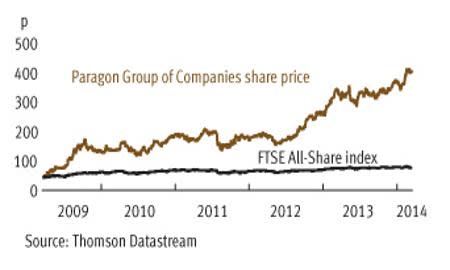

Buoyed by robust demand for rented accommodation, The Paragon Group of Companies (PAG) - which offers buy-to-let mortgages to professional landlords - has been growing at quite a pace. What's more, Paragon's niche market looks unlikely to slow any time soon, leaving the lender's shares set for more upside.

- Strong buy-to-let loan demand

- Very low arrears

- Increasingly diversified

- Banking licence offers new opportunities

- Nothing special dividend yield

- Sensitive to rising interest rates

In basic terms, demand in the rented sector is being driven by the structural under-supply of housing in the UK. That, in turn, is pushing up the price of the existing housing stock and prices have received a further boost from the government's help-to-buy scheme - that fuelled demand further by making mortgages more affordable for first-time buyers. Indeed, UK house prices rose 8.8 per cent during 2013 alone. Accordingly, a growing proportion of the population is being priced out of the market which, in turn, is boosting demand in the rented sector. In fact, property consultant Knight Frank said last month that the UK's private rented sector had doubled in size since 2000 to around 4m households and, significantly, it expects that figure to grow by a further 1m by the end of 2016. Rents are rising solidly as well - up 2.9 per cent in 2013, with regional hotspots (such as Manchester) having seen significant faster rental growth.

That adds up to a great story for those seeking to buy houses to rent out, but also for those that lend to them - such as Paragon, which generates about two-thirds of its profit from buy-to-let lending. In fact, buy-to-let mortgage demand has soared and figures from the Bank of England revealed that the value of new buy-to-let lending in 2013's third quarter had jumped 42 per cent year on year to £5.9bn. That demand is readily apparently at Paragon, too, and loan completions in the three months to the end of December rose threefold compared with the previous year. "We expect that activity to pick up further in the spring time," reckons analyst Gary Greenwood of broker Shore Capital. Yet Paragon's credit quality is actually improving, with a mere 0.31 per cent of loans in arrears at end-December, compared with 0.44 per cent a year earlier.

PARAGON GROUP OF COMPANIES (PAG) | ||||

|---|---|---|---|---|

| ORD PRICE: | 399p | MARKET VALUE: | £1.22bn | |

| TOUCH: | 399-400p | 12-MONTH HIGH: | 415p | LOW: 282p |

| FORWAR DIVIDEND YIELD: | 2.2% | FORWARD PE RATIO: | 13 | |

| NET ASSET VALUE: | 285p | |||

| Year to 30 Sep | Pre-tax profit (£m)* | Earnings per share (p)* | Dividend per share (p) |

|---|---|---|---|

| 2011 | 81 | 19.6 | 4.0 |

| 2012 | 94 | 23.5 | 6.0 |

| 2013 | 104 | 27.5 | 7.2 |

| 2014* | 114 | 29.0 | 8.0 |

| 2015* | 121 | 30.7 | 9.0 |

| % change | +6 | +6 | +13 |

*JPMorgan Cazenove forecasts, adjusted PTP and EPS figures Normal market size: 5,000 Matched bargain trading Beta: 1.29 | |||

Paragon isn't just dependent on buy-to-let lending to drive growth, either, and has also diversified into consumer finance. Admittedly, the £400m or so book here is small compared with the £8.3bn buy-to-let book. But in the year to the end of September, the consumer finance arm boosted operating profit by 23 per cent to £39.7m. The group has also been developing its Idem Capital business, which buys unsecured loan books from banks looking to shrink their balance sheets, usually at a big discount to their pay-back value. Moreover, Paragon has now launched a banking subsidiary - it received its banking licence last month. It's already offering motor finance and will launch savings products and personal loans later this year. The banking unit's ability to raise retail deposits could provide a valuable source of funding for Paragon, too.

Not that Paragon has any real funding concerns yet. In factd, to support its growth the group has £450m in warehouse loan facilities available and, in January, its £200m warehouse facility from Lloyds was renewed "on finer terms" until 2016. Paragon is also successfully packaging up mortgages and securitising them - that is, selling them on - with the proceeds being used to refill its warehouse facilities. Paragon has successfully tapped the retail bond market as well - it raised £60m of funds in this way in 2013 and another £125m in January. Significantly, the 6.125 per cent annual coupon on this latest bond is significantly higher than the uninspiring prospective dividend yield (around 2 per cent) available on the shares.

But the importance of today's ultra-low interest rate environment shouldn't be underestimated. Low interest rates drive demand for credit and help borrowers to service their loans, which keeps arrears low. Both demand and credit quality, therefore, will probably suffer once rates start rising. That said, the threat from rising rates is hardly imminent - the consensus among economists is that the first base rate rise isn't likely until mid-2015.