The UK economy is facing enormous upheaval as the country goes into lockdown. Public spaces have shut and individuals are being forced to stay at home. Those on zero-hours contracts, especially in the retail, leisure and hospitality sectors are facing job losses. Companies are looking at a severe fall in revenue and catastrophic cuts to profits.

We have no idea how long this will last and the impact on the UK economy and individuals' personal finances is extremely concerning. All the while, we are facing a deadly enemy which is putting extraordinary pressure on our healthcare system.

The help being offered by the government should provide some respite to companies facing significant distress. But the measures being taken are extraordinary and add to concerns about what our economy might look like on the other side of this.

Personal finance and behaviour

Is panic selling making the crisis worse?

What should I do to protect my wealth?

To a certain extent, the market sell-offs of the past few weeks are reflective of social behaviour: we are influenced not just by reality, but also our belief in what others believe. Anticipating that others will be selling has driven many of us out of the market. Chris Dillow discusses this herd behaviour in a recent economics column. And you can become a subscriber today to read Mr Bearbull's discussion of the mathematics of market movement throughout history.

So, is your selling making things worse? Potentially – especially for yourself. Selling during a falling market is widely regarded as the most foolish course of action as it is a sure way of crystallising losses. But how about ignoring the panic completely (or as best you can)? Scientific studies have shown that we are programmed to heed good news and disregard bad news. This could be beneficial in times of turbulence, says Chris Dillow – read his economics column here.

It’s hard, but this is a time for cool heads and rational, dispassionate thinking. “We can’t change what will happen so taking a step back from the noise and trying to work out what to do with our savings and investments.” remains Phil Oakley’s aim amid the carnage.

Sign up to our Alpha premium service to read Phil's tips for retaining a level head.

Macroeconomic policy

- What is monetary policy?

- Can an interest rate cut really ease pressure on the economy in times of crisis?

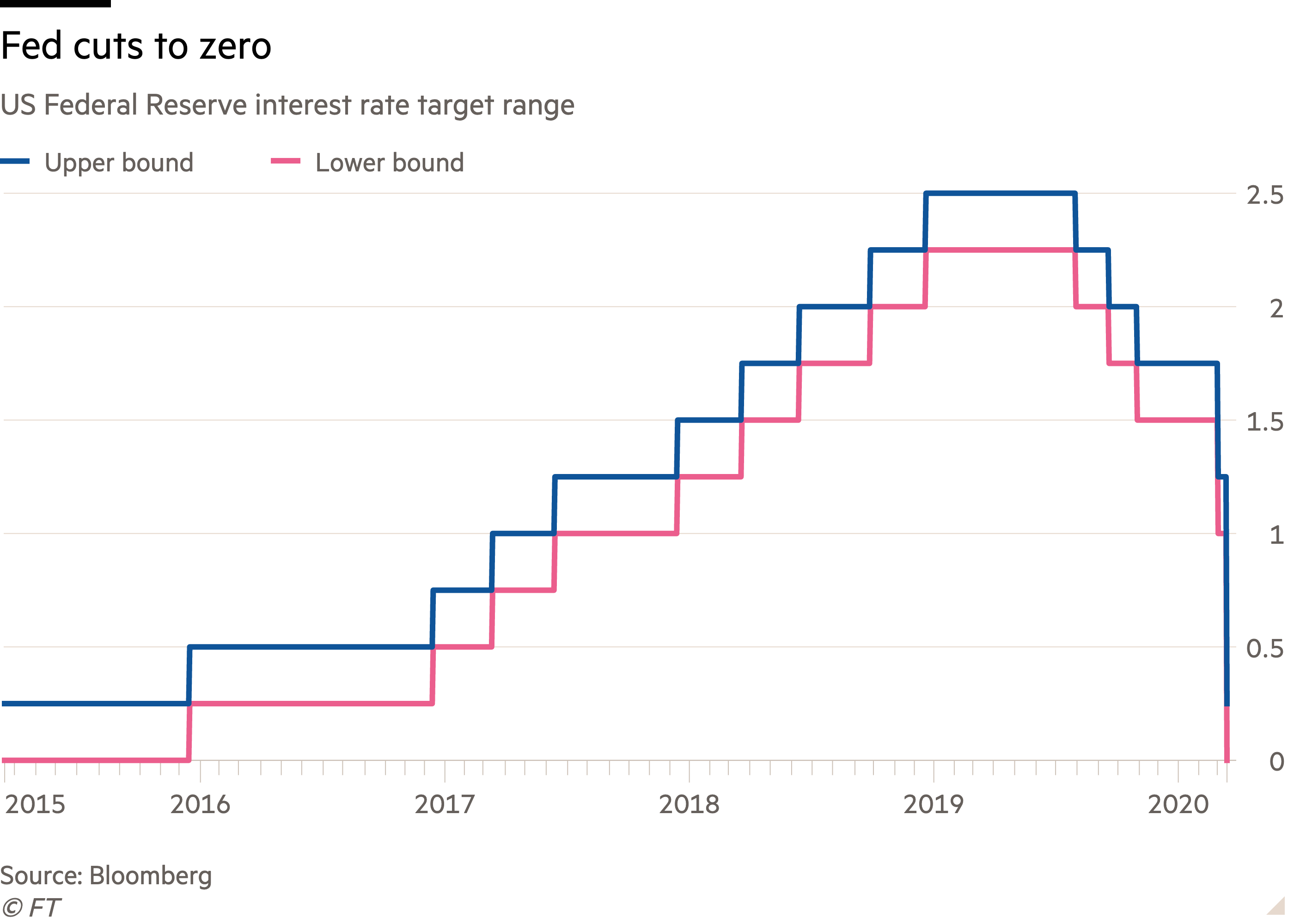

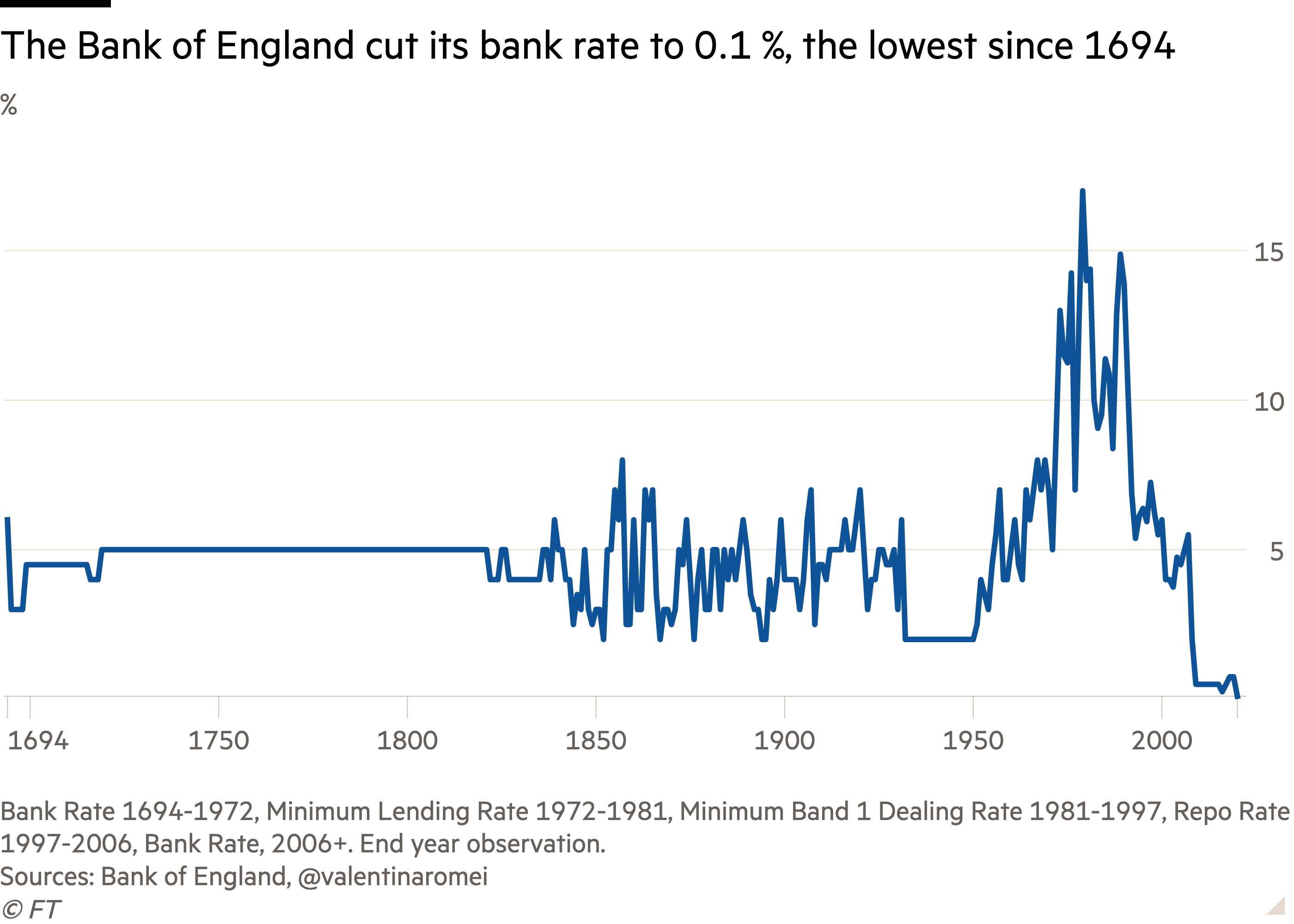

On 11 March, the Bank of England announced an emergency cut in interest rates from 0.75 per cent to 0.25 per cent. This followed similar action from the Federal Reserve in the US, which has since cut its interest rate to zero. On 19 March, the UK central bank pushed interest rates to their lowest in history – 0.1 per cent.

Interest rate cuts are used as a way of stimulating economic activity for two key reasons. Firstly, spending is more attractive when you are getting so little interest on your savings. Secondly, companies can borrow money very cheaply, which they can then invest back into their own growth. Very low interest rates have been a major contributor to the huge economic growth enjoyed in the UK and US since the financial crisis.

The problem is that interest rates were already very low before the current challenges. Plus, the nature of the coronavirus crisis means people aren’t able to get out and spend, even if they wanted to. For a more in-depth overview of the limits of monetary policy, click here.

Still, the government thinks that the negligible interest rates might provide some respite for businesses facing unprecedented challenges, which will in turn help protect employment for millions of people. Some homeowners’ mortgage repayments will also be affected by the cut in base rates – those on tracker rates (which account for about 11 per cent of the outstanding mortgages in the UK) will immediately see their monthly repayments reduced.

Cash sitting in the bank is currently accumulating next to nothing. But Chris Dillow makes a new case for cash – it might not be the worst investment in these troubled times. Become a subscriber today to find out more.

Meanwhile, the Federal Reserve has turned on the taps full blast to help prop up the market. A $2trn fiscal stimulus package by Congress in addition to the Fed's promises to buy unlimted US Treasury bonds and expand its asset purchase scheme provided a kick for the S&P 500 on Tuesday, as James Norrington examines here.

UK government policy

Is lockdown really necessary?

Where is all the government spending coming from and will it have a long-term repercussion on the UK economy?

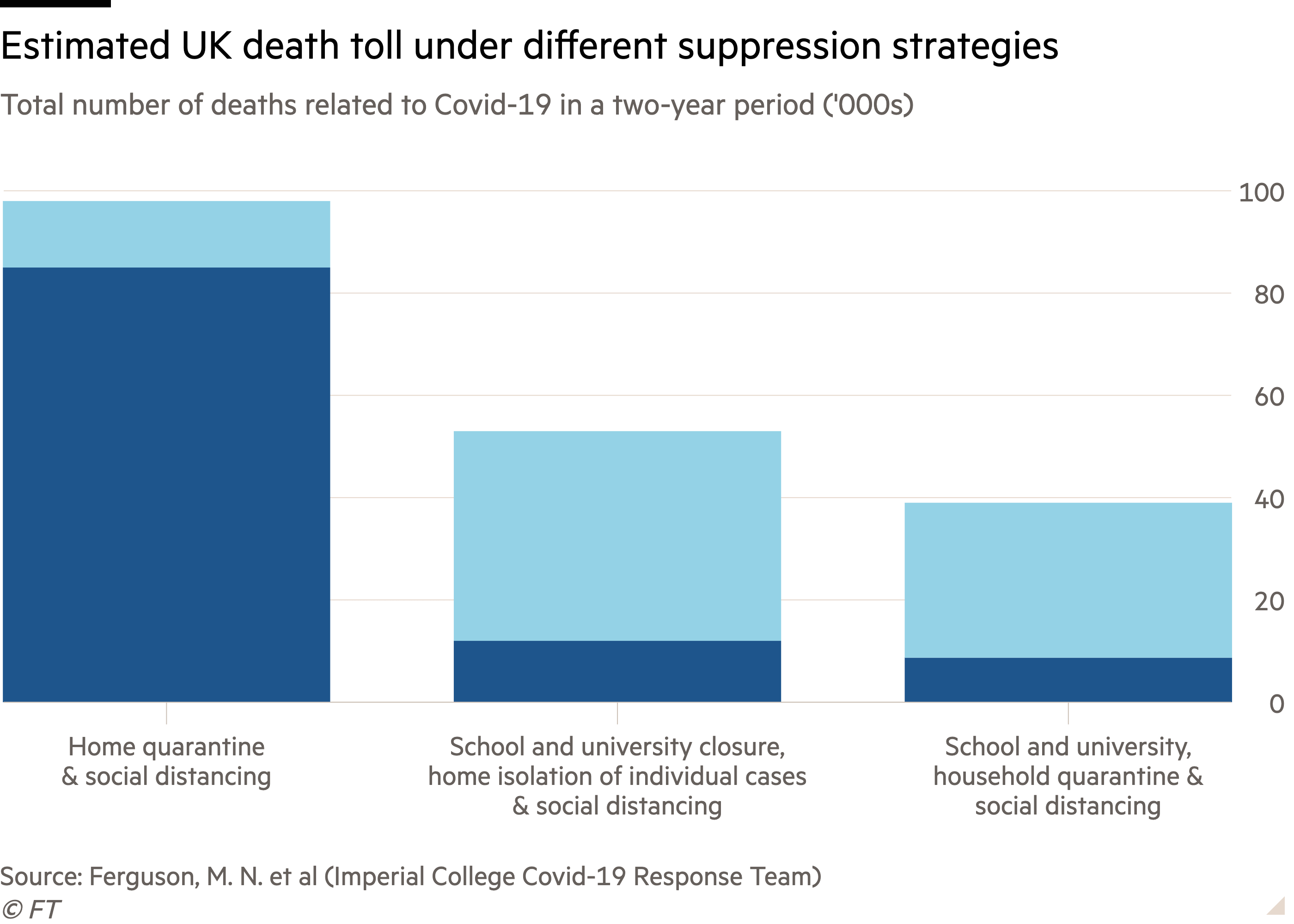

The number of deaths from coronavirus in the UK is rising exponentially, following a similar pattern to that of Italy. Enforcing the closure of public spaces should help mitigate the temptation of crowed venues. This is crucial if the UK wants to 'flatten the curve' and reduce the pace of coronavirus spread.

To reduce the burden on the businesses that are bearing the brunt of this enforced shutdown, the government has announced enormous spending. Chancellor Rishi Sunak has promised £350bn of government support for households and businesses. It will pay 80 per cent of salary for staff who are unable to work but kept on by their employer, covering wages of up to £2,500 a month.

Insurance and cover

What are my travel rights?

Who is on the hook for the costs of coronavirus?

Are the insurers going to pay out?

The coronavirus pandemic is now clearly an enormous threat to any travel plans this year, but as it is now classed as a known and foreseeable event, it can no longer be covered by insurance. Anyone booking a holiday now does so at their own risk. This doesn’t mean travel insurers will avoid an avalanche of claims.

Business interruption insurance presents another test for the industry. Until recently, the issue centred on the official classification of Covid-19 as a so-called ‘notifiable disease’, which was confirmed on 4 March. However, there is no consistent approach to the way insurance policies cover pandemic illness.

Business interruption insurance presents another test for the industry. Until recently, the issue centred on the official classification of Covid-19 as a so-called ‘notifiable disease’, which was confirmed on 4 March. However, there is no consistent approach to the way insurance policies cover pandemic illness.

Property and housing

What is happening to the property market?

What happens if I can't pay my rent?

Online estate agency Rightmove has confirmed that there has been a massive drop in house purchasing amid the coronavirus outbreak. The post-election bounce is fading rapidly as buyers and sellers reconsider their plans. With the country in lockdown, it’s unsurprising that viewings have dried up. As Emma Powell notes in her recent coverage of real estate services group Savills, investors and occupiers are grappling with severe uncertainty at the moment.

The fallout is having a knock-on impact on property investments via funds. Several asset managers have suspended trading in their open-ended property funds, citing “material uncertainty” about asset prices in the midst of the coronavirus lockdown.

Meanwhile, the government is doing what it can to ease the pressure on tennants who are facing several months without work or pay. Landlords have been offered an extension of three-month mortgage payment holidays for buy to let loans to prevent them from evicting tenants who run into financial difficulties, as Rosie Carr explains in more detail in this article. But buy to let landlords could be facing more pressing concerns as the price of their property falls, thus reducing their loan to value and forcing the property owner onto a far less generous mortgage deal than the ones currently being offered. In her article, Rosie explains the best course of action for buy to let landlords.

The pain facing commercial landlords is perhaps even more pressing. "In the wake of widespread closures of non-essential shops, pubs, restaurants and leisure facilities, landlords trying to predict the stability of rental income arguably face a tougher task than ever before," writes Emma Powell in her update of the commercial property market.

Health and science

Can our health service deal with the coronavirus?

The SARS-COV-2 virus which is causing the current outbreak of the Covid-19 disease is highly contagious and transmitted via water droplets. Worryingly, the illness is that it can be passed on by people who have not yet shown symptoms - indeed, some of the first patients diagnosed in both the UK and US had not come into contact with anyone who had been diagnosed with the illness.

Without effective diagnostics it is impossible to know how many people have had the illness and that has two major consequences: people have transmitted the disease without realising it; and the fatality rate (number of deaths divided by number of confirmed cases) is worryingly high. Diagnistics is one of the key components of an effective healthcare system, as we highlighted in our 2017 feature: Fixing the NHS.

The UK government is attempting to contain the disease by encouarging people to stay at home. If infection rates continue to mount as they have done in the last few weeks, the UK's national health service will face crushingly high demand. We need to "flatten the curve" and delay the spread of infection as much as possible while we await better diagnostics, medicines and, ultimately a vaccine. Become a subscriber to find out the progress being made by healthcare companies around the world in fighting the coronavirus outbreak.