Regular followers of BT (BT.) since the company’s market debut in the 1980s will know the feeling of exhilaration when the telecoms giant looks as though it isabout to deliver the returns that its size and market power would deem to be its divine right. Any investor experiencing such euphoria must exercise caution as, with equally wearisome regularity, there arrives the mirror feeling of dejection and disappointment when the company’s management forms a circle, aims a metaphorical pistol at its collective foot and merrily pulls the trigger.

- Activist investor lockout about to expire

- Pension deficit looks under control

- BT gets a decent fibre deal from Ofcom

- Large parts of the company may have limited residual value

Fundamentally, at the heart of BT’s story over the past 20 years, or so, is the sense that anyone other than whichever board is in place at the time could run the company more effectively. Intriguingly, there is a realistic prospect that investors may finally get to see if someone else can do a better job when the bid lockout clause expires in December for Patrick Drahi’s Altice.

It is notable that while Drahi’s 12.1 per cent stake buys a lot of kudos, he has so far refrained from throwing his weight around. This hasn’t stopped the company from reportedly engaging advisers to lead a potential takeover defence, which suggests definite unease that Drahi will move once the constraints on his being able to make an offer are lifted on 10 December.

For instance, recent news that the company had realised annual savings of £1bn over 18 months earlier than planned looks like a heartfelt cry to shareholders to keep the current and relatively recently appointed management in place. What Drahi would be buying, should that happen, is a company that falls well within the definition of a special investment situation. In essence, many of BT’s issues can be addressed via sustained management action and this makes an interesting opportunity for investors. And even without a bid, Philip Jansen, the turnaround specialist who took the helm as chief executive in February 2019, is already ringing in some noteworthy changes.

Pension gaps and Ofcom

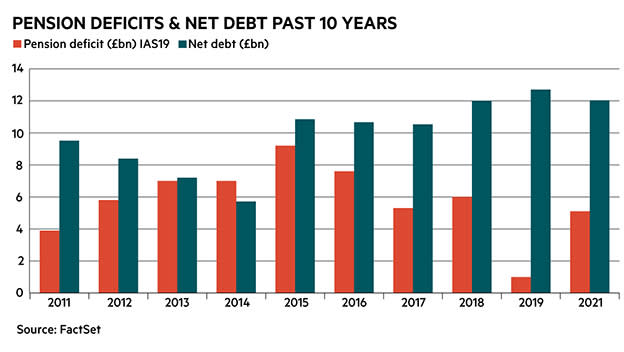

Aaside from the excited speculation over Drahi’s intentions, there are signs that some of the group’s very long-term issues are looking slightly less ominous, starting with the pension scheme. Like many large companies with a large legacy defined-benefit pension scheme, BT regularly gets labelled by the lazier sort of analyst as a pension fund with a telecoms company attached. In BT’s case, a deficit that had peaked at over £11bn in 2017 has started to move decisively in the right direction after an IAS valuation at the half-year result stage lowered this figure to £4.3bn net of deferred tax – still sizeable but certainly far more manageable. The strength of equities and a general trend for companies to gradually shift the risk of defined-benefit schemes to the life assurance sector has helped to improve the outlook for pension deficits across a range of companies.

The other reason that investors started to take more interest this year is that BT received a surprisingly easy ride from Ofcom over pricing for the new fast fibre network. Ofcom’s statement is worth quoting to illustrate the point: “Openreach’s fastest fibre services will continue to be free from pricing regulation...since people can choose the entry-level service as an alternative. Openreach can also charge a bit more for regulated products that are delivered over full fibre instead of copper, because full fibre is consistently faster and much more reliable.”

The inference from the regulator’s statement is that there will be no price caps on the fast fibre network, which given the estimated £15bn cost of installation, means BT stands a much better chance of generating a decent long-term return. The company is already offering 10-year pricing agreements to wholesale communications providers, for instance, which could hugely improve the visibility of earnings. Coincidently, Drahi’s investment came three months after Ofcom reached its decision.

Breaking up is hard to do

The news that large conglomerates such as GE are looking to break themselves up suggests one way in which BT could generate significantly greater value for shareholders. As it now stands, the company is a strange hybrid of business units that does everything from global business consulting to fibre broadband, to legacy landlines to, erm, sport.

Like an embarrassing uncle at a wedding, the most obvious candidate for the chop is BT Sport, which is under strategic review according to the last interim results. Apart from the longstanding issue over whether creating content is worth the effort, BT Sport never made enough of an impact with paying subscribers since starting in 2012, although it did help to stem the loss of broadband customers. If BT Sport is to be divested or partnered, then most investors would probably appreciate some sort of agreement before the next round of sports rights bidding next year. Otherwise BT could face the prospect of having to spend money on rights in order to have a worthwhile asset to sell. That said, its all important Premier League football rights are already agreed until 2025. It was reported earlier this year that talks were in progress with established streaming services over a potential sale or a joint venture, but there has been no further news.

The other division that looks increasingly out of place is BT Global. The division, then called Global Services, was the source of a huge accounting scandal in Italy that emerged in 2017. The £530m accounting fraud is still an ongoing issue, even though BT broke up its Italian division and sold it for scrap to Telecom Italia in 2020, as several former BT Global Services executives are currently answering fraud charges.

Since assuming the reins as chief executive, Jansen has sold off peripheral parts of Global, including a Latin American subsidiary for £110m. However, the sheer scale of its global operations means downsizing has proved to be a long process, with an often notable absence of willing buyers. With that in mind, a simpler solution might be a straightforward spin-out of Global into a separate listed company, leaving BT as a focused broadband fibre and mobile network supplier in the UK.

Getting rid of Global would not make a huge difference to the company's bottom line. For example, at the last annual results Global generated £3.73bn of revenues, but just £191m of operating profit for an operating margin of 5 per cent. By contrast, Openreach had sales and operating profits of £5.24bn and £1.23bn, respectively. In other words, Global seems barely able to cover the cost of its operations.

Cheap as chips?

Whatever ultimately happens with Drahi as a potential bidder, BT is turning into a fascinating corporate story in ways that does not relate to its propensity for self-inflicted wounds. The business looks far more focused than it did in 2019, when the current chief executive took over, and any new management action would build on those foundations. In pure valuation terms, the shares look cheap by almost every measure and hold steady at a price/earnings ratio of barely eight times Berenberg’s EPS forecasts for 2023 – this for a business that has historically generated a return on employed capital (ROCE) of 10 per cent. It is true that ROCE has been heading down, but with a free rein on fibre pricing, margins are forecast to improve from here (see table).

| BT's profits start to stabilise | ||

|---|---|---|

| YEAR | ROCE (%) | OPERATING MARGIN (%) |

| 2016 | 10.8 | 19.8 |

| 2017 | 9.40 | 16.4 |

| 2018 | 9.69 | 16.8 |

| 2019 | 8.95 | 15.5 |

| 2020 | 7.47 | 14.7 |

| 2021 | 5.90 | 14.4 |

| 2022* | 6.30 | 15.3 |

| 2023* | 6.80 | 16.2 |

| Average | 8.16 | 16.1 |

| Source: FactSet, *Berenberg forecasts | ||

Drahi’s investment seems to have put a floor under the share price, which is a welcome first step, and news of a private equity bid for rival Telecom Italia may have sparked some fresh momentum. The extent to which BT’s new fibre network delivers recurring revenues on top of its huge capital investment will be important for share price progress, too. That strategy could return BT to being a stable and predictable source of investor returns. Remaining a sprawling and unconnected pseudo-conglomerate is longer a seems viable option for whoever ultimately takes charge at the company.

| Company Details | Name | Mkt Cap | Price | 52-Wk Hi/Lo |

| BT (BT.A) | £16.3bn | 165p | 207p / 117p | |

| Size/Debt | NAV per share* | Net Cash / Debt(-) | Net Debt / Ebitda | Op Cash/ Ebitda |

| 118p | -£18.8bn | 2.5 x | 73% |

| Valuation | Fwd PE (+12mths) | Fwd DY (+12mths) | FCF yld (+12mths) | CAPE |

| 8 | 4.7% | 4.9% | 7.3 | |

| Quality/ Growth | EBIT Margin | ROCE | 5yr Sales CAGR | 5yr EPS CAGR |

| 14.3% | 8.1% | 2.5% | -12.2% | |

| Forecasts/ Momentum | Fwd EPS grth NTM | Fwd EPS grth STM | 3-mth Mom | 3-mth Fwd EPS change% |

| 5.7% | -1% | -5.0% | 1.8% |

| Year End 31 Mar | Sales (£bn) | Profit before tax (£bn) | EPS (p) | DPS (p) |

| 2019 | 23.4 | 3.16 | 26.3 | 15.4 |

| 2020 | 22.8 | 2.84 | 23.5 | 4.6 |

| 2021 | 21.4 | 2.29 | 18.7 | 0.0 |

| f'cst 2022 | 21.0 | 2.30 | 19.2 | 7.7 |

| f'cst 2023 | 21.2 | 2.45 | 20.6 | 7.8 |

| chg (%) | +1 | +7 | +7 | +1 |

| source: FactSet, adjusted PTP and EPS figures | ||||

| NTM = Next Twelve Months | ||||

| STM = Second Twelve Months (i.e. one year from now) | ||||

| * includes intangibles of £9.9bn or 135p per share | ||||