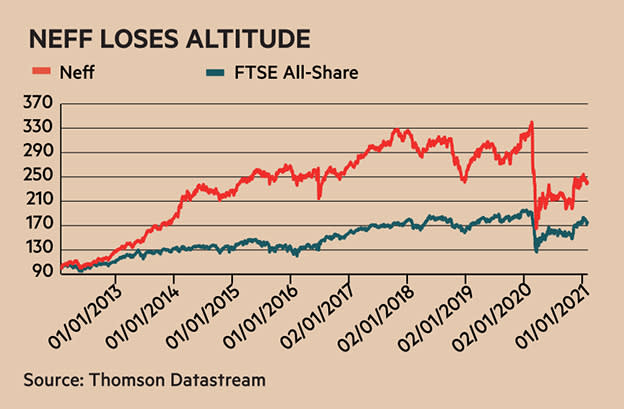

- The last 12 months have been an annus horribilis for my Neff-inspired screen.

- Cyclical picks came back to bite.

- The screen still shows solid outperformance since inception nine years ago.

- Growth characteristics of many of the 2021 picks look better than has been the case for a number of years.

My screen based on the investment approach of great American fund manager John Neff has had an annus horribilis. Besides some specific causes for the calamitous performance, I think the torrid showing may tell us something about the difficulties of looking for cheap growth stocks after a long bull market.

Before getting on to my more general observation about the terrible 12 months, it is worth highlighting one specific factor. I present warts-and-all results from stock screens in this column. So it was last year that NMC was included in the results but with my writing a risk warning into the accompanying article. At the time NMC had been the subject of a withering short report and later fraud was indeed uncovered.

But the more general observation about last year’s picks is that most had distinctly cyclical characteristics. Their businesses were all sensitive to economic shocks. So while they appeared to be solid growth plays based on the reported numbers stretching back several years, this reflected a long period of buoyant end markets. This happy situation came to a crushing end with lockdown.

12-MONTH PERFORMANCE

| Name | TIDM | Total return (11 Feb 2020 - 3 Feb 2021) |

| PageGroup | PAGE | -2.6% |

| Big Yellow | BYG | -3.6% |

| Legal & General | LGEN | -12% |

| Moneysupermarket | MONY | -17% |

| Barratt Developments | BDEV | -19% |

| Macfarlane | MACF | -21% |

| Unite | UTG | -29% |

| Vistry | VTY | -38% |

| NMC Health | NMC | -100% |

| FTSE All-Share | - | -8.5% |

| Neff | - | -27% |

Source: Thomson Datastream

Hunting for underpriced growth with this screen has proved most productive at earlier stages in bull markets. Over recent years the strategy has tended to identify low-quality, cyclical growth, which has a low rating attached to it for good reason. Early in a bull market, even when cyclicals are wrongly identified as genuine growth plays, they may still have some way to run as economic conditions continue to improve.

Still, over the full nine years I have run my Neff-inspired screen it has produced decent outperformance. The cumulative total return over the period stands at 139 per cent compared with 75 per cent from the FTSE All-Share. The screen is meant to provide ideas for further research rather than an off-the-shelf portfolio, so if I factor in a 1 per cent annual dealing charge the return drops to 119 per cent.

The screen’s criteria are:

■ Historic PE ratio below the most expensive quarter of shares and above the cheapest 15 per cent.

■ A lower than median average Neff PE ratio.

Neff PE = PE / Average of five-year compound annual EPS growth rate (five-year EPS CAGR) and forecast two-year average growth, plus dividend yield (DY)

■ A five-year EPS compound annual growth rate (CAGR) of more than 7.5 per cent but below 20 per cent (excessive growth can fall away).

■ Average forecast EPS growth for the next two financial years of more than 7.5 per cent.

■ Rising EPS in each of the past two half-year periods.

■ Five-year turnover CAGR of 5 per cent or more (in the long term, earnings growth needs to be based on rising sales).

■ Positive free cash flow in each of the past three years.

Only one share passed all the screen’s tests this year, Clipper Logistics. I’ve taken a look at the investment case below. Another five shares passed a weakened version of the screen that insists the valuation test is met but allows one of the other tests to be failed. Details of these shares are included in the table.

From the six shares, trading at both IG and CMC is very sensitive to market volatility. This means the consistency of growth is unreliable. But the other picks actually look an interesting selection. Arguably, as a bunch they represent higher-quality growth than many of the picks highlighted by the screen over recent years.

That said, an exceptional period of growth for some of these companies caused by lockdown or forecasts for the expected post-lockdown recovery, is feeding into the apparent cheapness identified by the Neff PE. Such high levels of growth will be fleeting.

SIX CHEAP GROWTH SHARES

| TEST FAILED | Name | TIDM | Mkt cap | Net cash / debt (-)* | Price | Neff PE | Fwd PE (+12mths) | Fwd DY (+12mths) | FCF yld (+12mths) | Fwd EPS grth FY+1 | Fwd EPS grth FY+2 | 3-mth fwd EPS change% | 3-mth mom |

| NA | Clipper Logistics | CLG | £565m | -£189m | 555p | 1.2 | 22 | 2.5% | 3.2% | 43% | 17% | 9.4% | 18.6% |

| EPS grth | CMC Mkts. | CMCX | £1,233m | £156m | 424p | 0.4 | 15 | 3.3% | 8.4% | 86% | -57% | 18.5% | 28.3% |

| EPS grth | B&M Euro. Value Retail | BME | £5,612m | -£1,626m | 561p | 0.5 | 17 | 3.5% | 9.1% | 99% | -13% | 13.6% | 11.5% |

| EPS grth | GCP Student Living | DIGS | £649m | -£231m | 143p | 0.8 | 33 | 2.8% | - | -50% | 111% | -30.5% | 28.5% |

| Fwd EPS grth | IG Group | IGG | £2,868m | £456m | 775p | 1.0 | 12 | 5.6% | 8.3% | 11% | -15% | 24.2% | 1.4% |

| FCF | Cranswick | CWK | £1,809m | -£122m | 3,438p | 1.8 | 19 | 2.0% | 4.4% | 16% | 2% | 3.1% | 3.3% |

Source: FactSet

*Foreign FX converted to £

CLIPPER LOGISTICS

Lockdown has been amazing for Clipper Logistics’ (CLG) business. The company offers an end-to-end logistics service for retailers in the UK and it also has small operations in Germany and Poland.

It generates 70 per cent of its logistics revenue from e-fulfilment. It offers these customers everything from taking receipt of stock at warehouses, storage, product picking, packaging, delivery, returns, repairs and disposal. Lockdown has substantially boosted online shopping, which was reflected in 34 per cent growth in Clipper’s first-half e-fulfilment revenues. The company reckons a permanent shift has happened that has accelerated the pre-existing e-commerce growth trend by three to five years.

Clipper’s bricks-and-mortar retail distribution business has also been doing well. Its first-half sales were up 9 per cent. Meanwhile, its new-and-used commercial vehicles sales operation, while an extremely small contributor to overall earnings, saw profits double in the first half thanks to improved dealer incentives and cost-cutting.

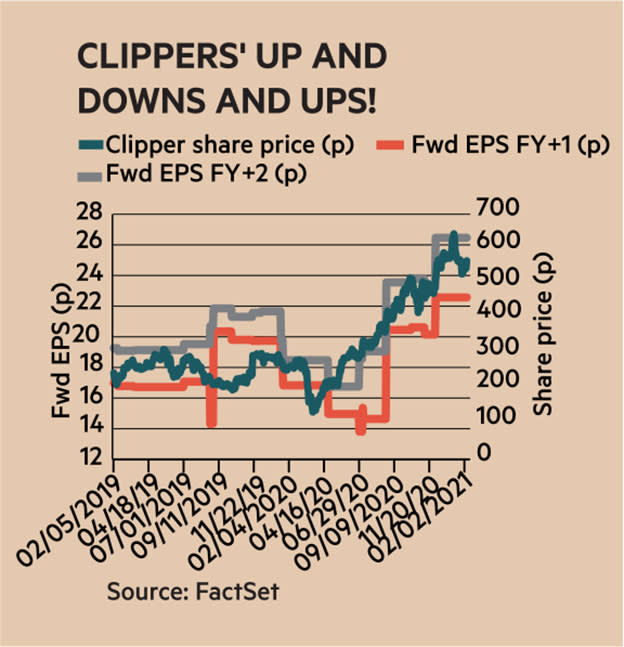

Brokers have been struggling to keep pace with progress. There have been a string of forecast-earnings upgrades since the lockdowns began.

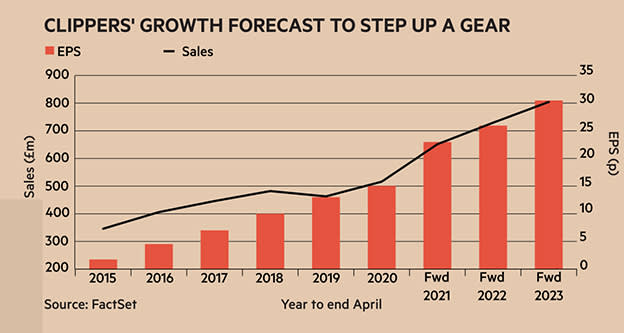

While Clipper is experiencing an extremely strong trading period, the longer-term record is also good, as illustrated by the accompanying chart of reported sales and EPS since IPO in 2014. The focus on e-fulfilment has played no small part in the success. Clipper also targets clients in growth areas; particularly fast fashion, and it has also been winning business in beauty and luxury retail. Acquisitions have helped growth and the company’s solid finances means it looks well set to do more deals. Half-year net debt was just £24m, ignoring lease liabilities.

While logistics is not high-margin work, Clipper’s e-fulfilment market leadership puts it in a strong position. It delivers around 500m units a year from 52 sites occupying 11m square feet of warehouse space. Not only does this scale mean it can create efficiencies and better serve national accounts, it also allows it to innovate. Many innovations are undertaken in collaboration with customers, which helps to strengthen relationships. Recent examples include introducing warehouse robots with SuperDry and rolling out in-warehouse white-goods repairs with Argos.

Other 'value-added' services include checks that returned clothes are 'floor ready' (often garments are cheekily worn before being sent back!) and making sure labels comply with the correct jurisdiction; a particular consideration following Brexit. The company also offers services to help retailers improve sustainability.

An impressive record of customers wins underscores the fact the company seems to be making the right moves. So too does its long-term relationships with big retailers such as Asos (ASC) and Morrisons Supermarkets (MRW).

Logistics businesses need a lot of capital to function. While Clipper mainly leases its assets, this does not make it an exception to the rule, although it does reduce the upfront investment needed for growth. The company has sizeable lease-payment liabilities (£185m at the half-year stage) and very large working capital items (half-year receivables of £124m and payables of £159m) relative to its profits (£34m of operating profits over the last 12 months). At a time when many retailers have been going under, this could be a concern.

However, the company’s model does build in some resilience. One big plus is that the majority of contracts (70 per cent) operate on a cost-plus basis. This is where all costs, including much capital expenditure, is paid by the client plus a margin. This removes the risk of Clipper having to cover the fixed costs associated with maintaining a warehouse when activity is depressed. Many of its other contracts require clients to agree to pay a fee based on an agreed minimum volume. In total, 94 per cent of contracts have guaranteed terms.

The nature of these contracts means revenues are often reported ahead of being billed and before money is collected. This creates the risk that a client will be unable to pay up, or will dispute the billing estimates.

But Clipper does not have too much exposure to any one client, with the top five accounting for less than 15 per cent of underlying profit last year. Protection from bad debt is also offered by Clipper’s claim on clients’ inventories should there be a problem. Meanwhile, its four commercial-vehicle dealerships offer a means to manage any onerous-lease liabilities connected to vehicles. And given the focus on e-commerce, it seems likely it would not take very long for Clipper to fill any leased warehouse space that came free.

These factors do not eliminate risk, but they are reasons to feel reassured. What’s more, while the value of working capital items are high relative to profits, which means small percentage movements can have a big impact on cash flows, net working capital tends to be teeny or negative. Based on full-year numbers, the amount the company owed in the form of 'payables' (unpaid suppliers, early payments by customers, etc) at £131m, matched amounts owed to it as receivables plus inventory. As long as such balance is maintained, it means negligible investment is needed in working capital to grow. This underpins the company’s record for cash conversion.

While the Neff screen looks for value based on the Neff PE, Clipper looks expensive compared with its history based on a traditional price/earnings (PE) ratio. Meanwhile, the high level of forecast earnings growth that feeds into the valuation is not expected to be sustained.

That said, with an enterprise value of 1.4 times last 12-months sales, the company’s valuation sits at around its pre-crisis level; although this was the historic peak. A forecast free cash flow (FCF) yield of about 3 per cent (FCF expected in the next 12 months as a percentage of enterprise value) also does not look too stretched to me given the sunny growth outlook. True, there are cyclical risks as well as the balance sheet consideration already discussed. But with a continued fair wind, at the current price the shares should still be able to do well despite having doubled over the last year.