- The UK remains the most mature e-commerce market in Europe

- Covid-19 and social distancing have had a profound effect on the way alcohol has been consumed through 2020

Shortly after the country started tracking the rising death toll from Covid-19, morbid headlines also began to spread across the business pages of national newspapers.

From retail to hospitality, commentators said entire sectors faced existential threats. With consumers moving online and companies in the virtual world picking up the profits, a death knell sounded for the bricks-and-mortar businesses that have been serving consumers in person for decades, if not centuries.

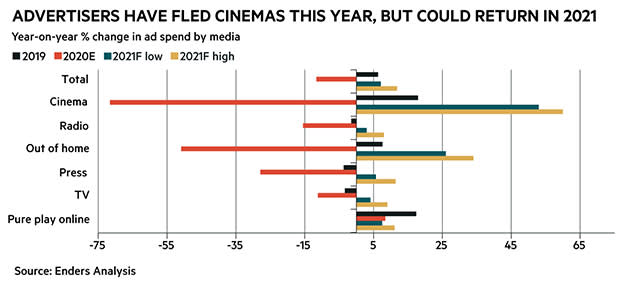

Investors have been responding to these gloomy prophecies. Shares in cinema chains have plunged this year, just as Netflix (US:NFLX) saw its stock surge more than 50 per cent. High-street retailers were also battered on the markets, while Amazon (US:AMZN) and its e-commerce peers climbed to new heights.

The severity of these price moves, with technology companies trading at eye-watering multiples of their current earnings, seems to reflect a belief that the online revolution will persist long after the Covid-19 crisis.

In many cases, predictions of a long-term change in consumer habits seem justified. But not every consumer has crossed the digital rubicon forever, and there may also be plenty of life in the more traditional businesses yet.

Click-and-collect

The UK remains the most mature e-commerce market in Europe, although it is still evolving. Prior to this year’s disruption, click-and-collect services accounted for roughly a third of transaction volumes, with non-grocery items representing the lion’s share of sales. However, physical retailers have become more mindful of the benefits on offer, not only in terms of shielding operating margins from delivery costs, but also through increased footfall at their stores, together with upselling opportunities aimed at customers arriving to collect packages.

In terms of e-commerce, it is sometimes said that the final mile of a package’s journey is the most problematic, both in terms of logistics and profitability. We may have become more accustomed to home delivery because of the lockdowns, but e-tailers appreciate – and are looking to exploit – the advantages of click-and-collect where consumers are concerned. For a start, there are no additional shipping costs. And by using the service, householders do not have to tailor their schedules to fall into line with courier delivery times, a significant factor given that many people are considered time-poor in the modern age. There are also issues surrounding security and damage which can act as a disincentive for consumers.

If you require proof positive that click-and-collect services are becoming further entrenched in the retail sphere, you need only take note of the banks of Amazon lockers at your local train station, supermarket, or mixed-use site. This is a clear reflection of growing symbiosis in the e-commerce space, which has not only stretched beyond bricks-and-mortar retailers to online-only channels, but will be in evidence long after Covid-19 is brought under control.

Drinking at home

It is widely held that the people of these Isles are partial to a drink. And Covid-19 and social distancing have had a profound effect on the way that alcohol has been consumed through 2020. The question is whether the changes brought about by the lockdown have become hard-wired where UK consumers are concerned, or if they merely represent an aberration?

Analysis from Nielsen Scantrack shows that although sales of supermarket alcohol went through the roof during the initial lockdown period (the 17 weeks to 11 July 2020), the overall volume of alcohol purchased in the UK came up well short of the comparable period in 2019. This is heartening in the sense that socialising – rather than the base practice of getting sloshed – seems to be the primary motivation driving alcohol consumption. However, it is by no means clear what the on-trade in the UK will look like once a degree of normality is restored. After all, summer only saw a phased reopening of venues that serve alcohol and many punters remain reluctant to drink in pubs and restaurants due to fears over contracting the virus.

Influential trade body, the British Beer & Pub Association, has warned that without enhanced government support measures, more than 30,000 pubs – 80 per cent of those in England – are at risk of closing for good if the tier system drags into March and beyond, to say nothing of independent brewers. If such a ghastly scenario plays out, it will result in an effective supply-side shortage, although it is difficult to say how many licensed premises would eventually reopen.

Although the consumer switch to the off-trade is the result of government regulation, it is depressingly conceivable that more people may eventually decide to consume more booze at home simply because of the relative cost benefits, particularly if a post-pandemic economic slump weighs on household disposable income.

With time on your hands– do it yourself

With the daily commute a relic of a bygone age, widespread furloughs in effect, and more time for householders to assess their living arrangements, Covid-19 has triggered a surge in home improvements, to go with its positive effect on hobbyists and the gaming fraternity.

The galvanising effect on DIY sales volumes is evidenced by the performance of Kingfisher (KGF) at the height of the pandemic. The parent group of B&Q and Screwfix saw like-for-like (LfL) sales increase by more than a fifth in the three months to 18 July, with online channels increasingly to the fore. Momentum has been maintained through the third quarter, with LfL sales up by 17.6 per cent, while click-and-collect transactions registered a 216 per cent increase. There was even a spike in sales ahead of the second national lockdown in England on 5 November.

Research published by Aldermore Bank midway through the year showed that38 per cent of adults have undertaken DIY or renovation jobs during the lockdown period, with 18- to 34-year-olds leading the way, intriguingly. A separate survey conducted by housebuilder Redrow (RDW) indicates that a quarter of UK householders will reassess how they want to use the space in their homes. Conceivably, this could support a certain level of demand going forward if temporary effects give way to a long-term trend. But household consumers may be just as keen to get out of familiar surroundings once fears over the virus and public spaces dissipate.

Online commerce isn’t just bigger – it’s better

It will come as no surprise that more people have shopped online this year than ever before. Data from Barclaycard showed that while face-to-face purchasing fell by 7.6 per cent in October compared with last year, online spending grew by just over a tenth. But for most people this was not a new habit – before 2020, the UK was already one of the biggest e-commerce markets in Europe. Shipping software company sendcloud estimates that online sales in the UK reached nearly £200bn last year. But the way that people shop online is changing, and the experience of buying something over the internet is evolving all the more rapidly now that it has become more deeply embedded in our lives.

There has been a marked rise in the use of online marketplace platforms – indicated by the stellar success of Etsy (US:ETSY) this year. Indeed, the platform’s share price has more than tripled over the course of 2020, as consumers flocked to its sellers for homemade face coverings. Total app downloads reached 2m last month, according to the research firm SensorTowers. In-app shopping too has featured more prominently this year. And platforms are quickly adapting to meet the new demand – or in some cases, trying to create it. Facebook (US:FB), for example, has introduced a shopping service on its photo sharing app Instagram.

This is good news for Apple (US:AAPL), which gets a cut of all in-app transactions that were downloaded on its app store (although it has cut this fee down to15 per cent for smaller developers). In any case, the e-commerce market is evolving quickly – even Paypal (US:PYPL) now allows its users to trade in the cryptocurrency Bitcoin. As platforms and payment methods develop, the e-commerce market is not only getting bigger, it is becoming more advanced.

Hospitality meets takeaway

As lockdown restrictions closed restaurant doors, consumers opened up takeaway apps from the likes of Uber (US:UBER) and Deliveroo, in which Amazon now holds a stake. Indeed, there has been a flurry of corporate activity in the market this year – not least in the shape of the massive JustEat Takeaway (JET) merger in Europe, which was worth £6.2bn.

But the Pfizer (US:PFE) and BioNTech’s (US:BNTX) vaccine has now arrived in the UK. While there still remains the logistical and political challenges of administering the vaccine to the population, it appears that a more normal future for 2021 is tangible. As such, we do not expect that the rise of the takeaway will kill the restaurant – there is no replacing the ambience and social element of convening around a well-lit table.

That is not to say that the takeaway market itself has not changed: it has become more competitive, and smaller independent restaurants who have struggled for the past year will more eagerly sign up to agreements with takeaway services. With more customers, more partners (UberEats’ active restaurants grew by more than half year on year in June), and more competition, the takeaway market has never looked so dynamic.

The viewers control the media

During the lockdown periods this year, we spent on average 28 minutes per day with our noses in a book. That is compared to three hours either sitting in front of a television or streaming videos. And it can be hard to resist the pull of the screen over a book – especially as streaming giants such as Netflix, despite lockdown, continued to drip-feed viewers a steady supply of new content to binge watch. Walt Disney (US:DIS) launched its Disney+ streaming service, which already has attracted more than 73m paid subscribers.

Traditional media means that a publisher selects what we watch and the time that we watch it – viewers simply tune into a broadcaster like ITV (ITV), or the BBC for example. But this year we have expressed a preference for the more interactive option – we want more control over the content we consume.

This might also explain why consumers are playing more video games, where they have a direct impact on what is happening on screen. UK development in the sector grew to record levels in 2020: no doubt helped by the launch of two new consoles from Sony (JP:) and Microsoft (US:MSFT). Greater interactivity is perhaps the next step in media consumption: Netflix has frequently experimented with shows that allow viewers to pick the course of action of the protagonist. While growth is expected to slow for streaming giants, we do not think it is likely that they will give up their newly-won market share, or reverse consumer expectations of a constant flow of high-quality, relevant content.

Opinion

Will 'Sell in May and go away' work in 2024?

Trading volumes and investor enthusiasm might hold the key to the May phenomenon – assuming, of course, that there is one

Mark Robinson