- Governance is a hard quality to measure, but rating a company’s environmental and social impact is even more challenging

- Boohoo is not the only ‘green pioneer’ to face the wrath of the short sellers in 2020

Is there a greater corporate red flag than management who refuse to answer valid investor questions about the longevity of the business over which they preside? Those that are happy to send out PR representatives when pesky journalists come calling, but cannot find the time to explain how they plan to spend investors’ cash to grow the business.

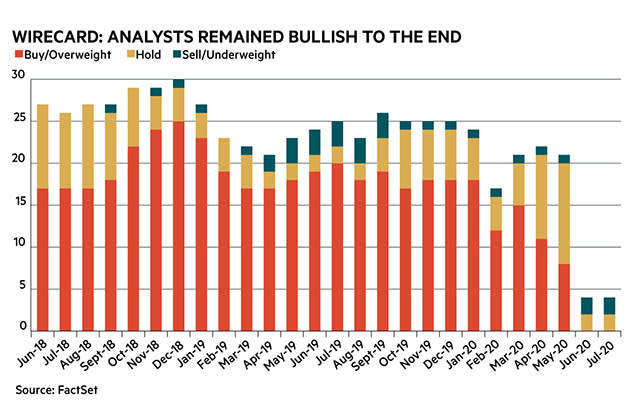

A carefully engineered management smokescreen was chief among the sins that contributed to the eventual unravelling of Wirecard earlier this year. When a Financial Times investigation in early 2019 found that an executive in the payment processor’s Asia-Pacific division had been suspected of using forged contracts, management plagued the journalists with legal threats and allegations of collusion. In June 2020, those journalists were vindicated when Wirecard’s auditor admitted that it could not locate €1.9bn of cash.

The case has stirred memories of Enron and Autonomy – both fraudulent companies whose management refused to answer legitimate concerns, while building an elaborate web of smoke and mirrors. Like Wirecard, their eventual exposure undermined faith in capital markets and regulators.

But if irresponsible management should send investors scarpering, the opposite is true of well-run businesses. Responsible management has long been a mark of truly excellent companies and it has become even more valuable amid the challenges posed by a global pandemic. But governance is hard to measure. In the UK, attempts to monitor responsible management have resulted in the box-checking corporate governance code, which regularly fails to identify poorly run companies. As Tim Martin, founder of JD Wetherspoon (JDW) and strong opponent of the UK’s corporate governance guidelines, points out, “[now defunct] companies like Northern Rock, HBOS and Carillion were compliant with the code.”

Mr Martin has reason to take umbrage with the corporate governance code. In 2019, Wetherspoons’ largest institutional investor voted against the re-appointment of a non-executive director simply because they had exceeded the nine-year limit on so-called independence as stated by the guidelines. At the time, Mr Martin argued that the code disillusions experienced executives from whom businesses have a lot to gain. “Adherence to a tick-box culture means, for example, that thereare no non-executives on the boards ofmajor UK banks who have any personal experience of the last banking crisis at their company,” he said.

The outspoken founder of Wetherspoons might seem a funny advocate of corporate governance – his brash business style means he is regularly held up as a symbol of wrongdoing in financial markets – but he presides over one of the UK’s most well-managed businesses; JD Wetherspoon ticks the corporate governance boxes which should actually matter to investors.

The board has an average tenure of 15 years and directors are required to maintain a minimum stake in the company. Staff, from top to bottom are incentivised by the performance of the company thanks to a generous share scheme, and Mr Martin is the biggest shareholder.

If governance is a hard quality to measure, rating a company’s environmental and social impact – the other two-thirds of hot investment style ESG – is even more challenging. In 2020, money has surged towards companies that claim good ESG credentials as investors speculate, probably correctly, that businesses that adhere to these principles have a promising future. In the nine months to September 2020, responsible investment funds saw net inflows of £7.1bn from UK retail investors, almost four times higher than the previous year.

But where the money flows, accusations of fraud follow and in 2020 there has been no shortage of examples of businesses claiming high ESG credentials with little merit. In the UK, the biggest culprit is arguably Boohoo (BOO). Fast fashion itself is an environmentally damaging industry and Boohoo has the added sin of cheap delivery and returns policies, which contribute to huge plastic waste. Throw in the host of related party transactions and poor working conditions and the company managed to fail at all three ESG hurdles.

These issues, along with dubious free cash flow figures and inconsistencies in the profit-and-loss statement were pointed out by activist short seller Shadowfall in a research note published in May. The company’s credibility and share price took a further hit in July when the factories owned by third-party suppliers in Leicester were accused of slave-like working conditions. Fund managers who had slapped ESG stickers on their portfolios were quick to dump their Boohoo shares. Questions have been asked about why they were included in ethical portfolios in the first place.

In part, such scandals might be expected, given the ESG industry’s relative infancy. “There is absolutely a danger stalking the sector right now in that, like any fashions in finance and any birth of innovative new activity on the back of a zeitgeist shift, you’re moving from what was basically a cottage industry into a massive enterprise almost overnight,” argues Gillian Tett, Financial Times US editor-at-large and founder of the ESG-themed newsletter Moral Money (see page 51). “There’s going to be challenges around whether you can get the infrastructure sufficiently mature sufficiently fast enough to avoid accidents.”

More red flags

Boohoo is not the only ‘green pioneer’ to face the wrath of the short sellers in 2020. In September, electric truck manufacturer Nikola (US:NKLA) – widely touted as a contemporary of electric vehicle giant Tesla (US:TSLA) – was forced to admit that the hydrogen-fuelled lorry in its promotional video was not moving under its own steam, but had been rolled down a hill. The revelation, exposed in a report by short-activist Hindenburg Research, prompted the resignation of the founder and chief executive, an SEC investigation and a collapse in the share price.

Hindenberg has also recently gone after Loop Industries (US:LOOP), the self-proclaimed pioneer of the sustainable plastic revolution, which the short seller claims has “no viable technology”. GrowGeneration (US:GRWG), an online retailer of cannabis growing equipment and organic garden supplier, was described by the activist as having “the brightest management red flags we’ve ever seen”. Like Nikola, the share prices of these apparently ethical companies collapsed in the wake of Hindenberg’s revelations, and Loop faces legal inquiries regarding the legitimacy of its plastics claims.

Exposing unethical companies claiming ESG-credentials perhaps goes beyond the traditional role of the short activists. “There probably aren’t that many companies in the ESG universe that actually make a positive contribution to society,” says Carson Block, founder of short activist Muddy Waters, “I suspect the vast majority of the money [being invested in ESG] is going to be misallocated.”

Revealing fraudulent ESG companies could eventually lead to a better allocation of capital in responsible ventures and prevent continued investment in areas that make negative contributions to the environment or society. For Mr Block, the role of the short sellers here is clear: “We want to pull their pants down in public and say ‘nothing green here’”.