We are all geniuses in retrospect. Still, we can confidently say predictions of a housing market slump in 2023 were very wrong. Interest rates rose to levels not seen since 2008, but the housing market remained surprisingly sturdy.

First, we should give the forecasters some credit. House price data is a fiendishly tricky thing, and not everyone is looking at the same numbers. The Office for National Statistics (ONS) measures prices at completion; Halifax and Nationwide use data from their mortgage customers; Rightmove measures asking prices; and Savills measures house value, which ignores transactions entirely. Still, the consensus assumption from many experts was that over the 12 months to the end of 2023, house prices would sink by between 5 and 10 per cent on one metric or another.

Admittedly, the 2023 calendar year is an arbitrary window for forecasting or recording data. Still, the slump did not happen. Not even close. Nationwide ultimately recorded a 1.8 per cent fall in prices in 2023, the ONS said 1.4 per cent, Rightmove 1.1 per cent, Savills said house values dropped a mere 0.3 per cent, and Halifax said prices rose by 1.8 per cent. For housing forecasters, 2023 was a predictive error equivalent to the Brexit vote, or Donald Trump's presidential win. An anomaly they should have seen coming but did not.

In theory, rising interest rates hit buyers and owners alike. The former can no longer afford higher house prices because mortgages are more expensive. Meanwhile, many of the latter are forced into selling because they can no longer afford their mortgage.

Yet in 2023, owners held onto their homes because many more were on fixed-term mortgages than during the 2008 downturn, when variable-rate mortgages were much more popular. Rising wages and low unemployment, unlike in 2008, also helped them keep up with payments. So, even though buyers' budgets shrank, sellers had less need to sell. The stand-off kept house prices as they were.

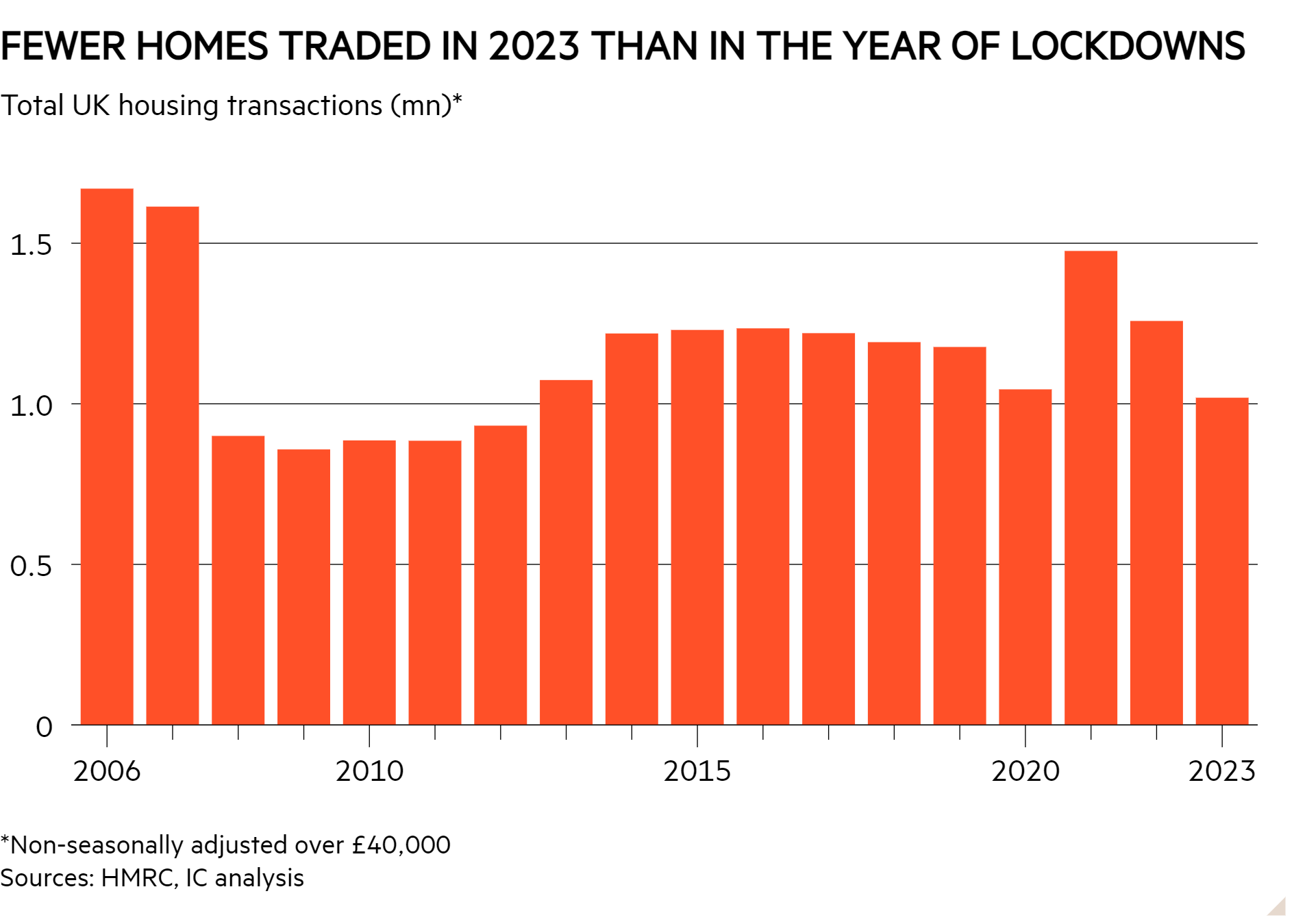

The numbers bear this out. IC analysis of HMRC data found that 2023 saw the lowest number of transactions in over a decade (see chart), and although mortgage arrears rose, they were nowhere near 2009 levels. In other words, most from the limited pool of sellers were not in dire straits.

The 'I told you so' award goes to the Joseph Rowntree Foundation (JRF), which outlined precisely how and why everything that happened would happen in a report from February 2023. In summary, its view was that all of the above combined with the persistent housing crisis keeping supply low would keep demand high even if budgets dropped.

But the JRF might turn out to be wrong, too. Bank of England data confirms that many homeowners will need to remortgage at higher rates between now and the end of 2026. As such, the central bank predicts monthly payments will rise to 9 per cent of post-tax income. It might not sound like a high figure to Londoners spending 35 per cent of their income on rent, but the figure is an average, meaning many homeowners will be in worse positions. It would also be the highest level since 2009.

Will this lead to a slump in house prices between now and 2026? Many of the same forecasters who were wrong about 2023 have revised their forecasts for 2024, anticipating anything from a 3 per cent drop to a 3 per cent rise. Your guess is as good as mine, but predictions of a significant fall have clearly tailed off.