- US is flirting with a slide into recession

- European markets are subdued

- Could bear market rally be turning into something more solid?

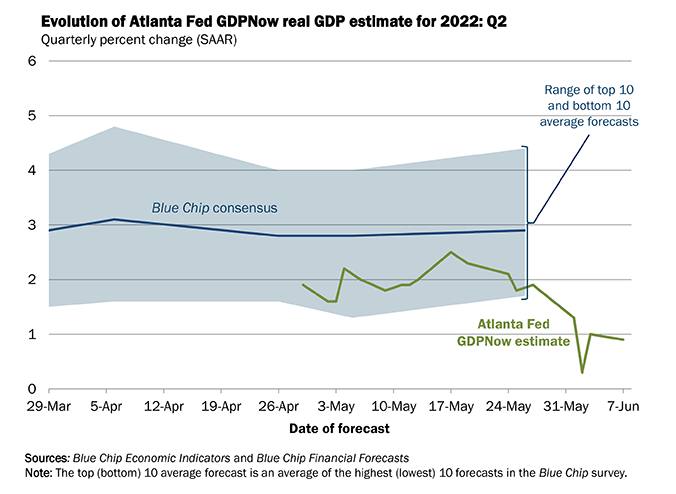

Close to recession: The Atlanta Fed GDPNow model suggests real GDP growth of +0.9 per cent in Q2, down from +1.3 per cent a week ago. Only on 27 May it was at +1.9 per cent, which as I noted last month was low enough to suggest a recession is on the cards since the GDPNow data is always some way out. Four weeks ago it was 2.5 per cent. The initial estimate of first-quarter real GDP growth released by the US Bureau of Economic Analysis on 28 April was -1.4 per cent, a full 1.8 percentage points below the final GDPNow model nowcast released on 27 April. I think the US is close to recession, defined as two consecutive quarters of negative GDP. PMIs have been declining, auto and retail sales have been weak; forecasts remain too high. Does this matter to the market? Well not a lot – we’re well used to the concept of Wall Street not reflecting Main Street. And I don’t think the Fed is going to cool off on rate hikes before it’s more confident inflation is coming down. What we would look at is the labour market - it will take some really bad payrolls prints to force the Fed to ease off but, for now it seem, even in a recession the labour market should stay tight.

European stock markets treaded lightly in positive territory on Wednesday morning with the FTSE 100 hovering around 7,600. Basic resources and banks were among the worst performers, whilst retail, tech and travel & leisure were the top sectors on the Stoxx 600. Notably strong performance from retail after Inditex posted an 80 per cent jump in profits with decade-high margins of 60 per cent. This came in the wake of Target’s warning it would need to work down excess inventory (deflationary?). Banks were dragged down by a third profit warning this year from Credit Suisse. Wizz Air (WIZZ) fell 2 per cent as the company warned of further losses on ongoing travel disruptions in the airline sector despite excellent demand over the summer.

The S&P 500 rallied almost one percent, as did the Nasdaq, as stocks on Wall Street rose for a second straight session. Exxon Mobil (US: XOM) nears record high of $104.76 set in July 2014 (albeit market cap still way smaller than then due to buybacks). Overnight, Asian markets were firmer with a 10 per cent pop for Alibaba (HK: BABA) shares in Hong Kong. US 10yr Treasury yields hold just above 3 per cent, with WTI up about 1 per cent at $120 this morning and gold hanging around $1,850.

JPM: "Many describe the recent market bounce as a “bear market rally”, but the chances are the stabilization becomes more durable. This is especially given the reduced positioning and cautious consensus outlook, and we note market internals over the past month are pro-risk."

Also JPM: “We look for markets to recover YTD losses in H2; however, we don’t advocate indiscriminate buying of broad equity markets. We see strong opportunities in segments with near record low relative valuations (e.g. innovation, China ADRs, small caps, energy, biotech, etc.)”.

RBC: "We are trimming our S&P 500 year-end 2022 price target to 4700 from 4860. We are continuing to bake in a slower economic growth backdrop in 2022-2023 but not a recession.”

And finally, BofA's Michael Hartnett: "summer of Volcker… Fed begins QT, summer of 50bps hikes, central banks just getting started, terminal rates trending higher across G7; 1974, 1981, 1994, 2009, 2018… no fun 'til Fed done... and in 2022 that requires negative payroll print."

ECB day tomorrow… expect a two-pronged attack on inflation and fragmentation; ending net asset purchases, signal hikes coming in July and be ready to adopt new tools to avoid bond spreads widening by supporting bond markets in weaker countries (ve are here to close ze spreads!).

FX markets not doing a lot this morning with EURUSD just under 1.07 and GBPUSD tracking the channel around 1.2550, but USDJPY is back above 133 at a fresh 20-year high, just as Bank of Japan boss Kuroda is out on the wires saying inflation will be transitory…

Neil Wilson was the Chief Market Analyst at markets.com