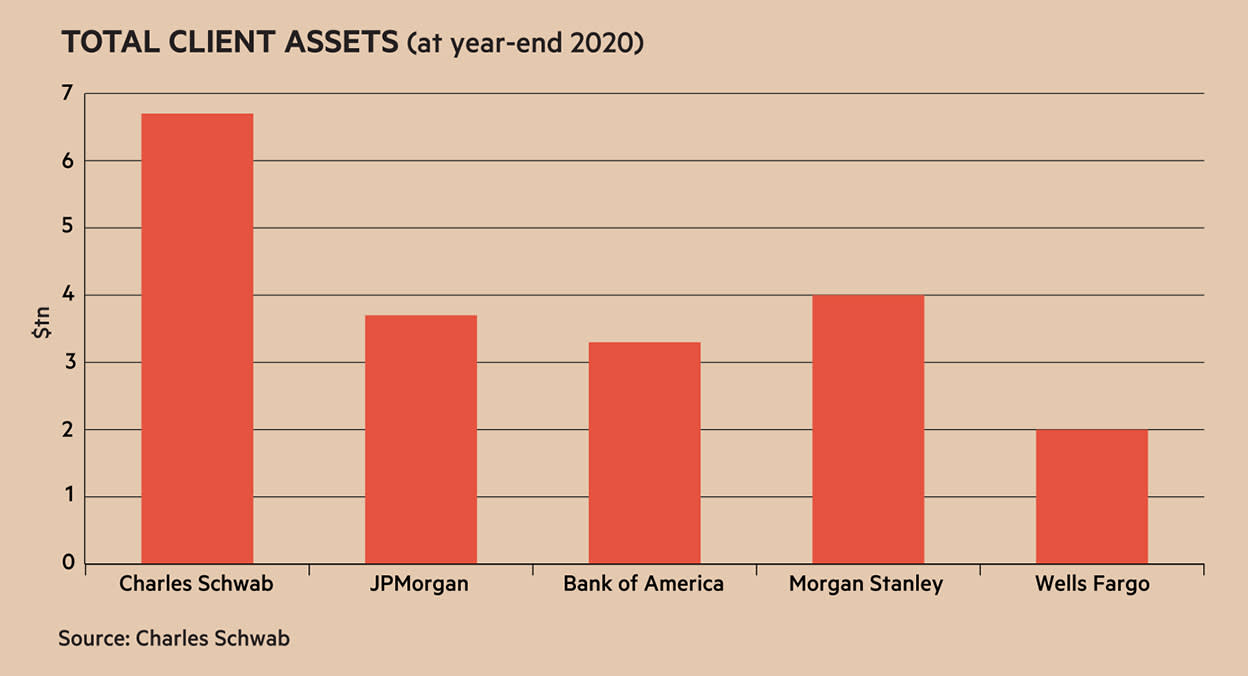

Some companies deal in sums of money so large that it can feel like the numbers cease to be meaningful. Charles Schwab (US:SCHW) is one such business. Founded in California in 1971, Schwab pioneered discount broking in the US and its services now span wealth management, securities brokerage, asset management, banking, and financial advice. It handles almost $8 trillion of client assets, 33m brokerage accounts and – somehow – it is still growing.

- Growth in client assets

- Exposure to American household savings

- New wave of retail investors

- Competitive market

- Sensitive to asset prices

The world of American sharedealing is blisteringly competitive. Established wealth managers and scrappy start-ups battle for customers, who are subsequently sold a batch of other financial services. In 2019, Schwab upped the ante, ditching trading commissions for US and Canadian-listed stocks and exchange traded funds (ETFs). This put pressure on its rivals to do the same, and directly challenged the likes of Robinhood (US:HOOD) which target young investors with colourful apps and zero-commission trades.

Some worried that the gambit would damage Schwab’s revenues and erode its margins – and their fears weren’t unfounded. Trading revenue decreased by 17 per cent in wake of the cut and pre-tax profit margins narrowed to an (albeit still roomy) 37 per cent in 2020, from 42 per cent in 2019. However, the lion’s share of Schwab’s revenue comes not from commission but from net interest – which is derived from idle cash in client accounts – meaning the group was well placed to withstand the pressure.

Some of Schwab’s peers proved less hardy, and the commission cut laid the groundwork for a $22bn takeover of TD Ameritrade – the largest brokerage acquisition in history and a key factor in the group's investment case. The merger increased 2020 calendar year revenue by $1.7bn of revenue and added $1.6 trillion in client assets, meaning the combined company now towers over the industry.

The sheer size of Schwab works in its favour, helping it to attract more investors and to spread operating costs over a larger client base. It is also targeting savings of $1.8bn to $2bn from combining the two groups. Its competitors have had a similar idea, however: last year, Morgan Stanley acquired online trading platform ETrade for $13bn. Scale matters in mass market wealth management.

Lockdown lull

Stripped of TD Ameritrade's contributions, Schwab’s lockdown performance was underwhelming. The group suffered at the hands of economic volatility, and falling interest rates negatively impacted revenue and caused it to waive management fees for certain funds.

Customer service also took a hit. Schwab said that its client service response and processing times increased during lockdown, and some customers struggled with delays on its website and mobile apps. In a market where brokers are competing for customers – and where the technology is getting ever slicker – client satisfaction is particularly important.

Schwab’s results reflected the difficult environment. Organic revenue fell to $10.0bn in calendar year 2020 – down from $10.7bn in 2019 and $10.1 in 2018 – while basic earnings per share fell by 21 per cent to $2.13. Return on equity also dropped from 19 per cent in 2019 to 9 per cent in 2020. However, adjusting for the impact of the TD Ameritrade deal, return on tangible common equity was still 15 per cent.

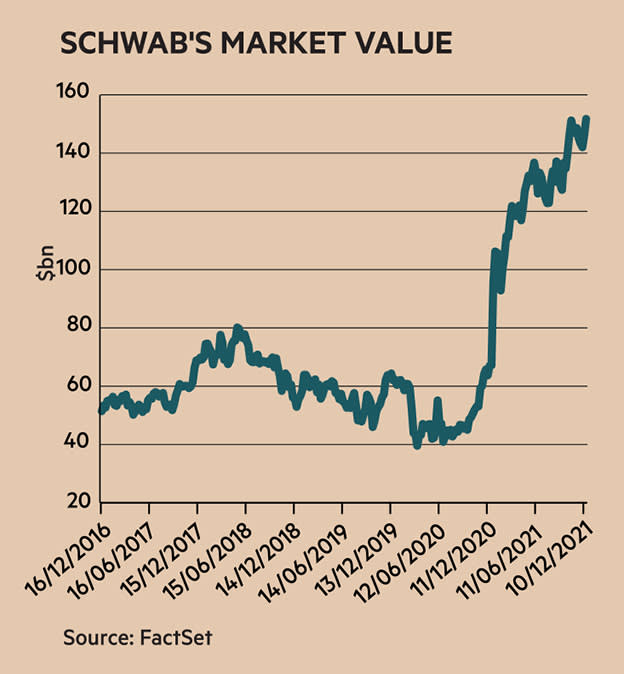

Over the past few months, however, the group has rebounded strongly. Third-quarter results for 2021 show that core new net assets have grown by 8 per cent organically. Meanwhile, net interest revenue is on the rise as a result of its broader asset base, while profits margins are expanding once again. Tthe Federal Reserve's plan for three rate rises will also add a tailwind. Looking ahead, consensus broker estimates suggest strong sales and profit growth is on the horizon, with EPS due to reach $3.64 for calendar year 2022.

It’s also important to note that the group has certain counter-cyclical qualities. If clients de-risk and keep their cash in their Schwab bank account, it becomes a net positive. Similarly, high interest rates – which spell trouble for many businesses – can boost Schwab’s earning power, without attracting the same credit risks as traditional banks, which can be hit by customers defaulting on loans. “It is appealing from a diversification standpoint,” says Giorgio Caputo, senior fund manager at JO Hambro Capital Management.

Generation investor

Wealth management is evolving. In the early stages of the pandemic, a body of young retail investors emerged, funnelling their lockdown savings into the exuberant US equity market. A study by Schwab found that 15 per cent of US stock market investors began investing in 2020 – and many are bullish about their prospects.

'Generation Investor' is around 35 years old, it found – compared with a previous median age of 48 – and earns around $20,000 less in annual income than the traditional retail investor.

This fresh-faced customer base could be interesting opportunity for Schwab. On the one hand, the group faces obvious competition from apps such as Robinhood. However, such companies face accusations of “gamifying” the stock market and encouraging risky behaviour by inexperienced investors. (Robinhood’s share price has slid since it listed in July.) Established companies could well benefit from the fallout, if US stocks continue to climb.

It’s not just retail investors that Schwab is seeking to entice, however. It also provides tools for financial advisors looking for more flexible ways of working. In October, it announced a digital makeover for one such platform. According to management, the redesign reflects “overall efforts to continue to integrate technology from both firms and deliver an industry-leading experience”.

The valuation of Schwab’s shares is high: they currently trade at over 22 times consensus earnings. However, with its mammoth client base and ever-extending reach, a diminutive valuation would ill-suit the American behemoth which – according to management – still has over $40tn of investable wealth to play with.

| Company Details | Name | Mkt Cap | Price | 52-Wk Hi/Lo |

| Charles Schwab Corporation (SCHW) | $148bn | $81.60 | 8,492c / 5,061c | |

| Size/Debt | NAV per share* | Net Cash / Debt(-)* | Net Debt / Ebitda | Op Cash/ Ebitda |

| 3,099c | $40.5bn | - | 348% | |

| Valuation | Fwd PE (+12mths) | Fwd DY (+12mths) | FCF yld (+12mths) | CAPE |

| 22 | 1.0% | 4.4% | 43.1 | |

| Quality/ Growth | EBIT Margin | ROCE | 5yr Sales CAGR | 5yr EPS CAGR |

| - | 9.6% | 13.5% | 15.5% | |

| Forecasts/ Momentum | Fwd EPS grth NTM | Fwd EPS grth STM | 3-mth Mom | 3-mth Fwd EPS change% |

| -14% | 19% | 14.7% | 6.7% | |

| Year End 31 Dec | Sales ($bn) | Profit before tax ($bn) | EPS (c) | DPS (c) |

| 2018 | 10.1 | 4.55 | 245 | 46.0 |

| 2019 | 10.7 | 4.85 | 267 | 67.8 |

| 2020 | 11.7 | 4.30 | 245 | 71.9 |

| Forecast 2021 | 18.5 | 8.28 | 326 | 72.0 |

| Forecast 2022 | 19.6 | 9.27 | 366 | 78.3 |

| Change (%) | +6 | +12 | +12 | +9 |

| Source: FactSet, adjusted PTP and EPS figures | ||||

| NTM = Next 12 months | ||||

| STM = Second T12 months (ie, one year from now) | ||||

| *Includes intangible assets of $21.9bn, or 1,213¢ a share | ||||