Skyward S&P

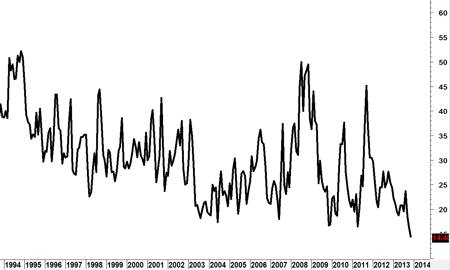

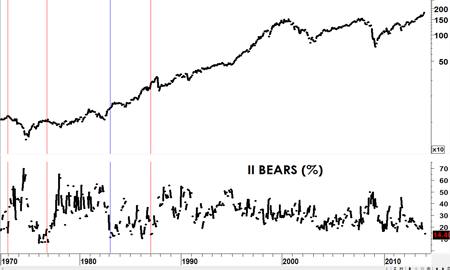

The latest Investors Intelligence report makes eye-catching reading. The gap between bullish and bearish pundits has now widened to a massive 41.4 points, the biggest difference since April 2011. There are fewer bearish US newsletter writers since at any time going back to March 1987, a few months ahead of the almighty crash.

Bears go missing

On the whole, such a dearth of bears seems to have been a feature of late-stage bull markets. There were similarly few pessimistic tipsters in 1966, 1972 and 1976. Strong downtrends followed all of those episodes. It is not inevitable, however. The S&P kept surging in 1963 and then again in 1983, despite a preponderance of bulls.

Bears absent at past tops

I have to say I see few parallels with 1983. Back then, stocks were just one year into a new cyclical and secular bull run. By most fundamental measures, they were screamingly cheap. Today, we are almost five years into a bull market, and only the most brazen of shills would try and claim they offer good value. My stance on Wall Street remains the same: I'm a short-term bull, but a long-term bear.

This is the exact opposite of how I feel about gold. Colin Loveless writes in wanting to know if I am still "starry-eyed about its long-term future as a safe-haven". I have been calling gold lower for quite some time in my online Outlooks. I could hardly do otherwise, given that the yellow metal is plainly in a strong downtrend.

Not everyone shares this logic, though. On the whole, spread bettors seem to be flocking into long positions, at least based on the positioning data I've seen. With gold in the dumps today, for example around $1,242, more than three-quarters of one spread-betting provider's punters are long. This pattern has been true for ages.

To address Colin's point, I am still long-term bullish on gold. The authorities have clearly committed themselves to the path of inflating away the debt. I see the current deflation "scare" as an ironic red-herring. Once the reality of persistent negative real interest rates and money-printing sinks in, I am confident gold will resume its uptrend.

How low might gold fall before it resumes its mighty bull market, @SneezumRaffe wants to know via Twitter? The current sell-off since September 2011 has seen the price drop by more than 37 per cent. This has emboldened gold's many sceptics to declare the boom as having ended, and not unreasonably.

Past gold pullbacks

I would point back to the mid-way stage of gold's last bonanza in the 1970s, where gold halved in price, only then to soar by more than 700 per cent over the next few years. I think it wholly possible that gold will end up falling 50 per cent this time round from its highs of September 2011. That would take it down to well below $1,000. At that stage, few investors will surely believe in the bull case. Gold will likely also be extremely oversold on its monthly chart. And, when the next leg of its bull market then gets under way, I eventually expect $2,500 to be seen.