- Shares trade at a discount to the wider sector

- The stamp duty break and pent-up demand have led to a bounceback in completion levels

- Strong demand has resulted in a net cash position and the reinstatement of dividends

- Shares trade at discount to sector

- Net cash balance

- Dividends reinstated

- Earnings in recovery

- Stamp duty break uncertainty

- Investment needed to rebuild outlet numbers

The blistering surge in housing market activity is a reality few would have predicted as the pandemic took hold in March last year. Yet a sharp rise in demand and supressed supply translated into the highest rate of sales price growth since August 2007, according to the Office for National Statistics.

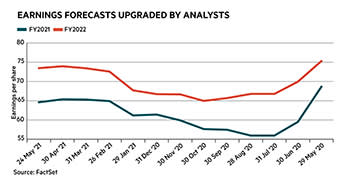

For the UK’s listed housebuilders, the buoyant market has led to a quick recovery in completions and strong forward order books. Analysts have put through a slew of upgrades to earnings forecasts for 2021 and 2022 for most of the sector’s major players. That includes Redrow (RDW).

Like peers, the mid-cap housebuilder has benefited from the stamp duty break on properties valued at up to £500,000, pent-up demand following the first lockdown and a rush to beat the end of the first Help-to-Buy scheme in March.

Pandemic bounceback

The recovery in completions since the first lockdown in March last year has been stellar. During the six months to the end of December, the group posted a record annual jump in legal completions of a fifth and a corresponding boost to revenue.

The high level of work in progress brought forward into completions during the six-month period also meant a net debt position of £126m was converted into a net cash balance of £238m. The dividend was accordingly reinstated at 6p a share, with a total payment of 19.5p forecast for 2021.

That followed a 2020 financial year when completions plunged 37 per cent, which, combined with a £17m provision for costs associated with its exit from London, meant pre-tax profits declined by two-thirds.

Given the stamp duty holiday was extended to the end of June and will be tapered to £250,000 until the end of September, there is a strong chance that the elevated level of demand will continue until the end of Redrow’s 2021 financial year on 30 June. However, in September, executive chairman John Tutte – who is due to retire on 1 June – warned that the exceptionally high level of demand would likely fall back slightly once the tax break came to an end.

The big question is just where sales rates will settle. Analysts are forecasting a gradual return to more normal levels of sales and pre-tax profits in coming years, broadly reaching the 2019 level by 2024. The analyst consensus pre-tax profit forecast for 2021 stands at £278m, almost double last year’s figure. That reflects a December order book that was 8 per cent higher than the same time in 2020 at £.1.3bn, 72 per cent of which is contracted. The group is also 95 per cent forward sold for the current financial year.

Sales prices are also expected to hold up well. The average price is forecast to be marginally higher than the 2019 level over the next four years, according to analyst consensus. That reflects more optimistic expectations for the market across the industry. Savills (SVS) has upgraded forecasts for average UK house price growth this year to 4 per cent, rising to 5 per cent next year. Earnings forecasts of 64.6p a share for 2021 and 73.5p for 2022 are the culmination of upgrades of 12 per cent since the end of September.

The group’s pre-pandemic profitability should also offer investors encouragement. The operating margin came in at around 20 per cent during the four years to 2019 and it posted a return on equity at the 21/22 per cent-mark during each of those years. That is in the same ballpark as more highly-valued peers such as Bellway (BWY) and Taylor Wimpey (TW.).

Management has guided towards an operating margin of 15.5 per cent this year, reflecting a higher proportion of revenue from affordable homes and lower margins on almost all London sites, including two private rented sector contracts.

London exit

Last year Redrow announced plans to scale back its London exposure to the flagship Colindale Gardens development alone. Management cited increasing challenges to returns including weak overseas demand and more buyers seeking to live and work outside the city. Indeed, even amid the housing market boom of the past 10 months, the capital has trailed the rest of the country in terms of sales price growth. At the half-year point, it had exited four of the six sites not already being built on and expects to exit the remaining two before the end of the financial year.

It is now tasked with replacing sites relinquished in the capital by purchasing more land in the regions. During the second half of 2020, the group returned to the land buying market, adding 2,284 plots with planning permission. Increasing land investment means management expects to close the financial year with a lower net cash balance than at the end of December, but has said it should remain above £100m.

Analysts at Berenberg argue that driving regional growth will require more capital to be retained and ploughed into new land. Could that hold back the amount of cash available to distribute to shareholders? The forecast increase in dividends between 2021 and 2024 is lower than ordinary payments made between 2016 and 2019.

Help-to-Buy uncertainty?

The stamp duty break is not the only stimulus measure that has both turbo-charged completions but also complicated sales forecasts. On 1 April the Help-to-Buy scheme was restricted to first-time buyers and regional sales price caps were imposed, which naturally sparked concerns of a fall in completions across the sector. Those using the scheme accounted for 44 per cent of Redrow's completions during the latter six months of 2020, as buyers rushed to take advantage of the scheme.

Redrow investors may have reason for confidence, though. A higher private average sales price of around £387,000 means the group tends to target second movers, who have already built up some equity to put towards buying a home. In February, management said it had not seen any changes to the overall rate of reservations ahead of the March deadline. In an indication of resilient demand, £750m of the £1.3bn order book at the end of December related to completions due beyond the end of the first Help-to-Buy scheme. Management expects the proportion of completions using the 2021-2023 scheme to settle at around half of historic levels, which would be equivalent to between 15 and 20 per cent.

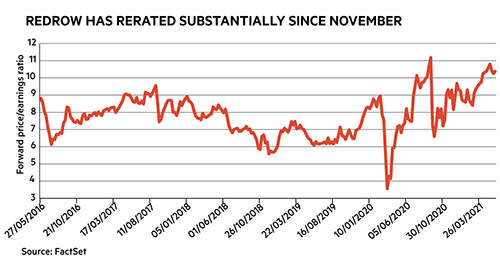

In line with the rest of the sector, Redrow has been boosted by the broader rally in previously depressed shares since news of vaccine success in November. The shares have risen by almost half over the past 12 months and now trade at a price/net asset value ratio of 1.2, based upon consensus forecasts for June, and a forward price/earnings ratio of 10. Based upon both of those metrics, Redrow is more lowly rated than all its UK-listed peers. A history of delivering impressive returns and solid progress on rebuilding completion levels and margins means that does not seem justified.

Last IC view: Buy, 446p, 16 Sep 2020

| REDROW (RDW) | ||||

| ORD PRICE: | 663p | MARKET VALUE: | £2.34bn | |

| TOUCH: | 662.4-662.8p | 12-MONTH HIGH: | 721p | LOW: 352p |

| FORWARD DIVIDEND YIELD: | 3.5% | FORWARD PE RATIO: | 10 | |

| NET ASSET VALUE: | 503p | NET CASH: | £238m | |

| Year to 30 Jun | Turnover (£bn) | Pre-tax profit (£m)* | Earnings per share (p)* | Dividend per share (p) |

| 2018 | 1.92 | 380 | 85.3 | 28 |

| 2019 | 2.11 | 406 | 92.3 | 60.5 |

| 2020 | 1.34 | 140 | 32.9 | nil |

| 2021* | 1.80 | 261 | 61.7 | 15.4 |

| 2022* | 1.89 | 295 | 69.7 | 23 |

| % change | +5 | +13 | +13 | +49 |

| NMS: | ||||

| Market Makers: | ||||

| Beta: | 1.51 | |||

| *Berenberg forecasts, adjusted PTP and EPS figures | ||||