"Bettors follow momentum signals" concludes the University of Chicago's Tobias Moskowitz in a new paper. He studied thousands of bets on four different American sports and found a pattern. Investors back teams that have done well recently, with the result that prices of bets on those teams eventually rise too much. This generates profits for early backers who sell their bets before the game, but losses for those who buy overpriced bets just before the match.

You might wonder why you should care about gambling on American ball games. Simple. There are countless possible anomalies in financial markets, which means that if you look hard enough you'll see all sorts of patterns that might enable you to make money. The problem is, though, that these might be just one-off statistical artefacts that cannot be relied upon to persist. Campbell Harvey of Duke University warns: "Most claimed research findings in financial economics are likely false."

To overcome this problem we need to see a pattern not just in one time and place, but in others. The finding must be replicated in other data sets. And this is what Professor Moskowitz's research does. The fact that momentum exists in betting markets increases the likelihood that momentum is a reliable fact about financial behaviour.

Momentum beats the market

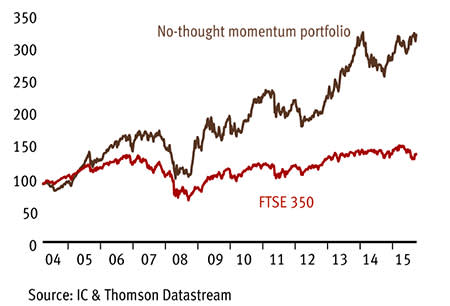

This is especially the case because this piece of evidence adds to plenty of others. The original discovery by Narasimhan Jegadeesh and Sheridan Titman of momentum in US equities has been corroborated by researchers at AQR Capital Management. The performance of our own no-thought momentum portfolio suggests the same thing happens in UK equities. Lucio Sarno at Cass Business School and colleagues have found momentum in currency markets. The LSE's Victoria Dobrynskaya has found momentum in international stock markets. AQR's Cliff Asness has found it in commodities. Eric Ghysels at the University of North Carolina has found it in UK and US stock markets in the 19th century. And Yale University's Will Goetzmann says it existed in the stock market in Tsarist Russia.

Momentum, therefore, is almost ubiquitous: it appears almost everywhere that researchers look. This could be because it arises not from egregious stupidity but from what is in fact reasonable but slightly mistaken behaviour.

There are two processes at work here.

The first is underreaction; if an asset gets some good news, this isn't fully and immediately embedded into prices, but instead prices drift up gradually later.

Underreaction, though, can be reasonable. Our prior beliefs are (or should be!) based upon sound evidence and theory and there are always reasons to be sceptical about new facts, not least because a lot of developments in financial markets are noise rather than signal. Such scepticism, however, can be overdone. Where it is, momentum will occur.

The second process is overreaction; once a price has risen, others buy it, causing its price to rise too far.

One reason for this overreaction lies in simple overconfidence. Investors who had bought the share before its rise interpret their profits as vindication of their stock-picking skill - which emboldens them to buy even more, thus pushing its price up further.

There can, though, be a second reason. Imagine you are in a strange town and want something to eat. You see two restaurants, one empty and the other bustling. Which do you choose? You might well go for the busier one, in the belief that the locals must know something. This is the heuristic of social proof. The same thing can apply to financial assets: sometimes, people buy them because they believe others know something.

But here's the problem. Those diners in the busy restaurant might not be knowledgeable locals but other strangers, some of whom wandered in simply because others did so before them. A bad restaurant might then be thriving because the blind have led the blind. In the same way, Harvard University's Andrei Schleifer and Brock Mendel have shown that bad assets can sometimes become overpriced as rational but uninformed investors chase noise.

Perhaps, therefore, momentum is so common because it arises from reasonable behaviour - even though such behaviour can be mistaken.

This doesn't, of course, mean that momentum investing is a foolproof way of making money. Nothing is. There's a risk that, sometimes, the momentum investor will buy assets that have risen too much. Nevertheless, the sheer weight of evidence in favour of momentum effects is impressive.