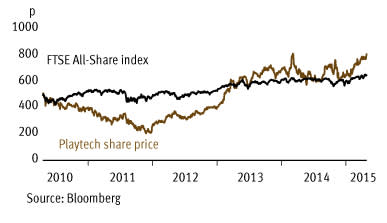

There are few gambling companies you can rely on for consistent growth. But Playtech (PTEC) has proved that finding a niche - in its case gambling software - means you can continue to grow a business even in a changeable regulatory environment. And while its business model is well-established, stellar annual results and a recent acquisition means the company looks set to embark on a new chapter in its growth story, which is not reflected in the share price.

- Strong growth track record

- Recent earnings-enhancing acquisition

- Attractive rating and analyst upgrades

- Net cash

- Regulatory environment

- Tight ownership

Playtech had a killer 2014. In fact, bosses were so bullish they upgraded earnings guidance at the half-way stage, only to smash those targets by reporting a 30 per cent increase in full-year adjusted cash profit to €207m (£151m). A slew of new business wins with the likes of high street bookie Ladbrokes (LAD) and a nationwide rollout with Coral betting shops left like-for-like sales up 13 per cent as well. The casino division is Playtech's growth engine and sales there rose 29 per cent last year to €244m, as the number of mobile contracts and new licensees jumped.

For those questioning whether Playtech has room left to grow, the Coral deal is important. Chief executive Mor Weizer said at the time of the results that the kind of deal Playtech had struck with Gala Coral - a 10-year partnership worth €5m a year in pre-tax profit to provide the gambling group with all of its online betting technology - would become an "industry standard". Traditionally, the company has signed 'single-product deals' with gambling operators to provide either casino software or poker software. The Coral deal marks the first time Playtech has agreed a comprehensive package of gambling technology for one operator. Mr Weizer said the deal "had not gone unnoticed" by the industry.

Playtech is also diversifying its business. In early April it agreed to buy a 91.1 per cent stake in TradeFX, an online contracts for difference (CFD) and binary options broker, for €208m upfront, and a further €250m payable in 2018. There's also a call option on a further 8.9 per cent stake exercisable in 2019. The deal was well-received by City analysts who claim Playtech got TradeFX on the cheap and will be able to sell its products to its existing 120 licensees, very few of which are believed to have CFD or binary options software. Playtech is also hoping to bump up TradeFX's B2B customer base, which only accounts for 3 per cent of revenues at present.

Analysts at Investec predict the deal will be significantly earnings enhancing for Playtech. The broker upped 2015 EPS forecasts by 12.4 per cent and 2016 EPS by 24.7 per cent. This means EPS is now forecast to grow by 22 per cent this year and 27 per cent the year after. Cash profit estimates for the current year and 2016 were upped by 12 and 24 per cent, respectively, as well. The deal should also improve the perceived 'quality' of Playtech's earnings. In the online-gambling world, earnings quality relates to the percentage of sales coming from less-risky regulated markets. Investec has pointed out that 63 per cent of TradeFX's revenue is locally regulated, and none of it is unregulated. Based on this statistic, Playtech's proportion of regulated revenue increases to 39 per cent from 36 per cent as a result of the deal.

Earnings improvements aside, some may feel uncomfortable about the fact that, not for the first time, Playtech is buying a company that is connected to its founder, billionaire Teddy Sagi. Mr Sagi is the ultimate beneficiary of Telesphere, an 86.5 per cent holder in TradeFX, and Brickington, which owns 33.6 per cent of Playtech.

| PLAYTECH (PTEC) | ||||

|---|---|---|---|---|

| ORD PRICE: | 801p | MARKET VALUE: | £2.4bn | |

| TOUCH: | 801-802p | 12-MONTH HIGH: | 816p | LOW: 571p |

| FORWARD DIVIDEND YIELD: | 3.3% | FORWARD PE RATIO: | 12 | |

| NET ASSET VALUE: | 297ȼ* | NET CASH: | €445m | |

| Year to 31 Dec | Turnover (€m) | Pre-tax profit (€m)** | Earnings per share (ȼ)** | Dividend per share (ȼ)** |

|---|---|---|---|---|

| 2012 | 318 | 168 | 57.1 | 23.2 |

| 2013 | 385 | 169 | 56.3 | 23.2 |

| 2014 | 457 | 194 | 58.8 | 26.4 |

| 2015** | 597 | 236 | 71.7 | 28.7 |

| 2016** | 757 | 300 | 90.9 | 36.4 |

| % change | +27 | +27 | +27 | +27 |

Normal market size: 3,000 Matched bargain trading Beta: 0.86 *Includes intangible assets of €381m, or 130ȼ a share **Investec forecasts, adjusted PTP and EPS figures, excludes 34.1p special dividend in 2013 £1=€1.39 | ||||