This poses the question: how much worse could things get? For equity investors, few issues could be more important. There has for years been a close link between economic activity and equity returns; since 1996 the correlation between annual growth in world trade and annual returns on the FTSE All-Share index has been a hefty 0.56. During this time, we have not seen decent returns on equities without decent growth in world trade. The health of the world economy is therefore crucial for investors.

US yield curve and industrial production

However, we cannot look to economic forecasters for comfort here. They have consistently failed to predict recessions, perhaps because these are complex emergent processes which are inherently impossible to foresee (yes, some people did predict the crisis of 2008, but they also predicted crises in 2005, 2006 and 2007 - which was useless for investment purposes).

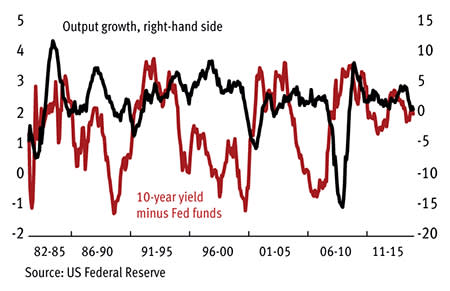

There is, though, one indicator that does have a track record of forecasting recessions: the yield curve. On four of the past five occasions when the US yield curve inverted - in the sense of 10-year yields falling below the Fed funds rate - a recession followed within a few months. And in the past 30 years, we've not had a recession without a prior inversion of the curve.

This isn't to say that the yield curve is a perfect predictor. Upward-sloping curves have been associated with a wide range of subsequent growth rates and inversions tell us nothing about the depth of recessions: the same size of inversion led to a mild recession in the early 1990s but a deep one in 2008-09. Nevertheless, the yield curve is a comfort for investors now. It is significantly upward sloping - 10-year yields are 2 per cent while the Fed funds rate is under 0.1 per cent - and history tells us this implies there's little chance of recession.

Or is there? One reason why yield curves predict recessions is simply that higher short-term interest rates hurt the economy. But it is real interest rates that matter. So, imagine the following scenario. We suffer a deflationary shock such as a fall in aggregate demand which causes real interest rates to rise even as nominal ones are around zero. At the same time, long bond yields stay above short-term ones because markets expect higher rates in (say) five to 10 years' time. In this scenario, we could get a recession even though the yield curve stays upward-sloping.

It could be, therefore, that the ability of yield curves to predict recessions is an artefact of a time of highish inflation. In a time of deflation, things could be different: an upward-sloping curve might be consistent with subsequent recession.

This is only a conjecture. However, two data sets corroborate it.

One comes from Japan since 1990. Its yield curve (defined as the gap between 10-year bond yields and the official discount rate) has been upward-sloping since the late 1980s. But it suffered recessions in 1993, 1998, 2009 and 2011.

Another is the UK's experience in the 19th century. Although recessions then were often preceded by an inversion in the yield curve, not all were. In 1850 and in 1892-93 real GDP fell without a prior inversion.

All this corroborates the theory that, at times of low inflation, the yield curve is no longer an infallible indicator.

Of course, none of this is to say that a recession is coming. In a sense, it's worse than that. What has for years been our best guide to the probability of a recession might no longer be as reliable as it once was. We should therefore get used to the nasty thought that recessions are unpredictable - which means that equities are not just risky, but uncertain.