2. Currency calamity

Donald Trump's election, Britain's decision to leave the EU and political upheaval in several countries sent a raft of world currencies spiralling downward in 2016. The pound gave the Turkish lira and Mexican peso a run for their money as one of the worst performers after the Argentine peso. The Indian rupee also tumbled after the government abolished 500 and 1,000 rupee notes in an ill-conceived effort to crack down on corruption and shift cash from informal activities into the formal economy. Political tensions, threats to trade deals such as Nafta and TPP, and coups and conflicts around the world are likely to mean further volatility in foreign exchange markets in 2017.

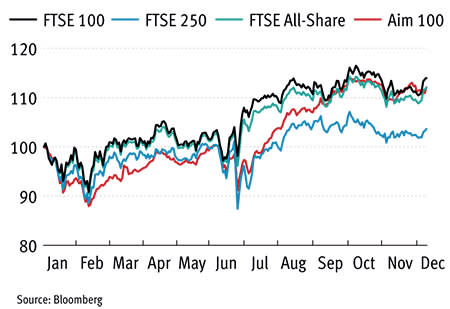

3. Playing FTSE

Rock-bottom interest rates, recovering energy and commodity prices and a resilient domestic economy underpinned solid performances from the UK's major equity indices in 2016. The FTSE 100, FTSE All-Share and AIM 100 all rose about a tenth, upending fears that the EU referendum result would spark a mass exodus from equities. Mining and energy companies - including Anglo American, Glencore and BP - led the charge. The weaker pound also spurred a wave of takeover deals in the second half of 2016, which sent shares in Lavendon, Brammer and other targets rocketing upward. However, the FTSE 250 performed less well as new regulations and a raft of profit warnings took their toll.

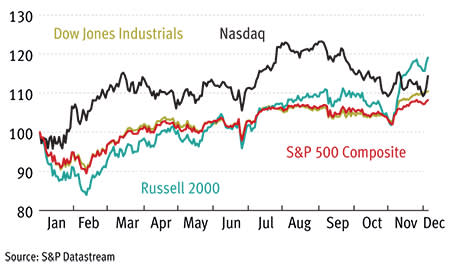

4. Trump triumph

Investors braced for the worst when Donald Trump won the US election, but fears of collapsing stock markets and global turmoil proved largely unfounded. Two weeks after the election, all four of America's major stock market indices - the S&P 500, Dow Jones, Nasdaq and Russell 2000 - closed at record highs for the first time in 17 years. Investors are betting that the incoming president will cut taxes, ramp up infrastructure spending, relax regulations and protect domestic industries (read our feature on US equities here). However, the real estate tycoon has personally intervened in the private sector and derided specific companies such as Boeing (US:BA) and Amazon (US:AMZN), suggesting his administration might not be universally good for business.

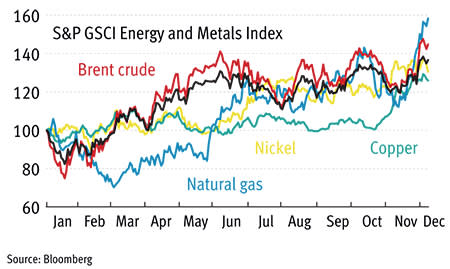

5. Energy boost

After plunging in the second half of 2014 and falling even further a year later, energy and commodity prices have staged a substantial recovery in 2016. The oil price has rallied because producers have agreed to limit supply, while the costs of metals such as copper and nickel have risen on the prospect of massive infrastructure spending and deregulation in the US, as well as the ongoing construction boom in China. However, higher energy prices could encourage more shale gas production in the US and greater use of new technologies such as hydraulic fracturing and horizontal drilling, boosting supply and tempering further price increases. Moreover, the latest Opec deal could fall apart if the cartel's members cheat and ramp up production.

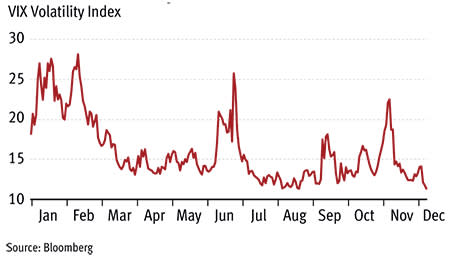

6. Shock and surprise

The Vix volatility index, known as the 'fear gauge', uses the prices of options to measure expectations of stock market volatility over the next 30 days. It surged in January after declines in US equities sparked fears of an economic downturn. It also spiked following the unexpected outcomes of the EU referendum and US election. After a capricious and turbulent year, many investors will cross their fingers for steadier markets in 2017. But the endless wave of cyber attacks, corporate scandals and geopolitical conflicts could mean more surprises lie around the corner.

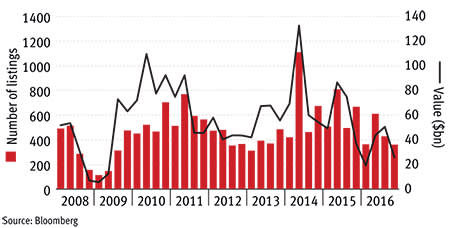

7. Sinking floats

Widespread economic and political uncertainty weighed on the number and pricing of stock market listings in 2016. The value of flotations slumped to a six-year low in the first quarter, while the volume of IPOs fell in all three quarters of the year so far. Pulled UK listings include Misys, Krispy Kreme and Pure Gym. But a recovery could be on the cards: medical products specialist ConvaTec (CTEC) raised nearly £1.5bn in late October, making it the largest London listing this year, while social media group Snap could snag a $25bn market valuation when it floats its shares in the spring.

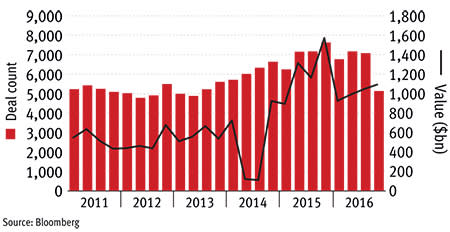

8. Deals unsealed

Despite megamergers such as AT&T's (US:T) $85.4bn takeover of Time Warner and Microsoft's (MSFT) $26.2bn purchase of LinkedIn, the value of global mergers and acquisitions fell sharply in 2016. The volume of deals held up well, perhaps benefiting from the weakened sterling and the post-referendum sell-off in UK shares, which enticed private equity firms to pounce on their targets. However, uncertainty in the US, UK and elsewhere may well have discouraged bigger, riskier bids.