A forecast dividend yield of close to 10 per cent is always going to inspire caution among investors. Weaker-than-expected services revenue during the third quarter sent shares in Vodafone (VOD) down to a 12-month low, increasing concern towards the sustainability of the telecoms giant's dividend. Services revenues slipped by 3.9 per cent year on year on a reported basis to €9.8bn, or by 0.8 per cent organically – behind analysts’ consensus estimate of 0.7 per cent. Meanwhile, group revenue dipped 6.8 per cent to €11bn (£9.5bn) for its third quarter to December 2018, which management attributed to the adoption of the accounting standard IFRS15, along with the disposal of its Qatar business and adverse currency movements.

The majority-owned southern Africa business, Vodacom, was partly responsible for the third-quarter decline in services revenue. Organic revenues here rose 1.5 per cent, lower than consensus estimates of 3.8 per cent, which management blamed on a “challenging macroeconomic environment” and a “sharp slowdown” in data revenue growth.

German service sales rose 1.1 per cent – slower than the second quarter’s 1.7 per cent growth – and consensus estimates of 1.5 per cent. A reduction in wholesale mobile virtual network operator revenues here counterbalanced good customer-base growth in mobile and fixed-line telecoms. Germany is becoming an increasingly important market and, following last year's Liberty Global acquisition (should the deal go through), RBC Capital Markets estimates that it will constitute around 40 per cent of group enterprise value.

Italy and Spain also continue to face price competition, but organic services revenues for both countries and the UK were better than market estimates. Vodafone has also agreed heads of terms to extend its UK network-sharing arrangements with Telefonica O2 to include 5G. Once arrangements have been finalised, it will consider the “monetisation” of its UK tower infrastructure.

Yet Vodafone’s shares are priced for catastrophe, with concerns mounting that the group could cut its payouts to investors. The purchase of assets from Liberty Global will add to its already sizeable debt pile – €32.1bn at November’s half-year results.

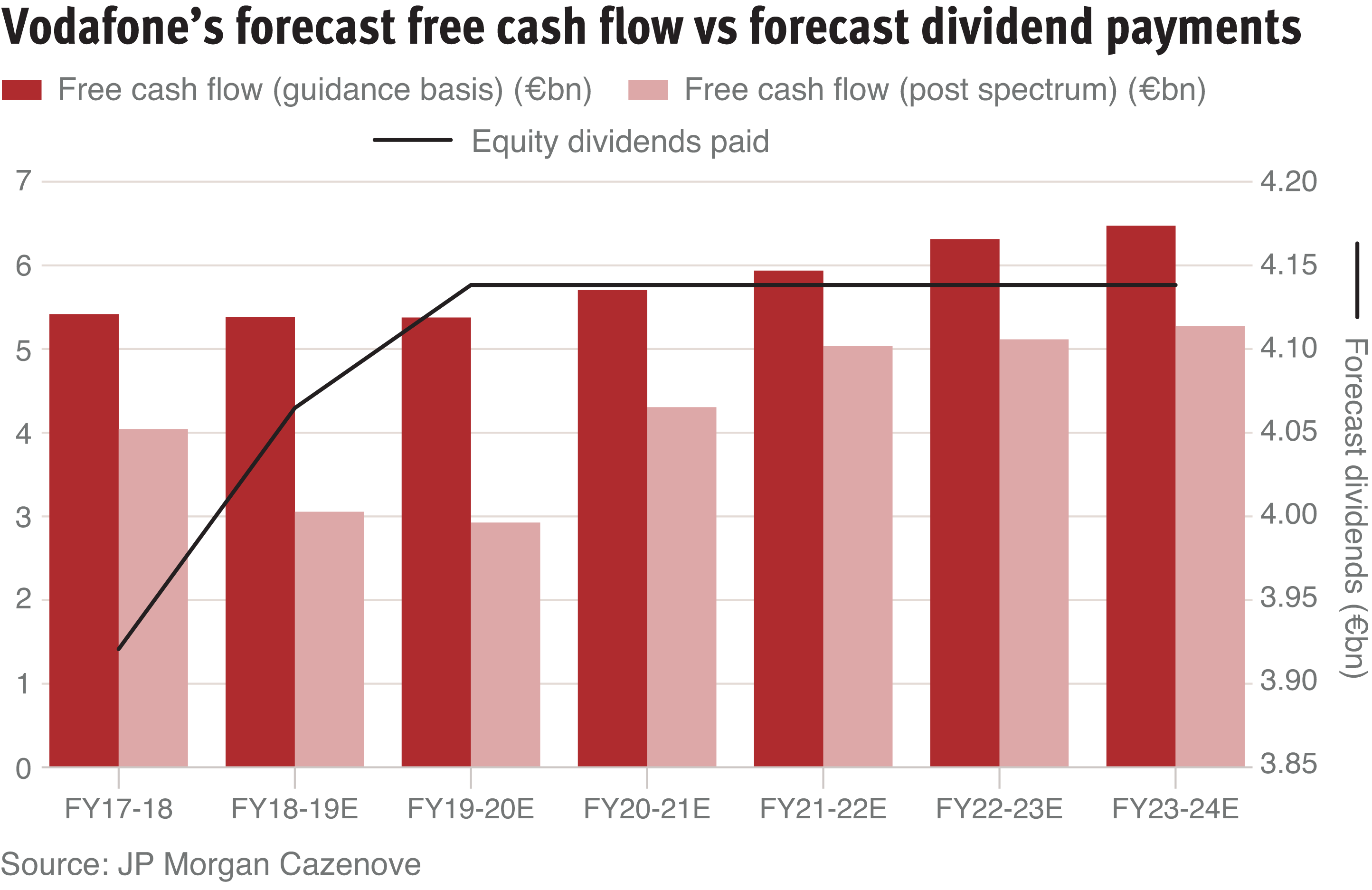

Indeed, while broker Numis and house broker JPMorgan Cazenove assume that a 15ȼ dividend will be sustained, RBC Capital Markets – which rates Vodafone as “underperform” – expects a 10ȼ dividend in FY2020, falling to 0.07ȼ in FY2021.

Key to the maintenance of the dividend is free cash flow, which should incorporate anticipated spectrum spend – essential to Vodafone’s competitive positioning. The dividend will not be covered by post-spectrum free cash flow until FY2020-21, according to forecasts by JPMorgan.

However, Vodafone has other options to reduce debt before slashing the dividend, including a potential sale and leaseback of telecom towers. Reassuringly, management maintained its full-year guidance for FY2019 within its third-quarter update – expecting organic adjusted cash profit growth of around 3 per cent, and pre-spectrum free cash flow of around €5.4bn.

What's more, the group remains on schedule to achieve its target €400m net reduction in operating expenses in Europe and ‘common functions’ during FY2019, and a €1.2bn reduction in operating expenses by FY2021, against FY2018 on an absolute organic basis.

Vodafone has paused the installation of Chinese organisation Huawei’s kit within its core European networks. Chief executive Nick Read says “now is the moment to engage with the security agencies, with politicians and with Huawei to improve everyone’s understanding”.