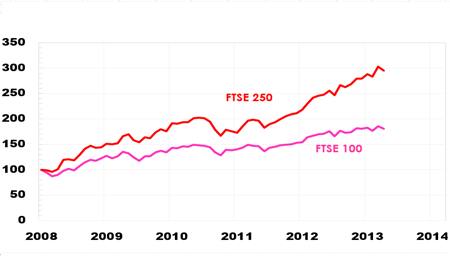

The FTSE 250 has had a storming run over the last five years or so, easily outstripping its big brother. Its total return over that period is about 219 per cent, compared to 127 per cent for the FTSE 100. It has also trounced both the large-cap index and indeed the small-cap index since all three came into existence in the mid-1980s, as I discuss here.

Based on one of my favourite valuation models, the FTSE 250 is indeed much dearer than the FTSE 100, as we might expect. The ShareMaestro programme – which takes into account forecast dividend growth, inflation, and riskiness – put the mid-cap index’s fundamental valuation at 16714.6 as of 27 March, only slightly above its actual price of 16202 on that date.

The full results and assumptions used to get there are shown in the table below. My thanks to ShareMaestro creator Glenn Martin for sending this through.

| FTSE 250 | RESULTS | ||

|---|---|---|---|

| Date | 27 March 2014 | Current Net Dividend | 400.2 |

| Share Name or ID | FTSE 250 | Actual Dividend Growth % p.a. | 6.0 |

| FTSE 250 Price | 16202 | End-Period Dividend | 536.3 |

| Current FTSE250 Net Dividend Yield % | 2.47 | End-Period FTSE 250 Dividend Yield | 3.03 |

| Unadjusted End-Period FTSE 250 | End-Period FTSE 250 Price | 17721.6 | |

| Net Dividend Yield % | 3.25 | Average Dividend Yield | 2.75 |

| Current FTSE100 Dividend Yield % | 3.65 | End-period Investment Value | 20294.1 |

| Average-Period Inflation Rate | 2.94 | Discounted Investment Value | 18553 |

| End-Period Inflation Rate | 3.21 | Projected growth for period % | 25.3 |

| Real Dividend Growth Rate | 3.00 | Projected annual growth % | 4.6 |

| Personal Investment Value | |||

| Risk Premium % | 11 | End-period Investment Value | 20294.1 |

| Redemption Yld % pa 5-yr Gilts | 1.81 | Projected growth for period % | 25.3 |

| Personal Capital Gains Tax Rate % | 0 | Projected annual growth % | 4.6 |

| Personal Extra HR Tax on Divs % | 0 | FTSE 250 Intrinsic Value | 16714.6 |

| Personal Risk Premium % | 0 | Value as % of Current Price | 103.2 |

For the FTSE 100, ShareMaestro’s valuations have provided an excellent guide to subsequent returns over time. A strategy of buying the index whenever its intrinsic value has been at least 105 per cent of its current price and shifting into cash whenever value has gone below 95 per cent of the price would have produced a market-beating performance over the last few decades.

The result for the FTSE 250 backs up my view that the index is still just about worth staying long of for the moment. It is somewhat dear overall, but not yet dangerously so.