I am not alone in thinking this way. Dr Ted Malloch, former Oxford professor, europhile and potentially Mr Trump's Ambassador to the EU, has publicly said: "You may think the Trump election is a so-called black swan event, or as one commentator called it a 'white lash'. It is not. Rather it is part and parcel of a much larger global pendulum swing towards populism and nationalism after decades of elitist globalism. The post-Berlin Wall consensus is over. Going around telling the locals that they are racists for opposing migration does not help. No longer do we need to have ultimate allegiance paid to corrupt international organisations."

The point here is that, just as it did in the great financial crash of 2007, consensus thinking leads to very crowded trades. With this in mind, as British remoaners try every technical tactic to block the country's exit from the EU and US students demand 'safe spaces' at college, let's look at this year's potential clangers/swans/swoons and cliff-edges.

As I see it the logic runs as follows: The US economic recovery will gain traction because the new President is a good businessman and he will invest in infrastructure. To do this he will be happy for his government to borrow a lot more money, which will push yields much higher. Both these issues will be inflationary, but will also make the US dollar stronger. We look at charts of four markets associated with these trends.

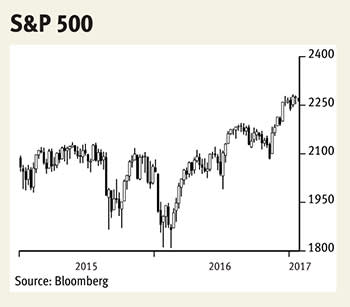

The S&P 500 closed at 2139 on 8 November 2016, matching the high of May 2015. Since then it has rallied 6.66 per cent (worrying for some, perhaps) which is impressive over a one-month period but hardly stellar over 20 months (equivalent to 0.33 per cent per month). The question now is whether the so-called economic recovery that President Obama engineered can pick up the pace and will be reflected in stock market rallies. Consumer spending will find it difficult to take up the slack because the labour force participation rate of 62.7 per cent is at its lowest since 1978 (from a peak at 67.3 in 2000).

Interest on 30-year Treasury bonds is at or close to rock bottom in the bigger scheme of things, even after backing up a bit on Trump. At 3.00 per cent they are halfway between last year's record low and 2013's 'taper tantrum'. No change in trend here.

Treasury inflation-protected securities (Tips) maturing in February 2042 have already reversed half of last year's falls as investors rethink their usefulness and value. No change in trend.

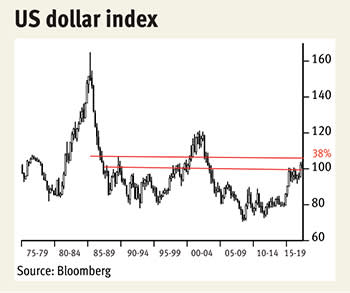

Which leaves the US dollar index hovering at some of its more expensive levels in decades. Very heavy lifting needed to rally convincingly.