In a mixed reporting season for the supermajors, first-quarter numbers for oil and gas behemoths BP (BP.) and Royal Dutch Shell (RDSB) were fairly well received by investors. Predictably, earnings were well up on the same period in 2017, when Brent was selling for less than $50 (£36.6), although cash generation at both London-listed stocks fell short of analyst expectations. That hasn’t stopped the prevailing narrative – a tightening and nervy market for crude – from pushing both shares to multi-year highs.

Indeed, at $75 a barrel, crude now hovers more than a fifth above the average sales prices booked by both BP and Shell in the first three months of 2018. The expectation among investors will be that second-quarter cash flows improve alongside this rise.

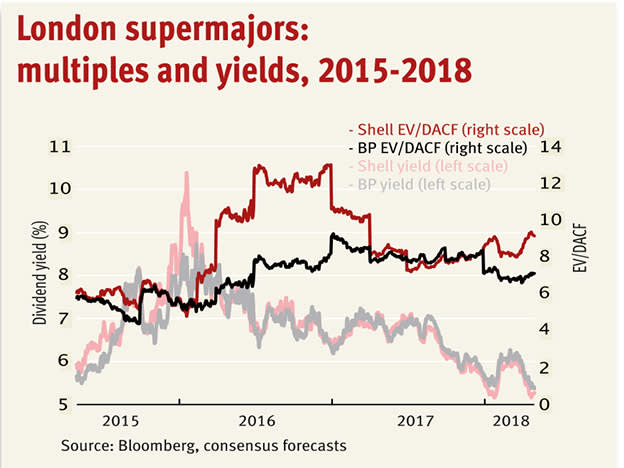

For Shell, a strong contribution from the integrated gas division meant first-quarter free cash flow of $5.2bn was enough to cover the dividend. But operating cash flow of $9.4bn was down year on year and on the last three months of 2017, owing to a higher tax bill and increased cash margining on derivative contracts. Nonetheless, the balance sheet shows further signs of repair; despite a slight climb in net debt, gearing narrowed and the group reiterated its intention to retire $25bn of shares between now and 2020.

For BP, earnings (defined as replacement cost net income) came in well ahead of consensus expectations at 13¢ a share, although net cash flow of $3.6bn was down 38 per cent on 2017’s fourth quarter. Limited divestments, an expected build in working capital and a final Deepwater Horizon-linked $1.2bn payment to the Department of Justice conspired to push net debt to $40bn. Gearing therefore climbed from 27.4 per cent at the end of 2017 to 28 per cent, although chief financial officer Brian Gilvary said this was in line with plans, and that net debt would roll off throughout 2018.

In an interview with Bloomberg, Mr Gilvary added that build in working capital was typical for the first quarter, and given the upward movement in prices. However, Panmure Gordon analyst Colin Smith pointed out that BP’s negative working capital impact was “twice that experienced by Shell, which has a much larger downstream business than BP”.

Still, at 545p, BP’s shares are trading at their highest level since the Macondo disaster. That provides a nice coda for chairman Carl-Henric Svanberg, who joined just months before an uncontrollable blowout at the Deepwater Horizon rig caused the largest oil spill in US waters. He departs at the end of 2018, and will be succeeded by former BG Group and Statoil chief executive Helge Lund.