It was a symbolic step. Last month, Norway’s sovereign wealth fund, built up over decades from the country’s own energy resources, proposed dropping its investments in oil and gas stocks. The trillion-dollar fund is far from the first to begin shying away from oil and gas investments in its attempt to protect the nation’s wealth from a permanent drop in the oil price. But the move demonstrates how mainstream it has become to think of environmental risk when considering investment opportunities.

A recent survey of European institutional investors by consultancy Create-Research indicated six out of 10 planned to increase their allocations to “responsible investments” – those screened for environmental, social and governance risk – over the next three years. None of the respondents planned to decrease their allocations.

The global political consensus now seems to be that climate change poses a profound challenge that must be dealt with. Carbon emissions from fossil fuels and other sources are, many believe, leading to weather events of increasing power and frequency. As population growth accelerates, our resources look set to become ever more constrained, increasing the risk of geopolitical turmoil as more people compete over dwindling resources in harsher environments.

The solution favoured by the world’s governments was the Paris Agreement, also known as COP21. World leaders committed to begin reducing the emission levels of greenhouse gases as soon as possible and provide $100bn (£756.5bn) annually to developing countries to aid their efforts, with a view to keeping the global temperature increase “well below” 2°C above pre-industrial levels. It included pledges to report on progress every five years while pursuing efforts to limit temperature increase further to 1.5°C. When the agreement was signed in December 2015, some critics attacked it as insufficient. Then, earlier this year, President Donald Trump announced the US would be pulling out and it looked all but dead on arrival.

Whether or not the US will actually refuse to honour the agreement is not yet clear. Many states and US-based companies have continued their efforts to reduce emissions since the announcement, but increasingly it looks as though a combination of technological advancement and economic opportunity will render the opinions of President Trump – and indeed all world leaders – moot. But for a shift towards a renewables-based energy system to happen, profound changes to the way energy is generated, moved, stored and consumed are needed.

Energy systems the world over are governed by three competing priorities, sometimes referred to as the “trilemma”: they need to be cheap, reliable and sustainable. Given the reliance on coal and other fossil fuels in the majority of the world, the first two demands have for a long time beaten the third, but coal is losing ground as a core part of the power generation mix.

Some believe the solution to all three planks of the trilemma is nuclear power, but the disasters in Fukushima and elsewhere make many cautious. What’s more, with UK wind projects recently winning government contracts with a guaranteed energy price of £57.50 per megawatt hour, the inflation-linked price of £92.50 over 35 years the government is paying for the Hinkley Point nuclear reactor destroys its cost appeal. Dr Charles Donovan, director of the Centre for Climate Finance and Investment at Imperial College London, says “you would be hard pressed to find a nuclear project that was built on time and on budget… Investors like building big things [but] the problem with nuclear is there are risks only governments really underwrite.”

Different renewable technologies face their own technical challenges, while a report from analysts at Cantor Fitzgerald, Unintended Consequences: The New World of New Energy, indicated that of 85 new listed energy and clean technology companies from January 2010 to September 2016, only 13 had a positive return and of those only six had not delisted. The report notes companies’ own renewable credentials can become a challenge, as frequently management’s message to investors was “more about saving the planet rather than delivering returns to investors”. While the report’s authors said this was “laudable”, they added it “often led to unsustainable businesses that met neither goal”.

As was seen with COP21, the policy landscape is constantly changing. In September, non-US makers of photovoltaic solar panels were hit with the prospect of tariffs and price controls after the country’s International Trade Commission ruled domestic manufacturers had been damaged by imported panels. But the body later issued recommendations for lower tariffs than hoped for by US manufacturers: the final word rests with President Trump.

In recent months, both the US and Australian governments have made energy policy proposals that are widely predicted to encourage energy suppliers to buy from coal-fired power stations. Concerns were also raised about the UK’s commitment to climate change action in the wake of the EU referendum, as it may no longer be bound by the political union’s climate change and renewable energy targets. However, the UK’s performance in this regard has been well ahead of the EU as a whole and as Energy UK, a trade association for energy companies, points out: “The UK’s above average performance masks the lack of action on climate change from some other member states... [Brexit] could potentially have a more significant impact for the EU in its delivery of its commitments under the Paris Agreement”.

Despite all this, the march of renewable energy looks almost unstoppable. In April this year, the UK had its first full day without turning on one of its coal-powered generators since the industrial revolution. Once dominant, the reliance on coal for power has fallen sharply. It accounted for 9 per cent of generation in 2016, from 23 per cent in 2015. The UK government is now considering dropping unabated coal generation entirely by 2025.

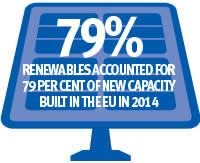

Looking at the data, it becomes abundantly clear which way the wind is blowing. According to research from Impax Asset Management (IPX), an asset management company that specialises in sustainability, renewables accounted for 72 per cent and 79 per cent of new capacity built in the EU in 2013 and 2014, respectively. This is largely focused around solar and wind power, which are generally accepted as the most developed technologies. Both have come down in price sharply in recent years, reducing their reliance on government subsidies and by extension their policy risk. Bloomberg New Energy Finance expects $10.2 trillion to be invested in new power generation capacity globally by 2040. Of this, almost three-quarters (72 per cent) is expected to go to renewables, with $2.8 trillion and $3.3 trillion for solar and wind, respectively.

Jon Forster, senior portfolio manager at Impax, stresses the importance of “the technologies, the value chain and the regulatory environment” when looking to invest in renewables. The sector is not immune from bubbles, he says, as was seen in solar energy in 2007, following oversupply from Chinese manufacturers, among other factors. Mr Forster adds: “We believe that allocation to renewables should make up a part of a much broader alternative energy portfolio.”

The prevailing strategies for bringing about a renewable energy system cluster around three priorities:

- Making generation more flexible and robust

- Improving the capacity for independent supply

- Improving all-around efficiency.

Combined with the spread of technology and generation capacity, experts hope these strategies will bring about a sustainable energy system.

Building efficiency

Efficiency efforts are the thin end of the wedge when it comes to the changing energy system, and can seem reassuringly similar to the way things are already done. Meters become smart meters, grids become smart grids, and improvements in efficiency lead to incremental improvements in service, price and processes. Perhaps for this reason, government policy tends to be more reliably supportive than elsewhere.

Efforts to improve efficiency are not strictly renewable, as the intention is to make every unit of energy go further by improving how the system balances supply and demand. Smart meters, for example, help consumers to use less energy, but are agnostic as to how the energy was generated. Nevertheless, as demand skyrockets with the proliferation of data centres and electric vehicles, action to improve efficiency will be a key part of the strategy to adapt.

Smart meters track energy usage in a more granular way than traditional meters, allowing real-time feedback to customers on what they are spending on energy and offering the grid data on usage patterns, allowing it to better balance energy supply and demand. The UK government has pledged every home and small business in the country will be offered a smart meter by 2020, providing strong momentum for rollout and leading to a steep improvement in the share price for Smart Metering Systems (SMS), which distributes and maintains domestic meters domestically.

Other countries are investing heavily in the rollout of smart meters, too, with the EU and India pledging to roll out 240m and 130m meters by 2020, respectively, while China aims to deploy 360m by 2030, according to data from the European Commission.

Given the regulated nature of the bigger players, improving efficiency offers improved returns for them too. National Grid (NG.) is exploring the potential for a smart grid on a national scale. The group is in talks with US tech giant Alphabet’s (US:GOOGL) artificial intelligence division DeepMind to explore using its AI technology to help it balance supply and demand across the network.

Building flexibilty

Different forms of renewable energy work better in different places, leading to wide discrepancies in the viability of different technologies in different areas. For example, the output of a wind turbine is related to wind speed, cubed. As Adam Forsyth, analyst at Cantor Fitzgerald, puts it: “If you have a site twice as windy as another, it’ll give you eight times more output.”

In a UK context it is easy to see why it creates a challenge, as the most promising sites for onshore wind generation are in Wales and the Scottish Highlands, while most of the demand for electricity is concentrated around south-east England.

Technologies such as wind and solar can also be highly intermittent, relying on the wind to be blowing or sun to be shining to produce electricity. Analysis by the UK Energy Research Centre found penetration of 20 per cent or more of intermittent renewables into the British electricity system could mean overall costs vary dramatically, although it adds this is because the costs are “normally the result of inflexible or sub- optimal systems”, noting energy systems “must adapt and be re-optimised to incorporate large proportions of variable renewable generation”.

Dr Donovan says: “The difficult thing about electric power is it’s not a global market, it’s inherently a very local market. You don’t implement a single fix.” Just as markets adapted to accommodate fossil fuels, he says, “we need to design markets that are responsive to the inherent properties of these technologies”.

One way to solve the problem is through energy storage, to eliminate the time factor from the generation and use of electricity. Battery technology made headlines earlier this year when Tesla and SpaceX founder Elon Musk made a public bet in March on social media website Twitter that his company could install a 100MW lithium ion battery – the largest such battery ever – within 100 days or else would do it for free. By November, construction on such a site was completed, a battery linked to a wind farm in South Australia, within 100 days of the grid connection agreement.

Lithium ion batteries are the technology many are expecting to solve the storage issue, with Bloomberg New Energy Finance estimating it would be a $20bn a year market by 2040. However, costs for the batteries still need to come down significantly. Mr Forsyth observes that lithium ion often becomes more expensive the more energy you need to store, so it can be difficult to access economies of scale.

Some instead believe that future lies in flow batteries – a rechargable battery technology where the energy is stored in an electrolyte fluid as opposed to the electrode material found in traditional batteries. The advantage of flow batteries against lithium ion is that they can be recharged incredibly quickly by simply removing the spent fluid and replacing it. UK-listed redT energy (RED) manufactures flow batteries, with chief executive Scott McGregor recently declaring the UK a “strong economic market” for the technology, having previously been vocal about the challenges.

Distributed supply networks

As with the introduction of any new technology, renewable energy holds a threat to the incumbents in the markets in which it operates. Many of the FTSE 100 have been working to adapt to the changes, with BP (BP.) investing heavily in renewables and SSE (SSE) developing wind farms. Inevitably, though, the shift away from centralised forms of power generation such as coal-fired power plants opens up opportunities for challengers to enter the market. Many experts believe there will be an increasing trend for off-grid power generation in coming years.

In the energy system as it exists currently, electricity is generated at a power station – generally through the consumption of a fuel such as coal or gas. It then goes through long-distance transmission lines to substations and is moved into subtransmission lines, also known as the distribution network. From there it is supplied to customers. This system is largely based on the assumption of power being generated from a few large sources then transmitted across a large network. Current trends indicate in future energy will be generated from many small sources and stored. Recent analysis from Moody’s Investor Service warned electricity flows are becoming “increasingly unpredictable”, with moves away from gas for cooking and heating combined with adoption for electric vehicles significantly altering the demands placed on networks. This is significant, the authors note, because “as renewable technologies evolve and become more affordable, an increasing number of residential customers may see an opportunity to save on energy costs by coming off grid”.

A key milestone for any new form of energy generation is reaching “grid parity” – also sometimes known as “socket parity” – meaning its cost of electricity is equal to or less than the cost of buying the same amount of electricity from the grid. The challenge the incumbent energy providers face comes from more distributed sources of energy that do not have the same need for power stations, transmission lines or distribution systems as the current system, meaning they can bypass large parts of the existing system and thus skip the attendant cost.

On this front, developing countries are poised to benefit as they can implement newer-style systems to begin with instead of updating large amounts of legacy infrastructure. Companies such as OPG Power Ventures (OPG) and Mytrah Energy (MYT) could stand to benefit, as both are India-focused energy companies. Mytrah is focused on renewable generation, while OPG has a combination of coal-powered and solar capacity. Both are also likely to benefit from the growing demand for energy in India as the middle class balloons.

Straddling the divide between developed renewables such as solar and wind, and newer technologies such as fuel cells, we have hydro power. Hydro uses the movement of water to power turbines to generate electricity, often in the form of dams or using tidal movements. Impax anticipates hydropower output more than doubling over the next decade. Pumped storage – which releases water from a high-elevation reservoir through turbines to a lower elevation in order to capture energy – is also expected to increase, with €26bn (£23.2bn) being invested in 60 new plants with 27GW capacity by 2020.

The development of hydropower, and concurrent improvements in its investment appeal, seem almost inevitable. “Had we put the focus into tidal that we put into wind 20 years ago, it’s possible tidal would be in the same position,” says Dr Donovan. The costs associated with building dams and other hydropower plants tend to be very large, with research from Impax noting “large capex, long permitting and development times are the rule for most new-build dams”. However, Dr Donovan says: “If there’s one this we learned from solar, it’s that once you get going, economies of scale start to take over.”

Where to next?

Transitioning to a renewable energy system will not be easy. The EU estimates €380bn (£340bn) will be needed annually between now and 2030 to hit renewables targets. Such an investment will inevitably lead to increased innovation and development of technologies, although Mr Forster says investment in upgrading the transmission infrastructure is also needed.

“Additional cross-border electric capacity throughout Europe is required to direct surplus power across different regions,” he says. “The turbines and solar panels you see are only a small part of the story.”

By continually developing efficiency, flexibility and distribution of supply, renewable energy can enter a virtuous cycle with each progressive improvement making it more appealing to investors and consumers, driving yet more improvements. While parts of the sector face different individual challenges, the fundamental drivers – namely the global drive to tackle climate change, the increasing demand for electricity and the falling cost of technology – remain sound.