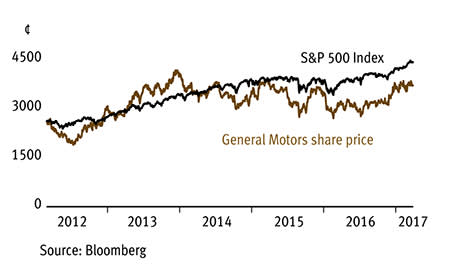

A deal to shift General Motors (US:GM) persistently loss-making European business has served to highlight the investment case for an American corporate icon, albeit an American corporate icon that filed for reorganisation under Chapter 11 bankruptcy proceedings seven years ago.

- Sale of loss-making Opel and Vauxhall brands

- Prioritised shareholder returns

- Focus on margin expansion

- Removal of European risk factors

- Possible cyclical peak in US sales

- Stalled institutional support

While some investors were disappointed by the terms of GM's deal rid itself of the millstone that was its European business, we believe the focus the disposal gives the group on the exciting US truck market and China make the lowly-rated shares look compelling.

France's state-controlled automaker Peugeot promised to pay $1.4bn (£1.15bn) for GM's loss-making Opel and Vauxhall brands. The US car giant's European financial operations are also to be jointly acquired by Peugeot and French bank BNP Paribas SA for about $950m. GM is to retain $6.5bn of underfunded pension liabilities and take a one-off $4bn charge. The group's total underfunded pension hole at the end of 2016 stood at $18.3bn.

The disposal of the European operation, which followed several turnaround attempts, has generally been viewed as favourable for GM which has learned the hard way that bigger is not always better. On the one hand, the sale removes non-performing assets and eliminates future cash outflows associated with the business, which broker JPMorgan estimates at $3.8bn. At a stroke, the Opel and Vauxhall sale also effectively reduces risk factors linked to the UK's withdrawal from the European Union, together with any knock-on effects from the European diesel emissions scandal. GM executives might also have factored the lingering financial uncertainties in the eurozone when considering the deal.

Perhaps most significantly, though, the move simplifies the business model, thereby enabling GM's management to direct their efforts to growth areas of the business and leading-edge developments, such as the rollout of the Maven car-sharing programme, a metropolitan-based service in which GM vehicles are rented by the hour. The group is also investing heavily in driverless and electric/hybrid vehicle technologies.

GM has been focusing on driving up sales into the higher-margin US retail market at the expense of its fleet sales. This is borne out by a marked fall-away in sales to the US hire car industry, which, although more predictable in down-legs of the cycle, has traditionally delivered relatively thin margins. GM retail sales were up 4.9 per cent in February, against a 1.7 per cent increase in fleet numbers, while a vehicle sales mix weighted towards SUVs and pick-up trucks fed into the operating margin. GM's market share in the US retail market is on the rise, even as it looks to expand unit profitability; a process augmented by a four-year plan designed to create $5.5bn in cost efficiencies by 2018.

Another key focus for GM is China, where the car maker has had a presence since the mid-1990s. Last year, it shifted 3.9m vehicles, a record in potentially the world's largest car market, as well-heeled locals clamoured for iconic US marques such as Chevrolet, Buick and Cadillac. Whichever way you cut it, the potential long-term opportunity in the People's Republic dwarfs anything on offer in the sclerotic European economy

One of the corporate world's biggest share buyback programmes is also helping push EPS forwards (as reflected by the rising EPS number in our table despite declining profits). The group returned $4.8bn last year through dividends and a $2.5bn share buyback and JPMorgan has pencilled in buybacks of $4bn this year, followed by $3bn in 2018. Cash from the European disposal should support capital return prospects.

| GENERAL MOTORS (US:GM) | ||||

|---|---|---|---|---|

| ORD PRICE: | 3,683¢ | MARKET VALUE: | $55.2bn | |

| TOUCH: | 3,672¢-3,753¢ | 12-MONTH HIGH: | 3,855¢ | LOW: 2,734¢ |

| FORWARD DIVIDEND YIELD: | 4.3% | FORWARD PE RATIO: | 6 | |

| NET ASSET VALUE: | 2,926¢* | NET CASH: | $1.7bn** | |

| Year to 31 Dec | Turnover ($bn) | Pre-tax profit ($bn) | Earnings per share (¢) | Dividend per share (¢) |

|---|---|---|---|---|

| 2014 | 151 | 4.24 | 304 | 120 |

| 2015 | 152 | 8.42 | 503 | 138 |

| 2016 | 166 | 9.81 | 612 | 152 |

| 2017* | 147 | 9.79 | 640 | 160 |

| 2018* | 144 | 9.51 | 650 | 160 |

| % change | -3 | -3 | +2 | - |

Normal market size: Matched bargain trading Beta: 1.35 *Includes intangible assets of $6.26bn, or 418¢ a share **Excludes GM Financial, restricted cash of $530m and marketable securities of $11.8bn ***JPMorgan Cazenove forecasts, adjusted PTP and EPS numbers | ||||