The business of checking people’s credit histories has become a ubiquitous part of modern life. Anyone who has inadvertently missed a credit card payment or put the cheque for the gas bill late in the post – admittedly this is going back a bit – can testify to the impact that such minor lapses can have on a credit rating.

- ecommerce has given Experian a boost

- Large presence in new markets

- High operational gearing

- Attractive peer valuation

- Regular legal and regulatory issues

What's more, while some countries, Denmark is a notable example, have no history of credit checks, they are an increasingly important part of life in the UK and the US. Credit checks for loan applications are considered routine, as well as for securing a rental contract, but some professions must also check the creditworthiness of potential employees, particularly firms such as solicitors who enter a limited liability corporate structure and are technically self-employed. So, where a need exists, the market will provide and credit checking company Experian (EXPN) has experienced phenomenal growth on the back of a broadening system of background checks.

Gaining access to credit reports has been easier in the UK since the last coalition government brought in a system of basic access for a nominal £2 fee. The effect has been to democratise the process and create a corresponding market for credit checks that has expanded rapidly. The US market is also thriving. Here, Experian holds data on 235m individual consumers and 25m businesses and covers everything from consumer lending to business analytics and legal compliance.

The company has also been a noticeably expanding presence in Brazil and Latin America where annual sales of $732m (£552m) are starting to closely match those in the UK & Ireland market.

The pandemic has helped to accelerate ecommerce trends in Experian’s developed markets, but the development of different types of credit has also created a natural demand for its services. For example, the expansion of 'buy now pay later', is a case of the market generating new opportunities for the likes of Experian to exploit, while at the same time proving to be an easy way for consumers to improve (or ruin) their credit scores.

Legal and regulatory

The downside with Experian tends to be the rate at which it runs into regulatory problems. Part of this is inherent to the sector as the company operates in a highly regulated market, but one where the rules, particularly on money laundering and data handling, are constantly changing. On the one hand, this gives Experian further openings to offer clients advice on new regulation and, on the other, it can sometimes become ensnared by them. The company’s accounts list a series of actions in Latin America and the UK related to either tax issues or data protection violations. Data protection problems, particularly after a major hack at competitor Equifax in 2017, have produced ever tighter restrictions on the handling and use of personal data, which at times has restricted Experian’s profitability, although also increased barriers to competition. While legal issues are unlikely to be material to Experian, they will inevitably surface given the nature of its business.

There is also the question of whether the company has options for growth in its core credit-checking business – such is Experian’s size and market dominance that regulators are unlikely to wave through acquisitions, which is why Experian pulled out of the £275m purchase of Clearscore in 2019 after doubts about market competition were raised. This leaves the company with organic growth dependent on the rate at which it can win new business. Therefore, it must expand its other interests to grow the top line and analysts cite the development of risk-management, as a service for financial institutions, which could be quickly developed on the back of its analytics and database businesses.

The key financials

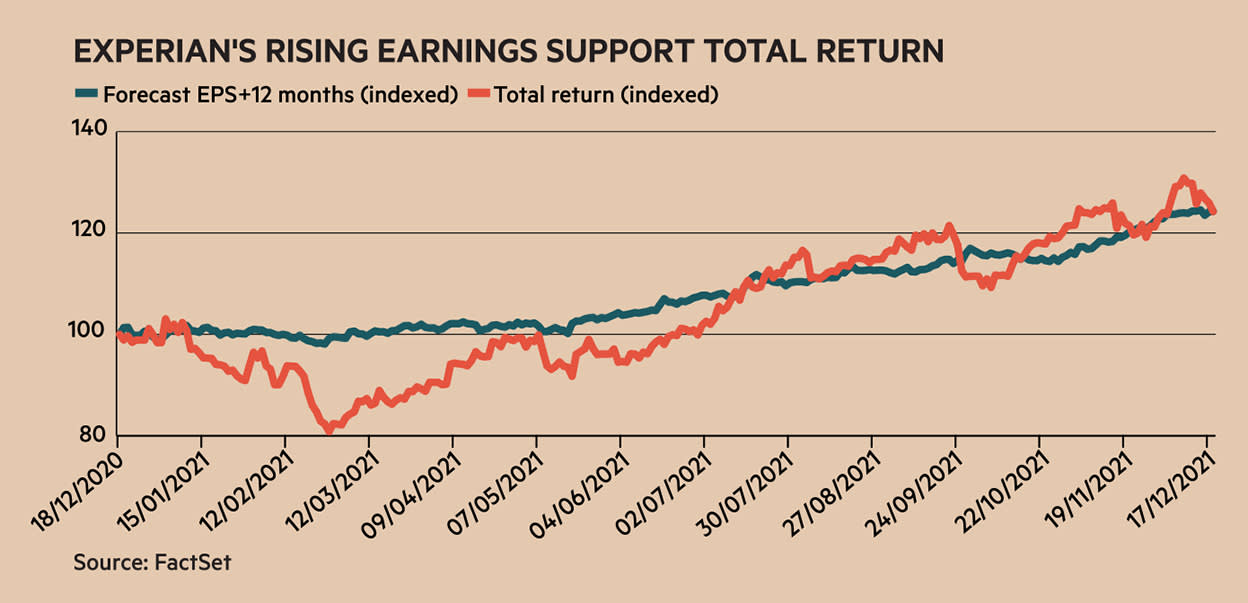

Experian’s greatest attraction for investors is the extent to which growth produces increased profits thanks to a high proportion of fixed costs. The current return on capital employed of 18 per cent compares favourably with other high-quality companies and reflects the capital-light nature of the business. This helps cash to flow quickly from profits and Experian expects to achieve at least 100 per cent operating cash conversion this year, with a majority of the cash run-rate occurring during the traditionally stronger second half.

Experian also has an impressive free cash flow margin, and matched a five-year high of 18 per cent at the last annual results. In addition, the company has been managing its balance sheet to free up liquidity; in 2020 it raised $400m in a bond sale. While the current ratio (current assets to current liabilities) is a nothing special 0.6, the net gearing is in line with its long-term average and debt to capital is only 52 per cent.

Competition looms in the form of US giant Equifax (NYSE:EFX) in direct consumer credit scoring, plus others who focus more on business analytics and services, including the likes of ThomsonReuters. Compared with most US competitors, Experian trades at a decent discount to its rivals, while generating better returns overall on its invested capital (see table). This illustrates the basic cheapness of UK equities when compared with their US equivalents, in that peer valuations appear to be out of sync despite the companies operating in broadly similar segments within the same markets. It is a valuation trend that has not gone unnoticed by professional fund managers with an interest in quality shares. For example, in October 2020, fund manager Lindsell Train took a large position in Experian shortly after the shares touched a year-high that September.

| Name | TIDM | Price | Market Cap. (bn) | %chg YTD | PE ratio | PEG ratio | Price to NAV | Yield (%) | Dividend Cover | EBIT margin (%) | FCF margin (%) | ROCE (%) |

| Fair Isaac Corp | FICO | 41,249¢ | $11.2 | -19.3 | 38.2 | 1.2 | -102.5 | nil | nil | 32 | 31.6 | 33.1 |

| Experian PLC | EXPN | 3,475p | £32.0 | 25.1 | 45.5 | 2.4 | 13.8 | 1 | 2.2 | 25.8 | 18.8 | 17.9 |

| Equifax Inc | EFX | 27,679¢ | $33.7 | 43.4 | 65.3 | 0.8 | 10.6 | 0.6 | 2.7 | 20 | 12.7 | 11.2 |

| TransUnion | TRU | 110,74¢ | $21.1 | 11.6 | 60.9 | 0.6 | 8.3 | 0.3 | 6.1 | 21.7 | 21.1 | 8.8 |

| Dun & Bradstreet Inc | DNB | 1,955¢ | $8.45 | -21.5 | 20.6 | 1.8 | 2.3 | nil | nil | 6.9 | 4.3 | 1.4 |

| *Source FactSet | ||||||||||||

In short, Experian embodies genuine quality of earnings within a business that has high barriers to entry and which is essential no matter what stage we find ourselves in the economic cycle. Buy.

| Company Details | Name | Mkt Cap | Price | 52-Wk Hi/Lo |

| Experian (EXPN) | £32.4bn | 3,513p | 3,674p / 2,265p | |

| Size/Debt | NAV per share* | Net Cash / Debt(-)* | Net Debt / Ebitda | Op Cash/ Ebitda |

| 248p | -£3.22bn | 2.1 x | 93% |

| Valuation | Fwd PE (+12mths) | Fwd DY (+12mths) | FCF yld (+12mths) | PEG |

| 34 | 1.2% | 3.1% | 1.9 | |

| Quality/ Growth | EBIT Margin | ROCE | 5yr Sales CAGR | 5yr EPS CAGR |

| 23.3% | 17.8% | 7.9% | 5.0% | |

| Forecasts/ Momentum | Fwd EPS grth NTM | Fwd EPS grth STM | 3-mth Mom | 3-mth Fwd EPS change% |

| 17.0% | 12% | 6.1% | 9.3% |

| Year End 31 Mar | Sales ($bn) | Profit before tax ($bn) | EPS (c) | DPS (p) |

| 2019 | 4.86 | 1.14 | 97 | 36.1 |

| 2020 | 5.18 | 1.16 | 74 | 38.3 |

| 2021 | 5.37 | 1.23 | 102 | 33.7 |

| f'cst 2022 | 6.20 | 1.51 | 123 | 41.0 |

| f'cst 2023 | 6.78 | 1.71 | 140 | 44.7 |

| chg (%) | +9 | +13 | +14 | +9 |

| Source: FactSet, adjusted PTP and EPS figures converted to £ | ||||

| NTM = Next 12 months | ||||

| STM = Second 12 months (ie, one year from now) | ||||

| *Converted to £, includes intangible assets of £913m, or 574p a share | ||||