profit margin on each plot sold. Selling prices then fall 10 per cent, but build costs take time to adjust. If the builder wants to earn a 20 per cent profit margin (£18m) on the lower price it has to pay less for land. In this case, the cost of land drops from £22,000 to £14,000 – a 36 per cent drop.

Table 2: The effect of falling prices

| Profit per plot (£k) | Before | After | % change |

|---|---|---|---|

| Selling price | 100 | 90 | -10.00% |

| Less: | |||

| Build costs | 55 | 55 | 0.00% |

| Other | 3 | 3 | 0.00% |

| Land | 22 | 14 | -36.40% |

| Profit | 20 | 18 | -10.00% |

When house prices fall, the much bigger impact on land prices can wreak havoc with housebuilders’ balance sheets. In 2008-09, most housebuilders posted significant write-downs in the value of their land holdings. This destroyed their profits, blew a big hole in the value of shareholders’ equity and limited their ability to pay dividends. Conversely, when house prices rise, the value of land increases, and this tends to get reflected in higher share prices for housebuilding companies. This is what has been happening for the past few years.

The bottom line is that house prices matter a great deal to housebuilding companies and their shareholders. Falling prices are very bad news, but falling house price inflation could also be a problem if build costs continue to go up.

UK house prices

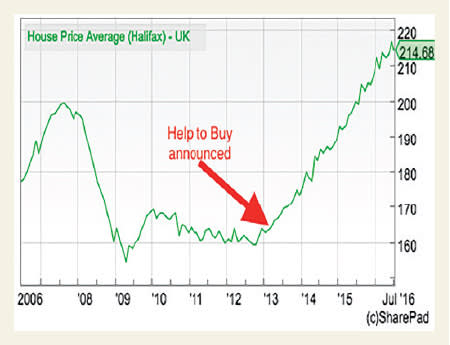

House prices fell significantly in the aftermath of the 2008-09 financial crisis. They then staged a weak recovery before stagnating between 2010 and 2012. Then came the announcement of the government’s Help to Buy scheme in April 2013. With the taxpayer essentially providing 20 per cent equity loans to house-buyers, banks became much less nervous in lending money against property values.

The increase in availability of 95 per cent loan-to-value (LTV) mortgages – which were effectively 75 per cent LTV mortgages as far as the banks were concerned due to Help to Buy – put money in buyers’ pockets and lit the blue touch paper under UK house prices as shown in the chart, right.

Since then the builders have been in a sweet spot. Not only has demand for houses been boosted by Help to Buy and low mortgage interest rates, but the supply of houses has been extremely tight. In 2007, 234,000 new homes were built in the UK according to the Office for National Statistics (ONS). In 2015, only 177,000 were built. The builders blame the long-winded planning system in the UK for holding back the supply of houses. Others accuse the builders of sitting on their land where they have planning permission – known as land banking – and effectively gaming the market in their favour, although evidence for this is patchy.

Either way, life for housebuilders at the moment is good. But how long can it last? UK house price inflation slowed to 8.3 per cent in the year to July 2016 according to the ONS, and prices fell in some parts of London, but affordability remains a big issue. The higher rates of stamp duty on buy-to-let investors and second properties has also subdued demand for houses.

Poor affordability has led some economists to take the view that house prices will have to start falling, and this is one of the reasons why housebuilding shares have fallen out of favour with investors during the past year. According to the Halifax House Price Index, average house prices are just under six times average earnings which is slightly below the peak valuation in 2007.

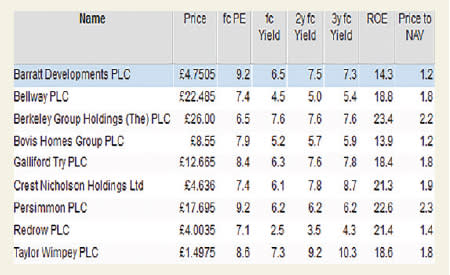

Linked to the issue of affordability is how reliant housebuilders have become on the Help to Buy scheme to sell houses. With the exception of Berkeley Group (BKG) which has a very low exposure to the scheme, many builders have around 30 per cent of their sales volumes linked to it. For builders such as Taylor Wimpey and Persimmon (PSN), the figure is over 40 per cent.

The government has extended the scheme to 2021. Without it, life for the builders would have undoubtedly been much tougher. However, it remains to be seen how much more Help to Buy can contribute to rising house prices, which are increasingly important to offset rising build costs.

Financial performance of housebuilding companies

So how has this favourable market backdrop fed through into the housebuilders’ financial performance? Very nicely is the answer. If you are going to look at two key measures of financial performance for housebuilders, arguably the best two are:

■ Operating profit or the earnings before interest and tax (Ebit) margin – the percentage of turnover turned into profit.

■ Return on equity – post-tax profits as a percentage of the money invested by shareholders.

Looking at operating profit margins first, we can see from Table 3 below that, with the exception of Bovis and Persimmon, margins are at all-time highs. If you believe that housebuilding is a cyclical sector, then these profit margins would suggest that we are nearer the top rather than the bottom of the cycle.

That’s not to say that margins cannot keep increasing for a while yet. Housebuilders continue to talk bullishly on how favourable the land buying market is. This is allowing them to buy parcels of land which can make high-profit margins and returns on capital employed (ROCE) at current selling prices.

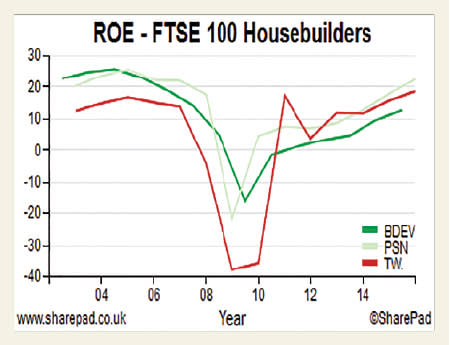

Return on equity (ROE) – shown in table 4 – is telling us a similar story. With the exception of Barratt, they are close to or ahead of the peaks achieved in the last house price boom.

These trends in profitability and ROE are very useful to help investors value housebuilding shares properly.

Valuation of housebuilding shares

Taking into account the current high levels of profitability in the sector, where does this leave the value of the shares? How do you know if a housebuilding share is cheap or expensive?

Many professional analysts value housebuilding shares by comparing the share price with the net asset value (NAV) per share. Using NAV makes sense when a company’s assets can be turned into cash relatively quickly. In the case of a housebuilder, the bulk of its NAV will be made up of unsold houses already built and plots of land less any debts. Sometimes, the net tangible asset value (NTAV) per share is used, which takes away the value of intangible assets such as goodwill.

During bad times when the housing market is depressed, housebuilders’ shares can be bought for less than their NAV per share. When times are good and investors are optimistic about the prospects for future profits growth, the shares can change hands at significantly more than NAV per share.

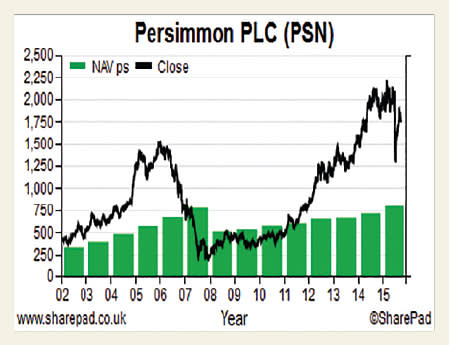

When looking at an individual housebuilding company you should look at the history of its P/NAV valuation and see where the shares are trading relative to their historic range. If it is at the low end and the outlook is good then that might indicate a potential buying opportunity. A valuation at the high end might signal that the shares don’t offer much profit potential.

The history of Persimmon’s share price compared with its NAV per share is shown in the chart to the right. As you can see, its shares are currently changing hands for considerably more than its NAV, which is telling us that the shares are very popular with investors at the moment. The same is true for the rest of the sector.

Table 3: Operating profit margins

| Name | EBIT margin | 1y ago | 2y ago | 3y ago | 4y ago | 5y ago | 6y ago | 7y ago | 8y ago | 9y ago | 10y ago |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Barratt Developments | 17.5 | 16.6 | 14.3 | 13 | 8.8 | 7.4 | 4.4 | -19.4 | 9.8 | 16.7 | 16.9 |

| Bellway | 20.4 | 17.2 | 13.6 | 11.4 | 8.5 | 6.6 | -3 | 4.7 | 18.6 | 19.2 | 19.5 |

| Berkeley Group Holdings | 26.3 | 26.1 | 23.9 | 20.3 | 18.6 | 18.6 | 17.3 | 17.6 | 20.5 | 20 | 18.8 |

| Bovis Homes Group | 17.5 | 17 | 14.9 | 13.6 | 10.4 | 7.5 | 7.1 | -19.1 | 22.4 | 23.1 | 24 |

| Crest Nicholson | 20.3 | 20.1 | 18 | 17.5 | 17.2 | 17.2 | |||||

| Galliford Try | 6.5 | 5.5 | 5.9 | 5.5 | 4.6 | 2.8 | 2.2 | 2.1 | 4.4 | 4 | 4.5 |

| Persimmon | 21.7 | 18.3 | 16.4 | 12.7 | 11.7 | 13.8 | 8.9 | -28.8 | 20.7 | 20.8 | 23.1 |

| Redrow | 18.9 | 18.5 | 16.3 | 12.7 | 10.1 | 6.9 | 3.2 | -39.4 | -27.2 | 16.3 | 17.1 |

| Taylor Wimpey | 20.3 | 18.7 | 15.7 | 11.2 | 9.3 | 4.1 | -18.6 | -26.5 | 3.9 | 12.9 | 13.3 |

Source: SharePad

Table 4: Return on equity

| Name | ROE | 1y ago | 2y ago | 3y ago | 4y ago | 5y ago | 6y ago | 7y ago | 8y ago | 9y ago | 10y ago |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Barratt Developments | 14.3 | 12.8 | 9.6 | 4.8 | 3.4 | 1.3 | -1.5 | -15.8 | 4.9 | 14.2 | 19.1 |

| Bellway | 18.8 | 14.8 | 9.2 | 7.2 | 4.7 | 3.6 | -2.8 | 2.7 | 17.2 | 18.4 | 20.5 |

| Berkeley Group Holdings | 23.4 | 27.5 | 21.2 | 17.4 | 12.5 | 10.7 | 9.6 | 11.6 | 19.2 | 16.7 | 16.6 |

| Bovis Homes Group | 13.9 | 12.4 | 7.7 | 5.5 | 3.4 | 2.1 | 1.3 | -6.1 | 12.4 | 14.3 | 14.3 |

| Crest Nicholson Holdings | 21.3 | 19.6 | 18.1 | 22 | 43.1 | ||||||

| Galliford Try | 18.4 | 17.7 | 14.6 | 11.8 | 10 | 5.9 | 3.8 | 9.6 | 16.2 | 15.1 | 26.7 |

| Persimmon | 22.6 | 17.8 | 12.9 | 8.7 | 7 | 7.6 | 4.6 | -21.6 | 17.5 | 22.1 | 22.2 |

| Redrow | 21.4 | 21 | 15.9 | 9.7 | 6.6 | 4.1 | 0.2 | -28.7 | -28.3 | 15.5 | 17.4 |

| Taylor Wimpey | 18.6 | 15.7 | 11.7 | 12 | 3.9 | 17.2 | -35.5 | -37.6 | -4.3 | 13.9 | 15.2 |

Source: SharePad

Working out the right P/NAV valuation

This is a little bit more advanced analysis but stay with me on this and hopefully you’ll understand what I am going on about. As you can see from the chart on page 30, there is a relationship between a company’s return on equity (ROE) and its share price. Share prices tend to rise when ROEs are rising and vice versa.

The rising share price also results in a higher P/NAV – the gap between the share price and NAV per share tends to get bigger. This is shown in the preceding chart.

This makes sense. A company with a higher ROE can grow in value faster than one with a lower ROE, just like a savings account with a higher rate of interest. It stands to reason that it should have a higher valuation and higher P/NAV multiple.

Professional investors try to determine the right P/NAV multiple for a share by estimating a company’s sustainable return on equity and comparing it with the returns required by shareholders to invest in the company – known as the cost of equity (COE).

This required return or cost of equity is one of the most hotly debated topics in finance. There’s no right answer to what number it should be. I’m not going to get into this topic right now, but most professional investors assume that it is around 8 per cent. Feel free to choose a value that you are comfortable with.

Getting back to the P/NAV multiple. The logic here is that a share is only worth its NAV per share if the company can produce an ROE that is equal to or more than the cost of equity. So if the sustainable ROE is 8 per cent then the estimated P/NAV is worked out by dividing the ROE by the COE:

P/NAV = ROE/COE = 8 per cent/8 per cent = 1.0

If the sustainable ROE was 16 per cent the P/NAV would be: 16 per cent/8 per cent = 2.0

If the sustainable ROE was only 4 per cent then it would be: 4 per cent/8 per cent = 0.5

So we now have some simple rules:

■ ROE >COE then P/NAV >1.0

■ ROE=COE then P/NAV = 1.0

■ ROE < COE then P/NAV <1.0

So if you were looking at a share with a sustainable ROE of 12 per cent and a cost of equity of 8 per cent and a NAV per share of 100p this is how you would work out a value for the share:

Implied P/NAV = 12 per cent/8 per cent = 1.5

Value per share = NAVps x P/NAV = 100p x 1.5 = 150p

This approach contains an important lesson for investors. A share with a P/NAV of less than 1 is sometimes seen as being cheap. It might not be if it cannot make a sustainably high ROE. Bargains do exist when ROE is temporarily depressed and can recover from a low to sustainably higher average levels in the future.

So how do we go about valuing housebuilders using this method? This is not easy because of the up and down nature of the sector with periodic booms and busts. Estimating a sustainable ROE is not easy.

If we take a view that the current ROEs (see table 5 below) – which are close to or ahead of the ROE’s achieved at the last cyclical peak – can be sustained forever then the whole sector looks very cheap indeed. This is not likely to happen if history is any guide. History tells us that housebuilding moves through peaks and troughs in profitability and ROE. A sensible valuation might take this into account. Table 6 below gives implied valuations based on 10-year average ROEs which takes into account a boom and a bust.

This might not be the right approach either, as the past booms and bust are unlikely to be repeated identically. However, with the exception of Berkeley Group, all the shares look overvalued. In the words of value investor Ben Graham, it seems there’s not much in the way of a margin of safety here.

Table 5: ROEs

| Name | ROE | Implied P/NAV | NAV ps (p) | Implied Price (p) | Close | Upside/ Downside |

|---|---|---|---|---|---|---|

| Barratt Developments | 14.3 | 1.79 | 398.7 | 712.7 | 473.4 | 50.50% |

| Bellway | 18.8 | 2.35 | 1286.3 | 3022.8 | 2237 | 35.10% |

| Berkeley Group | 23.4 | 2.93 | 1311.2 | 3835.3 | 2553 | 50.20% |

| Bovis Homes Group | 13.9 | 1.74 | 712.7 | 1238.3 | 857.5 | 44.40% |

| Crest Nicholson Holdings | 21.3 | 2.66 | 250.6 | 667.2 | 462.8 | 44.20% |

| Galliford Try | 18.4 | 2.3 | 724 | 1665.2 | 1276 | 30.50% |

| Persimmon | 22.6 | 2.83 | 800.7 | 2262 | 1748 | 29.40% |

| Redrow | 21.4 | 2.68 | 275 | 735.6 | 405.1 | 81.60% |

| Taylor Wimpey | 18.6 | 2.33 | 83.6 | 194.4 | 147.8 | 31.50% |

Source: SharePad

Table 6: Implied valuations based on 10-year average ROEs

| Name | 10y avg ROE | Implied P/NAV | NAV ps | Implied Price (p) | Close | Upside/Downside |

|---|---|---|---|---|---|---|

| Barratt Developments | 4.8 | 0.6 | 398.7 | 239.2 | 473.4 | -49.50% |

| Bellway | 9.4 | 1.18 | 1286.3 | 1511.4 | 2237 | -32.40% |

| Berkeley Group | 17 | 2.13 | 1311.2 | 2786.3 | 2553 | 9.10% |

| Bovis Homes Group | 6.7 | 0.84 | 712.7 | 596.9 | 857.5 | -30.40% |

| Galliford Try | 12.3 | 1.54 | 724 | 1113.2 | 1276 | -12.80% |

| Persimmon | 9.9 | 1.24 | 800.7 | 990.9 | 1748 | -43.30% |

| Redrow | 3.7 | 0.46 | 275 | 127.2 | 405.1 | -68.60% |

| Taylor Wimpey | 1.6 | 0.2 | 83.6 | 16.7 | 147.8 | -88.70% |

Source: SharePad