Europe has been through some tough times over the past few years, but from an investment perspective it is now looking a lot more attractive.

Good long-term returns

Improving fundamentals in Europe

Smaller companies exposure

Experienced manager

Short-term underperformance

Volatility

While deflation has been a concern in the eurozone inflation is now coming through, at the same time as consumption is rising, employment numbers are improving and the economy has started to grow. Even more important for investors, companies seem to be in good shape. "First-quarter company reporting was encouraging to say the least," says Juliet Schooling Latter, director of research company FundCalibre. "Earnings upgrades were plentiful and, perhaps even more significantly, earnings expectations for the rest of the year are improving. This is a reversal of the trend we've seen for the past six years or so, when expectations declined rapidly over the course of each year."

While valuations are not as cheap as a few months ago following a good run for European equities, they still look better value compared with other developed equity markets and the eurozone bond market. And eurozone equities could receive a further boost. "With the possibility that the European Central Bank's (ECB) nine-year rate cutting cycle could soon be at an end and the bond-buying programme due to start tapering at the end of the year, an investor rotation from bonds to equities could be on the cards," explains Ms Schooling Latter.

A good way to get exposure to this could be Baring Europe Select Trust (GB00B7NB1W76). This aims for long-term capital growth from companies smaller than €5bn (£4.47bn), in particular mid-sized ones and some smaller ones. These tend to be more exposed to their domestic economies than large multi-nationals, so should be better placed to capture Europe's improving fundamentals and have the potential for stronger growth over the long term.

Baring Europe Select has beaten Euromoney Smaller European Companies (ex UK) Index over three years, and the Investment Association (IA) European Smaller Companies sector average over three and five years.

The fund's manager, Nicholas Williams, and Barings' European equity team try to exploit inefficiencies, aiming to identify mispriced stocks and niche opportunities. They look to add value in this under-researched area via market analysis and stock selection, picking companies according to their own merits rather than positioning the portfolio to reflect macroeconomic news. They favour companies whose strategic positioning and competitive strengths can drive sustained improvements in their profitability and returns. They also look for companies with well-established business franchises, proven managements and strong balance sheets.

Mr Williams has worked in investment for more than 20 years, a good part of which which he has spent running European smaller companies funds. "As well as beating the index fairly consistently, his defensive performance profile, which includes typically lower volatility than the benchmark and a degree of protection from falling markets, shows that his risk-averse approach is paying off," say analysts at wealth manager Tilney Group.

Political risks remain in Europe, for example with elections in Germany coming up, and withdrawal of quantitative easing could cause European equity market volatility.

Smaller companies can be volatile and higher risk than larger companies, as has been the case at times with this fund's returns. Baring Europe Select Trust’s managers run it via what is known as a growth at a reasonable price (Garp) basis, so look to buy growth stocks at the right price rather than cheap stocks. This means the fund tends to underperform in momentum or rapidly rising markets, when stock fundamentals are less important.

However, by focusing on quality companies it gets exposure to smaller companies in a relatively lower risk way, and its managers dilute risk by holding a large number of stocks - currently 107 – so no one holding can dominate performance. The fund also has a higher weighting to mid caps than smaller companies relative to many of its sector peers.

And regardless of shorter-term influences, over the long term – the period over which you should hold higher-risk assets such as overseas smaller companies – this fund has made strong returns.

So if you want to tap into Europe's potential and a fund that has proven its ability to make good long-term returns, Baring Europe Select Trust looks like a good way to capture growth. Buy.

| BARING EUROPE SELECT TRUST (GB00B7NB1W76) | |||

| PRICE: | 3935p | MEAN RETURN: | 20.00% |

| IA SECTOR: | European Smaller Companies | SHARPE RATIO: | 1.65 |

| FUND TYPE: | Unit trust | STANDARD DEVIATION: | 10.84% |

| FUND SIZE: | £2.06bn | ONGOING CHARGE: | 0.81% |

| No OF HOLDINGS: | 107* | YIELD: | 1.00% |

| SET-UP DATE: | 31 August 1984* | MORE DETAILS: | barings.com |

| MANAGER START DATE: | 31 October 2004 | ||

| Source: Morningstar & *Barings |

| Performance |

| 1-year total return (%) | 3-year cumulative total return (%) | 5-year cumulative total return (%) | |

| Baring Europe Select | 30.49 | 80.80 | 174.17 |

| Euromoney Smaller Europe Ex UK TR index | 34.30 | 65.18 | 174.43 |

| IA European Smaller Companies sector average | 30.63 | 64.01 | 140.34 |

| IA Europe Excluding UK sector average | 26.62 | 49.25 | 114.20 |

| Source: Morningstar, as at 21 July 2017 |

| Top 10 holdings as at 30 June 2017 (%) |

| Recordati | 1.6 |

| Temenos | 1.6 |

| DSV | 1.5 |

| Elior | 1.5 |

| IMCD | 1.5 |

| ASM International | 1.5 |

| SPIE | 1.5 |

| Christian Hansen | 1.5 |

| Euronext | 1.5 |

| TRYG | 1.4 |

| Source: Barings |

| Geographic breakdown (%) |

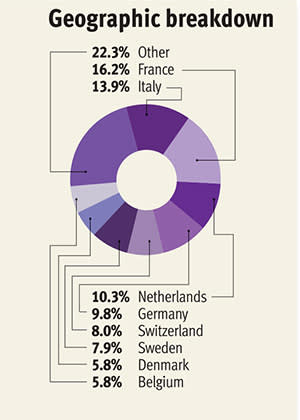

| France | 16.2 |

| Italy | 13.9 |

| Netherlands | 10.3 |

| Germany | 9.8 |

| Switzerland | 8.0 |

| Sweden | 7.9 |

| Denmark | 5.8 |

| Belgium | 5.8 |

| Finland | 5.6 |

| Other | 16.6 |