The eurozone economy is growing well, and might continue to do so.

Next Tuesday’s purchasing managers' surveys are expected to report that both services and manufacturing are expanding strongly, with growth in the latter close to a six-year high.

Other surveys, however, might show a couple of clouds bubbling up in this otherwise sunny sky. Ifo’s survey of German business conditions could show a second successive slip, albeit from near-record highs. And the National Bank of Belgium’s business confidence survey might continue what the Bank described last month as a “relatively gloomy trend” in manufacturing conditions: this matters, because Belgium is often seen as a bellwether of conditions in the eurozone generally.

For now, though, I suspect we shouldn’t worry much about these. One big fact suggests the eurozone’s expansion can continue, at least for a while: monetary conditions favour growth.

ECB president Mario Draghi has promised that interest rates will remain at their current levels for “an extended period of time”; this means a zero refinancing rate for many more months.

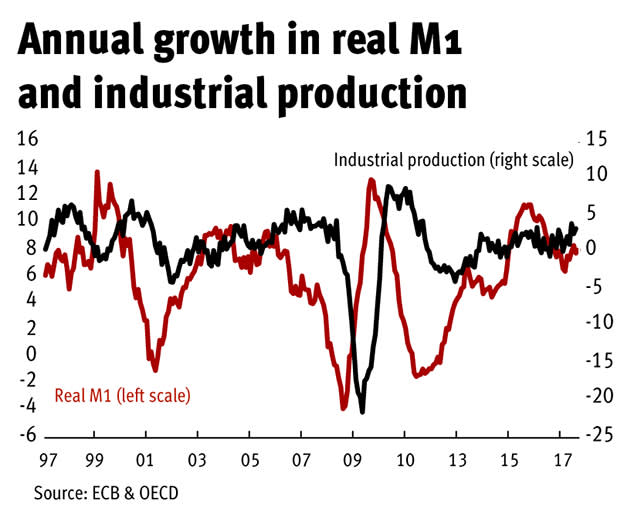

It’s not just the price of money that supports growth, though. So too does the quantity of it. Latest figures show that the M1 measure of the money stock – which comprises notes and coins and bank deposits that are readily withdrawable – rose by 9.5 per cent in the year to August. Controlling for inflation, this is growth of 8 per cent, which is well above the average growth since 2000 of 5.7 per cent.

This matters because this measure has been a good leading indicator of economic activity. The three significant slowdowns in output growth since the inception of the eurozone were all preceded (with a lag of a few months) by slowdowns in real M1. And pick-ups in growth in output – in 2000, the mid-00s, 2010 and 2016-17 – were all preceded by good growth in real M1.

With real M1 still growing strongly, this relationship points to decent ongoing growth in output.

In this context, we shouldn’t worry much about the effects of the recent rise in the euro: its trade-weighted index has risen by almost 7 per cent so far this year, in part because the stronger economy has strengthened the currency. The fact that the UK’s trade gap hasn’t responded much to sterling’s fall tells us that net trade isn’t very responsive to exchange rate fluctuations. The strong euro might cause a squeeze on exporters’ profit margins and perhaps even a trimming of capital spending intentions. But it shouldn’t derail the expansion.

This is good news for even the most parochial of UK equity investors simply because there’s a good link between eurozone industrial production and the All-Share index. Since 1996 the correlation between annual changes in the two has been a hefty 0.54, with each percentage point of higher output growth associated with 1.7 percentage points of higher equity returns.

The eurozone, therefore, gives us a good reason to be optimistic about UK shares.