There’s always room for another article on emerging market (EM) investments – primarily because of the potential long-term growth rates on offer – but also simply because there are now so many ways to gain exposure. Whatever your views on the rise of EM economies since the early 1990s, particularly in terms of trade flows and their effect on the industrial base of western economies, it’s certainly much easier to ‘buy in’ than it was 20 years ago – it’s probably little solace for blue collar workers, but investors are now spoilt for choice in this area.

Doubtless, many of our readers have already opted for holdings in closed-ended options such as Templeton Emerging Markets (TEM), but there’s dedicated investment managers like Ashmore (ASHM), regionally focussed financial institutions like Standard Chartered (STAN), or the many mandated funds in this area.

There is even a widely accessed retail market in EM exchange traded funds (ETFs), although these derivatives have been blamed for anomalous pricing as they are traded in much greater volumes than their more illiquid underlying instruments (a similar criticism surrounds the trade in physically-backed gold ETFs, but that’s another story).

It’s worth noting that 234 Chinese home-grown stocks, dubbed 'A shares', are being added to the MSCI's Emerging Market index between June and September this year. This means trackers and ETFs that benchmark themselves against the index will start to hold Chinese stock market blue-chips, in addition to their exposure to Hong Kong-listed Chinese companies.

Helping China clean up its act

But away from managed money and derivatives, we think there’s another avenue worth exploring. As western nations found to their cost during the latter decades of the 19th century, industrialisation comes at a price. As EM economies evolve, we’re seeing more opportunities for home-grown companies that offer high-tech equipment and services designed to lessen the environmental impact of progress, through the modernisation and refinement of inefficient production processes.

The breakneck speed towards industrialisation has given way to negative consequences for the physical environment and even raised the spectre of civil unrest. The dash for economic growth is increasingly accompanied by a more considered take on its wider stakeholder implications. You get some idea of the re-prioritised outlook in China’s 13th Five-Year Plan for Economic and Social Development (through to 2020), which, among a series of policies related to environmental protection, includes a goal of improving the number of annual days with clean air to 80 per cent – hardly an unrealistic expectation, one would think. Because the nation still possesses the rudiments of a planned economy, it has been able to initiate outright bans on polluting activities, rather than fiscal incentives to reduce them – as is so often the case in the west.

Bans on new coal-burning capacity were introduced, along with controls on steel and aluminium smelters. Large numbers of urban domestic dwellings, currently dependent on the burning of coal, are being converted to electricity or gas (around half of China’s pollution is traceable to coal-fired power stations}. However, although these measures have dramatically reduced pollution levels in the large northern cities, the nationwide incidence of fine particulate matter fell by a relatively modest rate through 2017, suggesting that the draconian measures may have inadvertently shifted some polluting activities to other parts of the country.

An unlikely commodities angle – high-grade benefits

Although it may seem counter-intuitive, China’s determination to implement meaningful environmental controls could have positive implications for investors who approach EM investments from the commodities angle by gaining exposure to producers of key industrial inputs – a familiar theme. China may be reducing excess capacity in its steel mills, but a government crackdown on inefficient illegal furnaces that use scrap for production has spurred demand for seaborne iron ore, as higher-grade ore limits emissions and boosts productivity. This has provided an unexpected fillip for high-grade iron ore miners such as Rio Tinto (RIO). In addition, the FTSE 100 mining group, along with ‘lower impact’ producers such as Norsk Hydro ASA (SWX: NHY), are also benefiting from the country’s clampdown on aluminium facilities (China remains the world's largest producer of the metal), or at least those that fail to meet the beefed-up environmental regulations introduced in 2015. This should also help to alleviate persistent overcapacity in global markets.

Clean industry fuelling economic growth – a difficult balancing act

Although developing economies are increasingly seeking less polluting processes, they still need to fuel economic growth – a difficult balancing act. China’s war on pollution has put a brake on the economy, at least to an extent, which helps explain why it is just as keen to revolutionise heavy industry – cleaner power plants, more efficient smelters etc. So, while western industrial companies have found the going tough when they’ve tried to compete with EM rivals in terms of volume production, they’re certainly competitive further up the value chain. A handful of UK industrials have already positioned themselves to profit from this dynamic, but we think it will provide increased opportunities for investors over the long haul.

Before we examine some of the companies that are exploiting increased demand for advanced industrial inputs and processes, it’s worth exploring the parallel changes that are shaping EM economies, because they’re not quite the same beasts they were 20 years ago.

The EM growth narrative remains intact – at least over the long haul

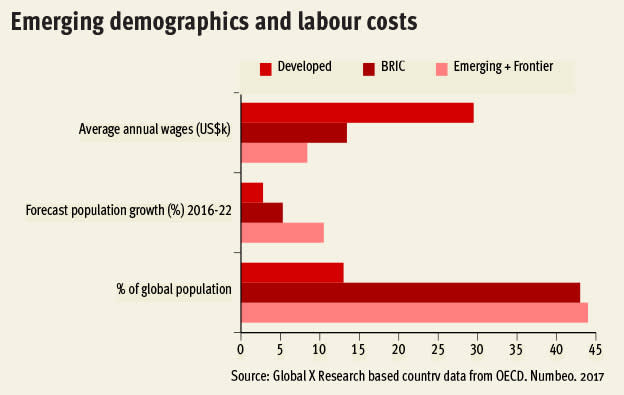

The pace of economic development is made plain from an historic perspective. Figures published by the World Bank show that the contribution of the seven largest EM market economies (as a proportion of global output) has climbed markedly, with the EM7 – Brazil, China, India, Indonesia, Mexico, Russia and Turkey – accounting for 24 per cent of global economic output through 2010-2016, up from an average of 14 per cent in the 1990s. Over the same timeframe, the relative contribution of the G7 industrialised economies shrank to 48 per cent from 60 per cent.

As they grow, so the EM economies evolve, becoming ever more resilient to shocks such as the 1997 Asian financial crisis. Improving regional capital markets and treasury management have given emerging nations a larger set of policy levers to conduct expansionary fiscal and monetary policies – this was apparent in the aftermath of the global financial crisis.

Unlike earlier crises, where EM economies often fared much worse than developed nations, this time the shock had broadly similar effects. Indeed, most EM economies don’t have the same burden of highly indebted consumers, so they weren’t forced to endure the subsequent debt retrenchment that dragged on western economies.

Municipal/state/corporate debt issues

However, the municipal, state and corporate debt profiles of some EM economies, most notably China, give more cause for concern. As if to bear this out, Beijing has tightened controls on new local government debt to reduce risks following a surge in borrowing since the global financial crisis.

Nonetheless, analysis from PwC states that the E7 could grow around twice as fast as the advanced G7 economies through to 2050, by which time six out of the seven largest economies in the world are projected to be emerging economies led by China (1st), India (2nd) and Indonesia (4th).

We know that long-range economic forecasts are about as reliable as those for the weather; indeed, it’s been said that an unsophisticated forecaster uses statistics as a drunken man uses lamp-posts – for support rather than illumination. But the projections from the accountancy giant do fall into line with the wider narrative – expectations for these economies remain positive over the long haul, although there are some immediate challenges.

Tightening US monetary policy puts on the squeeze

At the start of this year, Carlos Hardenberg, manager of the Templeton Emerging Markets Investment Trust, pointed out that global investors were essentially underweight in EM stocks, or at least below the level that he would have expected given the proportion of global GDP and market capitalisation they represent. The main threat to valuations stems from the likelihood of further tightening of monetary policy in the US. The Federal Reserve recently hiked rates for the second time since the final quarter of 2017. The median forecast for interest rates at the end of this year was left unchanged, but projections point to an extra increase in 2019, with more tightening to come in 2020.

As rates have risen, they’ve lifted the US dollar against all but three of the biggest EM currencies this year; a potential problem given the inverse correlation between the dollar and many commodities (by extension, EM growth rates). The Trump administration’s tariff initiatives and murmurings of a trade war have resulted in a slide in the yuan exchange rate, although this issue has obviously yet to play out. A rising dollar also alters the debt profiles of developing economies, as their external liabilities tend to go up in line with dollar appreciation.

With GDP growth across the Atlantic edging up towards 4 per cent under the Trump administration, and given its likely impact on interest rates, we’re unlikely to witness a repeat of last year’s 34 per cent return in the MSCI Emerging Markets Index. US dollar effects can combine to reduce aggregate demand in EM economies, but you could argue that this doesn't undermine the long-term investment case for western companies, which are effectively piggy-backing on the changing face of industrialisation in these markets.

Three established thematic plays: Johnson Matthey, Porvair and Vesuvius

You would imagine that a company founded in London two centuries ago as a gold assayer, would be an unlikely candidate to tap into this growth, but Johnson Matthey (JMAT) has survived this long precisely because of its ability to adapt to industrial change. Today it is probably best known for producing catalysts that remove polluting substances from vehicle exhausts – a potential problem as the global switch to electric motoring (EV) gathers momentum.

But the group identified the opportunity in Asia’s EMs early in the millennium, opening its first auto catalyst facilities in Shanghai in 2001, and its regional growth rates are now benefiting from increasingly stringent regulatory measures on air quality in auto growth markets, most notably China. Johnson Matthey now operates across seven locations in China and is a major manufacturer of emission control catalysts and automotive battery materials in the country. Production of light duty vehicle (LDV) catalysts are growing ahead of global vehicle production, while the transition towards low or zero emission motoring is likely to be driven by hybrid vehicles (which still require clear air technologies), as opposed to pure EV.

Beijing’s determination to reduce the environmental impact of industrialisation and improve resource efficiency also paved the way for the opening of a platinum group metal refinery in the eastern-central coastal province of Jiangsu. The refinery provides advanced analytical methods and modern refining technologies – a classic example of how UK companies can compete globally by offering products and services further up the value chain. More than 90 per cent of Johnson Matthey's sales are linked to high-margin technologies designed to increase resource efficiency, or to lessen the impact of industrial processes on the environment – with much of the demand regulatory-driven.

Another UK industrial, Porvair (PRV) is engaged in advanced technologies linked to metals filtration and microfiltration. It operates across three divisions: Aerospace & Industrial (approximately 40 per cent of group revenue); Laboratory (30 per cent); and Metal Melt Quality (30 per cent).

The geographic spread shows the group expanding across the EM space, in addition to its traditional locales: 54 per cent of revenue is in the Americas; 19 per cent in Asia; 13 per cent in the EU; 13 per cent in the UK; and 1 per cent in Africa. The group continues to build its presence in Asia, with further investments made to expand its Metal Melt Quality capabilities in China during 2017. As the Chinese aluminium market matures, the group expects demand for its proprietary filters to grow on the back of proven quality and environmental performance. Higher grades of metal require better filtration and Chinese producers are moving to higher-grade alloys.

Vesuvius (VSVS) is also growing on the back of tightening regulatory strictures and the push for more efficient production processes. The FTSE 250 constituent provides high-specification ceramics and molten metal flow engineering technology for the steelmaking and foundry industries.

At its latest full-year figures, management pointed to accelerating momentum in China, with 9.2 per cent underlying sales growth, driven by the trend towards “higher quality steel requiring higher quality products and value creating solutions”, although the group grew sales in excess of underlying market growth in India, South America, Mexico and EEMEA (Eastern Europe, the Middle East and Africa). Again, the group’s business model is underpinned by proprietary technologies and premium pricing. This combination and an effective focus on ‘value add’ has enabled it to outperform its underlying markets – last year, the steel flow controls segment grew by 11.8 per cent, double the rate of the wider market, driven by China, India and other EM foundries.