Euromoney is one of those FTSE 250 businesses of which many people may never have heard, sitting in the relatively unglamourous Industrial Support Services sector. A casual glance might suggest that this is primarily a magazine publisher – the group’s name after all is a portmanteau of two leading print titles and it does publish a sizeable number of magazines. However, there is considerably more to this company and it is in fact one of those businesses that plays a pivotal role in the workings of numerous industries globally, albeit its input is largely unseen by the public at large.

Euromoney is primarily a business-to-business (B2B) information services provider, delivering ‘price discovery’ and market intelligence to a wide range of financial and industrial markets. The information and pricing data it handles is mostly from what are called ‘opaque’ markets. As the term suggests, this means rarer and more unusual market data that few (if any) other providers can deliver. In addition to data provision, it organises and runs trade shows, exhibitions and other corporate events, although due to Covid this part of the business is relatively inactive and has been a drag on the remainder which has been largely unaffected by the pandemic.

The world today is overrun with data and the world’s economy can really only run efficiently if business critical data is readily available and flows easily to those who need it. More important than availability of information is both the quality of the data and the assurance that it can be relied upon. A considerable amount of data and information is readily available: market financial information is a prime example as are the likes of oil, copper, cotton or iron ore prices. But there are myriad products vital for a host of businesses and the wider economy for which information much less accessible – this is opaque data. This encompasses the likes of paper, forestry products, small batch chemicals, foodstuffs, agricultural goods, freight or uncommon metals. In order to execute transactions successfully, business and other organisations need quality assured, trustworthy and well-audited information and this is the core of Euromoney.

The value of trust

During the Libor rigging scandal it became clear that market essential interest rate data could no longer be trusted, and since then there has been a heavy requirement for market-essential data to be very heavily audited and verified. In many ways how trustworthy and how well externally audited a data source is almost as valuable as the hard data itself. If two parties are to agree on contract terms there needs to be trust and accountability. Using Euromoney’s data sources, counterparties can rely on strong levels of assurance outside of themselves: Euromoney’s internal processes and its own data auditors including the likes of British Standards (BSI) and the Office of the Information Commissioner (ICO).

The scarcity of its data, its trusted quality and the quality of its distribution platforms have allowed the group to sustain strong pricing and solid margins.

Subscription model

Another attraction is how the group’s data services are paid for. The bulk of Euromoney’s revenues come in the form of subscriptions, an attractive model for any business. Payments by users are longer term in nature (typically 12 months minimum), have high roll-over/renewal rates and the fees are paid in advance. This provides strong visibility and a favourable cash-flow profile. If it were not for the considerable swing factor that now accompanies the event sector (see later) Euromoney might present one of the market’s more assured levels of revenue. While confidence and assurance are good, that can make for a dull investment as share prices are much more driven by shocks and surprises than they are by certainty.

The other advantage of the opaque dataset and subscription model is that it has high operational gearing, namely that a very large percentage of any additional revenue falls through to profit. This is because there is very little additional cost required to service the incremental customer – “create once, sell many” is a group mantra. This does mean, however, that any new data services can drag on profits in their early days and operational gearing works against you if you are losing revenues.

Flies in the ointment

To this point, the Euromoney business model appears very strong and very robust. But there have been a couple of major blows to the business in the last thee to four years that look to have undermined market confidence.

Events – until 2019, in-person events promoting and showcasing various of the group’s products and services provided a large portion of the total revenues. In 2019, these accounted for around 40 per cent of total revenues, weaving through different product areas and disciplines: then came Covid. In 2020, Covid lockdowns and travel restrictions saw incomes halve, and by H2 of that year they were running down 80 per cent. In FY2021, revenues fell by another 25 per cent. While events were neither the driver of profits nor the main growth engine of the group and had lower margins than the quasi-software data businesses, the speed and extent of the fall here did somewhat catch the market napping. When the revenue evaporated, the division's costs largely remained and management seemed to hope/believe that the impact would be more temporary, so there was no rush to remove these costs. This has left quite a large hole in overall profitability.

Mifid 2 – this EU directive changed the way in which research, information and opinions on financial products could be marketed, distributed and charged to institutional investors. Prior to Mifid, financial data products could be freely distributed to a very wide range of consumers with customers paying indirectly through transaction commissions or ad-hoc payments when a good service had been rendered. Mifid instead demanded formal, rigid client agreements between intermediaries and investment clients. This meant, in practice, that investors had to choose, allocate and, in effect, ration information/research budgets in advance and narrow their list of providers. In this process two of Euromoney’s star performers, BCA and Ned Davis, arguably the growth engines of the whole group, were hit hard seeing growth rates collapse from strongly double-digit annual percentages well into single figures.

Together, these were the driver of the near two-thirds collapse in EBIT after FY2019, from which Euromoney has not fully recovered. The ending of Covid may allow events to bounce back, but there is still, after two years, no clear strategy as to how the two research businesses will be able to restore old fortunes. Addressing these factors is important, but there is another, major, forward-looking issue that needs to be addressed. Data and/or Web 3.0.

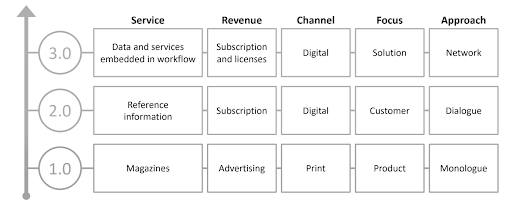

Data 3.0

While many will be familiar with the idea of Web 2.0 and, in turn, Business 2.0, a key part of Euromoney’s strategy has been to transition into a Data 3.0 business. So what is a 3.0 business? 2.0 is the current incarnation of internet data where interactivity, social connectivity, and user-generated content dominate and where ready-to-digest content is ‘pushed’ to users rather than being ‘pulled’, as was the case with the early internet. Mobile connectivity has been a powerful tool in the evolving and expanding the use of data. But, while there is some tailoring or focusing of content, a lot of data (especially for businesses) is still largely static and requires interpretation or manipulation having been ‘pulled’ by the end user: think the reams of UK government data that is readily available, but is static and is distributed through the data sets of numerous different agencies.

3.0 is built upon the core concepts of decentralisation, openness, greater user utility, artificial intelligence (AI), blockchain (and similar distributed ledger systems) and machine learning all of which threatens to be as disruptive as the explosions wrought by mobile connectivity, social media and powerful ‘push’ apps such as Facebook.

The evolution of business critical data

Source: Euromoney PLC

3.0 is listed as a core part of Euromoney’s strategy, but its approach seems to be one of evolution and investment in small bolt-ons bringing in new opaque data channels rather than the revolutionary shift to a 3.0 model that might be necessary. Buying dataset ownership in small businesses and trying to change how that data is sold (along with all of the existing data sets) most likely needs a much larger investment in a business that is already well-rooted in 3.0 delivery. This would almost certainly involve a more expensive move than the small or tens-of-millions that have been invested hitherto mainly widening the breadth of its data. Such an acquisition would most likely cost several hundred million but should perhaps be seen as the essential next step. The data that Euromoney controls has immense value but if it cannot be served to end users in new and evolving ways, its value and utility risk being diminished.

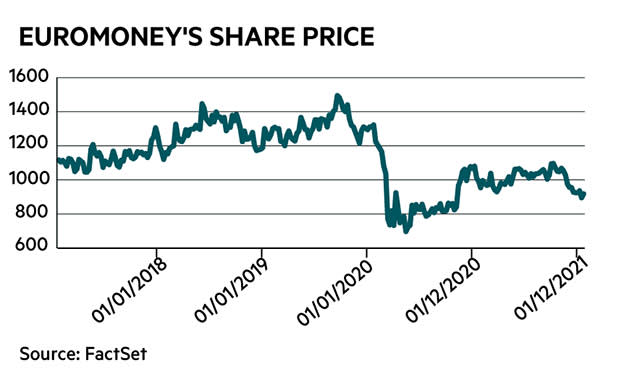

It may be that Euromoney cannot readily or quickly make the transition, but that should not diminish the value of its data and sources: it may just be that the whole business needs to be acquired by a technology giant to allow that to happen. Given the valuations that have recently been attached to large transactions within the B2B data provision industry (the recently announced Informa Business Intelligence unit sale rumoured to attract 22 times Ebitda or GlobalData’s recent purchase LMCA and LMCI at 19 times Ebitda for example) Euromoney could be an increasingly cheap target. The shares have de-rated 16 per cent in absolute terms and 20 per cent relative to the All-Share since the November full-year results and are still lower than immediate pre-Covid levels and 40 per cent below a pre-Covid peak of 1,500p. Its shares are trading on less than 11 times Ebitda.

What should investors do?

There does seem to be value to be unlocked here, but not without more substantial action first, be that internally or externally. The market looks to be sending out a clear signal, with valuations of similar businesses, that Euromoney perhaps ought be valued more highly but instead its value is dropping. As intimated above one of two things may need to happen to unlock value.

Euromoney probably needs to take a much larger step, accelerating or even leapfrogging its way to transition to 3.0. While there is some cash on the balance sheet, it only runs to tens-of-millions where hundreds would be needed, so substantial debt (manageable because there is very high cash conversion) or an equity issue might be needed. In this case 2 + 2 could equal five (or much more) and for the right deal shareholders should be willing to support any such move.

The alternative is to look for a bid to bring out the value of Euromoney’s data quality, audit/assurance, quality and trust into either a combination with a relative equal in the same space to pool costs of transition, or else see itself absorbed by an information giant such as S&P or Bloomberg. Investors would need to see independence lost but value created.

Today’s more piecemeal strategy of infrequent bolt-ons will struggle to add value and restore the rating of the business. We may be misreading the runes here, but when your specific circumstances seem to be improving and your market space is, in City parlance, ‘well bid’ yet your valuation is falling, something’s gotta give. Time for a new game plan – go big or go home.