My Best of British screen tries to identify winning shares from domestically-focused large-caps. This has been tough work in recent years given the seemingly interminable whir of Brexit angst. But following three years of torrid performance, in the past 12 months the screen has had an excellent run. Could this be the market heralding the emergence of political harmony and sunny economic uplands? Possibly not, but that doesn’t mean the good times for the screen need to be fleeting.

The past few years were never going to be easy for a screen aiming to beat the wider market by focusing on domestic plays. The challenge was set by the nation’s emergence from the Brexit referendum almost split down the middle for leave (52 per cent) and remain (48 per cent). Since then, among political movers and shakers, the narrow winners of the referendum have often seemed intractably divided over what a desirable Brexit would involve. Meanwhile, many of the losers still appear to believe they can snatch victory from the jaws of defeat.

And now the nation has a Brexit deadline at the end of the month, with a government with no parliamentary majority that is chiefly made up of adversaries to a previous Brexit deal, but that profess to want a new deal, while also advocating a possible no-deal, despite a law aimed at ruling out a no-deal on 31 October. Could things be messier or more confusing for investors?

Yet there are also grounds to think we may finally be entering some kind of Brexit end game (at least, for the initial stage of the Brexit process that the country has spent the past three years grappling with). Importantly, a resolution of some sort and the clarity that could bring may be enough to put the wind in the sails of the Best of British stock screen, especially considering the heavily negative investor sentiment towards the UK market.

What’s more, this screen was devised to profit from a time when it was politically expedient to talk down the UK’s prospects. It was put together in reaction to economic fear-mongering to lay the case for austerity economics. Politicians were going so far as to suggest credible parallels existed between the UK and the enfeebled Greek economy.

Once again there is a political gain to be had from talking down the nation’s economic prospects. In this case, the debating position is to predict dire consequences from whatever form of Brexit a politician is opposed to.

While I’m definitely not smart enough to know what the economic implications are of any of the plethora of possible outcomes, the polarised nature of the debate means it’s odds-on that many economic arguments are being richly over-egged on every side of the Brexit ding-dong.

This is a long-winded way of saying there is a credible contrarian case to hope the Best of Britain screen could benefit if the country can move things forward, especially if it is in a spirit of intelligent compromise. The timing of the screen last year was lucky, with performance benefiting from the level of pessimism pervading the market 12 months ago – especially towards housebuilders, which were heavily represented in the screen’s results.

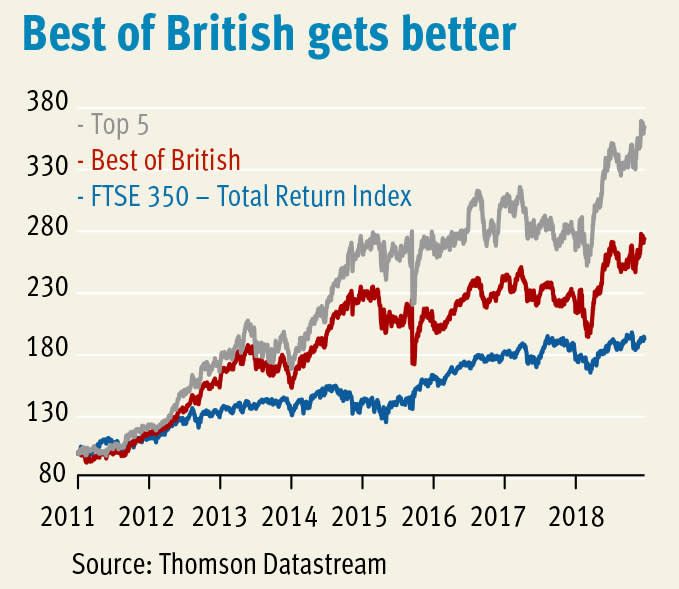

Indeed, the screen is not representative of all UK-focused companies and seems to have managed to do an impressive job with stock selection last year. The top five shares, based on three-month momentum, produced a 34 per cent total return and the whole screen delivered 26 per cent. This compares with 9.3 per cent from the FTSE 350.

2018 performance

| Name | TIDM | Total return (15 Oct 2018 - 2 Oct 2019) |

| Redrow | RDW | 20% |

| Marshalls | MSLH | 66% |

| Barratt Developments | BDEV | 30% |

| Bellway | BWY | 25% |

| Primary Health Props. | PHP | 29% |

| B&M European Val.Ret. | BME | -1.4% |

| Taylor Wimpey | TW. | 11% |

| FTSE 350 | - | 9.3% |

| Best of British | - | 26% |

| Top 5 | - | 34% |

Source: Thomson Datastream

The recent strong showing takes the cumulative total return from the screen since I started to run it in 2011 to 174 per cent, or 264 per cent for the top five based on three-month momentum. This compares with 93 per cent from the FTSE 350 over the same period. While the screens monitored by this column are considered to offer ideas for further research rather than off-the-shelf portfolios, if I add in an annual charge of 1.5 per cent to reflect real-world dealing costs the cumulative Best of British total return drops to 143 per cent, or 223 per cent for the top five.

At its heart, the Best of British screen is a momentum screen with a few quality checks and an insistence that over three-quarters of a company’s sales come from the UK. The screening criteria are:

■ At least three-quarters of revenue from the UK.

■ Three-month share price momentum better than the FTSE 350.

■ Return on equity of more than 10 per cent.

■ One-year beta of less than one.

■ Forecast EPS growth in this and the next financial year.

■ Better than average five-year compound annual growth rate (shorter periods used when a full five-year record is unavailable).

■ Net debt of less than 2.5 times cash profit.

This year only four shares passed all the tests. I’ve taken a closer look at them below. The table above also provides details of shares passing all but one test unless the test failed was either the test for UK revenues or the momentum test.

Best of British 2019

| Name | TIDM | Market cap | Price (p) | Fwd NTM PE | DY | PEG | P/BV | Fwd EPS grth FY+1 | Fwd EPS grth FY+2 | 3M Fwd EPS change | 12M Fwd EPS change | 3-mth momentum | Net cash/debt(-) | UK rev | Test failed |

| Howden Joinery Group Plc | LSE:HWDN | £3.4bn | 572p | 17 | 2.1% | 2.6 | 6.2 | 6.3% | 7.3% | 0.8% | -2.8% | 10.0% | £217m | 98% | na |

| GCP Student Living plc | LSE:DIGS | £710m | 172p | 28 | 3.6% | 0.4 | 1.0 | 19% | 14% | -0.8% | -3.1% | 5.4% | -£234m | 100% | na |

| Rightmove plc | LSE:RMV | £4.9bn | 559p | 27 | 1.2% | 3.5 | 105 | 8.7% | 8.6% | - | - | -0.2% | £42m | 100% | na |

| Marshalls plc | LSE:MSLH | £1.3bn | 672p | 24 | 1.9% | 3.2 | 4.8 | 9.4% | 6.4% | 0.4% | 7.9% | -0.5% | -£98m | 95% | na |

| Cranswick plc | LSE:CWK | £1.6bn | 3,004p | 22 | 1.9% | 3.6 | 2.9 | -4.3% | 17% | 2.7% | -14% | 14.3% | £6m | 97% | Fwd EPS grth |

| Countryside Properties PLC | LSE:CSP | £1.5bn | 335p | 8 | 3.8% | 0.9 | 1.8 | 12% | 9.8% | 0.1% | -7.4% | 10.2% | -£40m | 100% | Beta |

| Barratt Developments PLC | LSE:BDEV | £6.5bn | 646p | 9 | 4.5% | 27 | 1.3 | -0.2% | 0.9% | 4.4% | -1.2% | 8.3% | £758m | 100% | Fwd EPS grth |

| The Unite Group plc | LSE:UTG | £3.2bn | 1,088p | 26 | 2.7% | 0.9 | 1.3 | 14% | 11% | - | - | 8.2% | -£592m | 100% | Net Debt |

| The Berkeley Group Holdings plc | LSE:BKG | £5.2bn | 4,166p | 12 | 0.7% | - | 1.8 | -29% | -0.1% | 0.3% | -0.1% | 7.9% | £975m | 100% | Fwd EPS grth |

| Safestore Holdings plc | LSE:SAFE | £1.4bn | 673p | 23 | 2.5% | 1.2 | 1.8 | 6.0% | 7.2% | 0.4% | - | 7.7% | -£426m | 76% | Net Debt |

| SEGRO Plc | LSE:SGRO | £8.8bn | 804p | 31 | 2.4% | 0.8 | 1.2 | 11% | 8.5% | - | - | 6.5% | -£1.9bn | 84% | Net Debt |

| SSE plc | LSE:SSE | £13bn | 1,252p | 14 | 7.8% | 0.5 | 2.2 | 17% | 15% | -4.5% | -20% | 6.2% | -£9.3bn | 88% | Net Debt |

| Bovis Homes Group PLC | LSE:BVS | £1.5bn | 1,108p | 10 | 5.3% | 1.2 | 1.4 | 8.1% | 8.9% | 1.4% | -2.3% | 5.7% | £80m | 100% | Beta |

| Big Yellow Group Plc | LSE:BYG | £1.8bn | 1,057p | 24 | 3.1% | 2.1 | 1.6 | 5.7% | 6.7% | -0.6% | -3.1% | 5.4% | -£337m | 100% | Net Debt |

| Crest Nicholson Holdings plc | LSE:CRST | £976m | 380p | 8 | 8.7% | - | 1.1 | -13% | 1.0% | 0.5% | -31% | 4.8% | -£66m | 100% | Fwd EPS grth |

| Softcat plc | LSE:SCT | £2.0bn | 1,019p | 29 | 1.3% | 3.2 | 25 | 19% | 3.7% | 3.6% | - | 2.6% | £53m | 100% | Beta |

| Greggs plc | LSE:GRG | £1.8bn | 1,828p | 21 | 2.0% | 2.0 | 5.5 | 22% | 4.8% | -0.6% | 27% | -19.1% | -£191m | 100% | Mom |

Source: S&P CapitalIQ

Howdens Joinery

Despite all the Brexit doom and gloom, and dire trading from some high-street DIY retailers, trade-focused kitchens specialist Howdens (HWDN) has continued to deliver. The company boasts the tantalising combination of high returns on capital (return on capital employed was over 40 per cent last year ignoring lease liabilities) and decent growth. The group makes about a third of the items it sells at a large manufacturing facility in Runcorn and distributes through a network of 731 depots. Its depots are mainly located in no-frills industrial estates, which means the group dodges the high overheads associated with running high-street retail premises. The company sees scope to expand its depot network in the UK to 850 and is also adding to its small number of overseas outlets.

Howdens appears to be benefiting from its popularity with tradespeople and the resilience of this part of the construction market. Recent growth has come from existing customers, who are spending more with the company, as opposed to increased customer numbers. The loyalty of the customer base has also been reflected in the success of price rises in January. This contributed to a pick-up in the group’s gross margins following a couple of years of moderate decline as the company focused on volume growth.

The company offers eight-week credit as a draw to builders who are normally not paid until after kitchens are installed. While receivables (money owed on sales) as a proportion of revenue have picked up slightly over recent years, at 13 per cent there appears to be little to worry about. Stock as a proportion of sales has also been rising, although again, at 16 per cent, this is not high and the increase has been put down to Brexit planning and the introduction of new ranges.

While the company put in a creditable performance during the credit crunch, it is cyclical. Management expressed a “cautious” outlook at the time of the half-year results in July and earlier in the year consensus forecasts slipped. The group’s financial year is also heavily weighted towards its second half and October tends to be a particularly busy month. Any reticence about home improvement projects caused by the Brexit deadline could therefore be quite keenly felt.

Still, the fact that estimated full-year capital expenditure has risen from £60m at the time of the 2018 results to £70m-£80m at the half-year stage could be viewed as a sign of confidence. What’s more, Howdens has a reassuring balance sheet and a hard earned reputation as a well-run business. The shares’ valuation has also looked unchallenging since de-rating following the outcome of the Brexit vote.

GCP Student Living

Student accommodation specialist GCP (DIGS) can in some senses be considered to be making money based on one of Britain’s key exports: education. While GCP’s 11 operational student blocks may be located on these shores, it is overseas students that are key tenants. The good news is that the UK still appears to be keen on attracting international students, and just as importantly young people from abroad continue to show a healthy appetite for Britain’s well-respected universities.

The government wants to increase the number of overseas students by 30 per cent by 2030, while Britain’s new prime minister, Boris Johnson, has said foreign students will be able to stay and work in the UK for two years after graduating, backtracking on the home office’s previous, more restrictive stance. Meanwhile, acceptances of EU students to UK universities were up 3.8 per cent in the current academic year and 4.9 per cent for non-EU students. UCAS estimates increases for the next academic year of 1.0 per cent and 7.9 per cent, respectively.

This is a good backdrop for GCP. But there are signs that the real estate investment trust (Reit) is in danger of becoming a victim of its own success. The company’s strong track record – annualised shareholder returns of 12.9 per cent since its 2013 float – is built on targeting regions where student accommodation is in short supply and is expected to remain so due to planning restrictions. GCP is particularly focused on London, but is also developing two properties in Brighton, which it judges to have similar characteristics to the capital.

The problem is, the attractive fundamentals and scarcity of properties in these areas is causing property prices to rise. This means the potential returns for buyers, such as GCP, are falling and growth could be curtailed as a result.

The attractive dividend yield on offer also needs to be seen in light of a lack of earnings cover. Last year only around 85 per cent of the payment was covered, although the company believes it will be paying all of the dividend from ongoing profits once properties it currently has under development are up and running.

Still, it is never entirely comfortable when a property company is paying shareholders income out of capital, especially when it has only recently raised capital from shareholders by issuing new equity, as GCP did with two placings raising £43.1m in its last financial year.

Rightmove

Property advertising website Rightmove (RMV) is one of the best examples on the UK market of the so-called 'network effect' in action. Put simply, as more people use the site (both estate agents and house hunters) the more valuable it becomes for all involved, and Rightmove has extracted that value for its shareholders over many years. Indeed, so important is Rightmove to finding potential buyers, that few estate agents would dare not have a listing and few sellers would want to list with an agent that didn’t. The dominance has allowed Rightmove to progressively increase listing fees, which are charged per estate agent office, while also selling more advertising extras. It makes for a great business.

The icing on the cake is that Rightmove has very limited capital needs, which means it throws off cash as it grows and has returned spadefuls of the stuff to shareholders.

The fact that Rightmove charges estate agents by the office helps insulate it from the ebbs and flows of the housing market, but only to a degree. What the company cannot protect itself from is estate agent closures. In its first half there were some signs of closure-related sales weakness, but this was more than made up for by rising spending per advertiser and increased new-home listings. Rival Zoopla has more recently reported more pronounced weakness, which suggests closures could be picking up pace. However, to a degree this may simply be a reflection of hard-pressed estate agents consolidating ad spending with the market leader, Rightmove.

Rightmove weathered the last recession reasonably well. But the fact that spend per advertiser has increased by 3.5 times in the past 10 years to £1,077m means a downturn today may be more keenly felt now than it was in the past, as there may prove less scope to keep raising advertising rates to counter falling customer numbers. But it’s the high rating commanded by the shares that looks most vulnerable to disappointments.

Marshalls

Building products group Marshalls (MSLH) was the standout performer from last year’s screen. And it’s not hard to see why investors are so keen on its shares. In a flat construction market it has experienced impressive sales growth, both on a like-for-like basis and thanks to last year’s acquisition of concrete product company Edenhall. As well as winning market share, the company has been capitalising on trends such as increased urbanisation and pedestrianisation. Product innovation has also been key to driving sales and margins. Meanwhile, planning restrictions have helped restrict the supply of many types of building material.

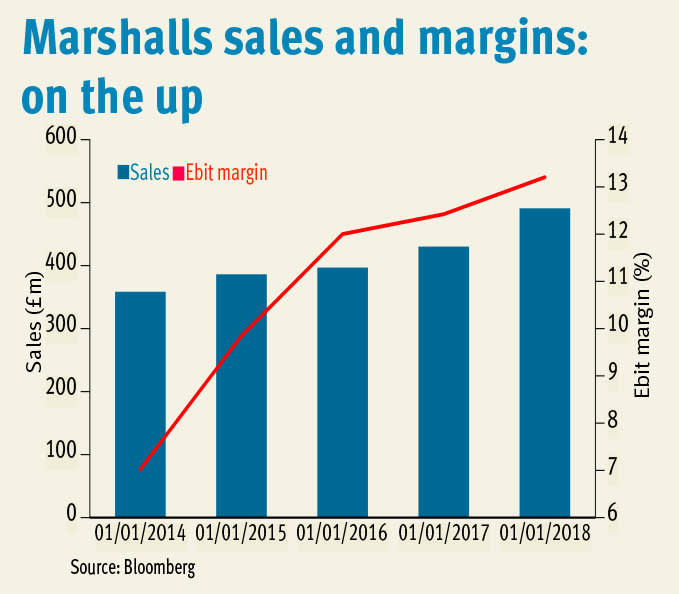

The strong investment story has been reflected in several years of impressive sales growth on improving margins (see chart).

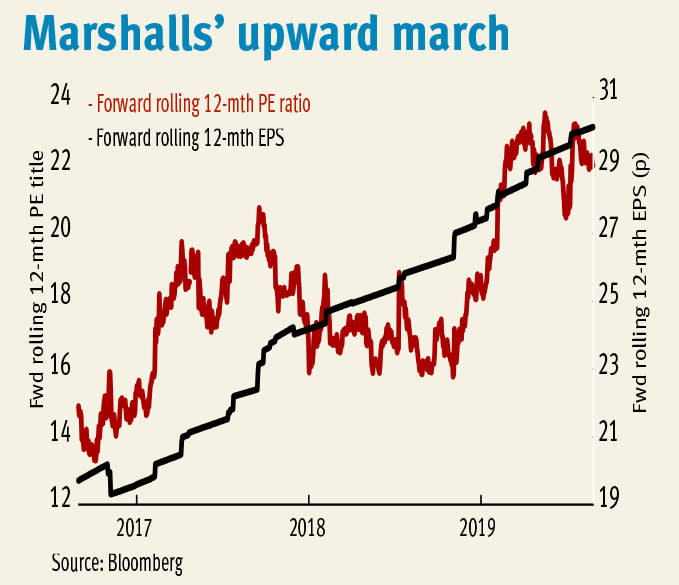

The relentless improvements have prompted broker forecast upgrades and a rerating of the shares (see chart).

The company has recently put together a new five-year plan aimed at delivering more of the same. Management has identified eight “pillars” to drive growth, which include moving into new product areas, increasing efficiency, improved customer engagement and product innovation. That said, end markets are cyclical and the sheer extent of progress over recent years – both operationally and in share price terms – will be hard to maintain.