Hunting for value in the oil and gas sector is not easy at the moment. The oil majors have rallied considerably in recent months, leaving their valuations stretched in a still-tepid price environment, while many smaller players, some of which boast excellent assets, are either mired in debt or endlessly locked in rounds of fundraising. However, one good candidate for investment on value grounds is Ophir Energy (OPHR), an explorer and producer with on- and offshore assets in Asia and Africa. That's because the cashed-up group looks attractive on a range of asset-based valuation metrics, all of which throw in the company's promising developmental assets in Equatorial Guinea, Tanzania and Indonesia for very little. What's more, the market has ascribed an enterprise value to Ophir that prices its 2P reserves at just $5.60 (£4.62) per barrel, well below the sector average of closer to $10.

- Proven production

- Excellent development assets

- Big discount to book value

- Net cash position

- Exploration risks

- Tanzania asset uncertainties

Naturally, that figure only means something if the oil cannot be profitably extracted. Yet the company expects this year's output from its Bualuang and Sinphuhorm wells in Thailand - set to average 11,000 barrels of oil equivalent a day - to deliver underlying post-tax cash flow of between $15 and $23 per barrel. That's no mean feat given Brent crude has spent most of 2016 below $50 a barrel, and shows that Ophir can rely on a significant source of cash generation to help it build its portfolio elsewhere. It is heavy investment in exploration (net cash fell $185m in the year to the end June) that may partly explain why Ophir has not significantly re-rated, unlike many other dollar-earning resources stocks. The absence of a dividend probably hasn't helped either.

At present, development drilling is focused on Myanmar, Tanzania, Indonesia and Côte d'Ivoire, the last of which was recently "high-graded" - industry jargon for improving the quality of the highest-return assets - to prospective resources of 240m barrels of oil.

But the asset that holds the greatest immediate promise is the 80 per cent-owned Fortuna liquefied natural gas (LNG) development in Equatorial Guinea. The block - which is expected to produce 2.2m metric tonnes of gas a year - is now ready for a final investment decision that would lead to first gas by 2020, when regional demand is expected to rise. Before then, Ophir needs to approve one of two "world-class" consortia bidding for the upstream contract, which has been revised down from $1bn at the end of 2014 to just $450m. The company has also shortlisted four gas offtake partners, which should form an important source of prepayments and capital, thereby mitigating the potential risks of dilutive fundraising.

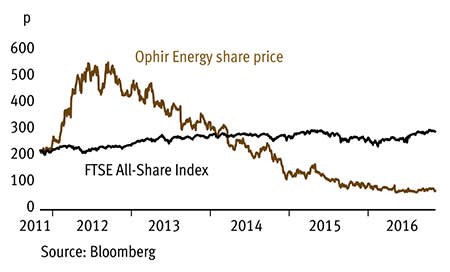

We should hold our hands up and admit that we've previously been wrong on Ophir, tipping its shares in September 2013 at 325p. Since then, the oil price and the slow pace of project development have been the twin sources of punishment. But with the oil price stabilising, the time looks ripe for a second check.

OPHIR ENERGY (OPHR) | ||||

|---|---|---|---|---|

| ORD PRICE: | 75p | MARKET VALUE: | £530m | |

| TOUCH: | 74.8-75.3p | 12-MONTH HIGH: | 107p | LOW: 64p |

| FORWARD DIVIDEND YIELD: | NIL | FORWARD PE RATIO: | NA | |

| NET ASSET VALUE: | 227¢ | NET CASH: | $207m | |

| Year to 31 Dec | Turnover ($m) | Pre-tax profit ($m) | Earnings per share (¢) | Dividend per share (¢) |

|---|---|---|---|---|

| 2013 | 0.0 | -280 | -42.0 | nil |

| 2014 | 0.0 | 288 | 10.0 | nil |

| 2015 | 161 | -376 | -46.0 | nil |

| 2016* | 182 | 9 | -1.0 | nil |

| 2017* | 228 | 26 | -3.0 | nil |

| % change | +25 | +189 | - | - |

Normal market size: 15,000 Matched bargain trading Beta: 1.58 £ =$1.22. *JPMorgan forecasts | ||||