- A disappointing 3 months for Blue Chip Momentum

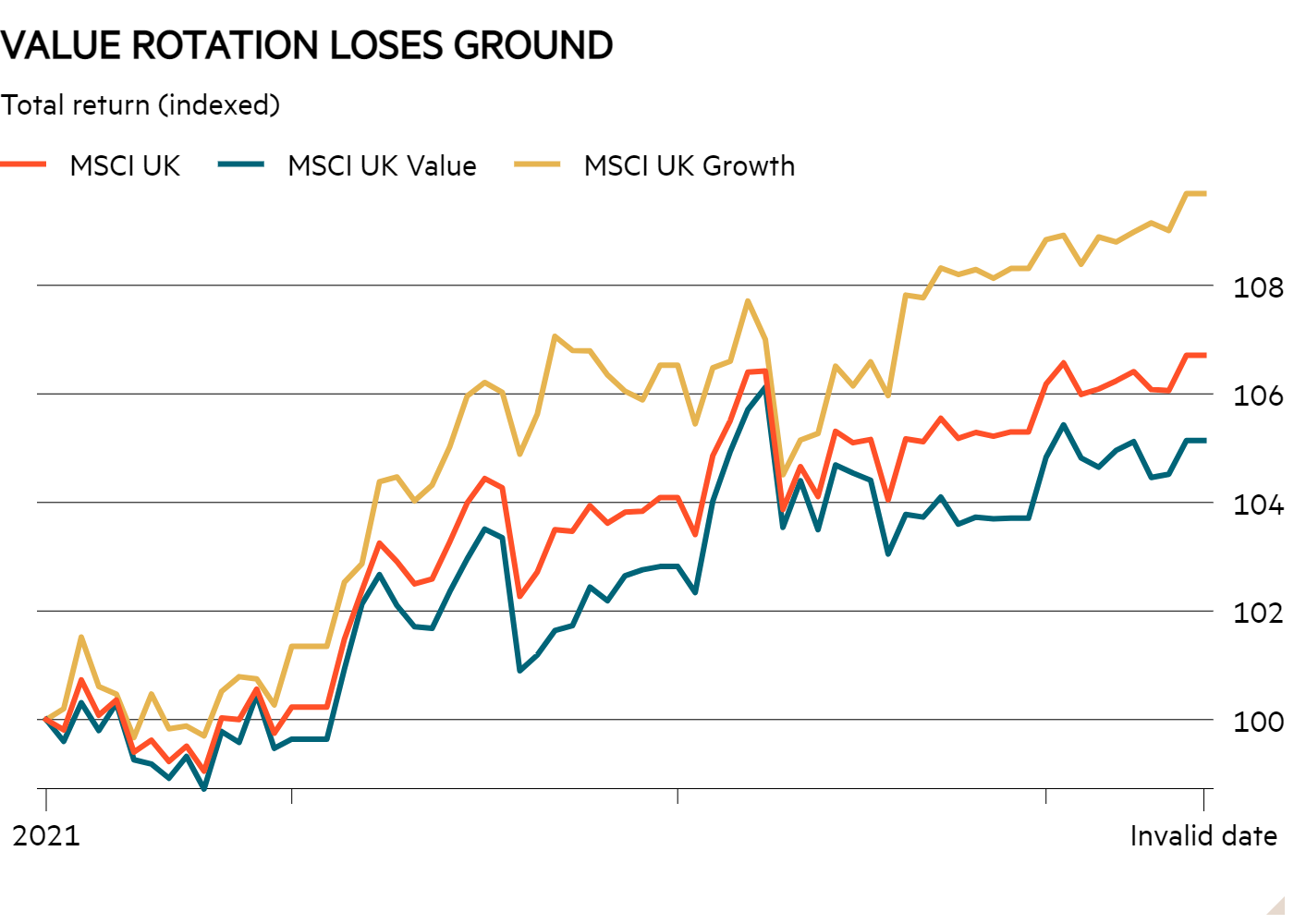

- Is the value rotation still on?

- Long-term performance underlines the power of momentum

- 10 new Longs and Shorts for the coming three months

While there has been no lack of headlines about the value revival, in the past three months it seems to have lost a bit of steam. Indeed, despite all the bluster, the MSCI UK Value index has produced a 5.1 per cent total return over the past quarter compared with 6.7 per cent from the MSCI UK index and 9.7 per cent from UK Growth.

This faltering of the value trend has shown up in the performance of my Blue Chip Momentum screen over the past three months. Many of the screen’s Long picks had their colours pegged firmly to the mast of 'value'.

The value rotation may just be pausing for breath. However, despite the many excited suggestions that there’s plenty more gas in the tank, it is also possible that the trend is all out of steam after a terrific run since November. Indeed, the UK Value index has returned 39.1 per cent over that time compared with 32.3 per cent from the main UK index.

For momentum strategies, times are often less risky when style trends are not too strongly pronounced. That’s because very dominant investment themes can create big performance whipsaws when sentiment changes.

While there is still a definite value flavour to the Long picks this month, in general the 10-stock selection seems more mixed than last time. The selection process is simply based on picking the 10 best (Longs) and worst (Shorts) performing shares of the previous three months.

On aggregate, over the past three months the Longs and Shorts produced the opposite performance to what one would hope for. The Longs slightly underperformed the FTSE 100 index and the Shorts outperformed.

| 3-month performance | |||

|---|---|---|---|

| SHARE PRICE RETURNS (15 Mar - 11 Jun 2021) | |||

| LONGS | SHORTS | ||

| International Consolidated Airlines Group SA | -6.6% | Fresnillo PLC | -9.6% |

| Entain PLC | 21% | London Stock Exchange Group plc | 2.2% |

| Ashtead Group plc | 19% | Rightmove plc | 16% |

| Johnson Matthey Plc | 0.4% | Experian PLC | 12% |

| Barclays PLC | 0.1% | Avast Plc | 6.3% |

| Anglo American plc | 5.4% | Bunzl plc | 2.9% |

| Antofagasta plc | -12% | Hikma Pharmaceuticals Plc | 10% |

| Pearson PLC | 6.2% | Imperial Brands PLC | 13% |

| Barratt Developments PLC | -2.3% | Polymetal International Plc | 11% |

| Aviva plc | 6.7% | Unilever PLC | 7.6% |

| Longs | 3.7% | Shorts | 7.1% |

| FTSE 100 | 5.7% | FTSE 100 | 5.7% |

| Source: FactSet | |||

The performance monitoring of this screen is rather unrealistic (it is the only screen I monitor in this way). The purpose of the blue-chip momentum screen is mainly about seeing this amazingly powerful phenomenon in action, as well as providing ideas that could be worth further research. The flaws in the performance figures are that they take no account of dividends paid or notional costs of operating the strategy. From that perspective, it is particularly worth noting that it is commonly assumed that dealing costs from frequent reshuffles would be enough to offset the benefit of a pure momentum strategy.

Still, the long-term data I’ve amassed over the years does a good job in illustrating that momentum is something that’s worth paying attention to. There are also many other far more rigorous studies into momentum that tell similar stories.

| Long-term performance | |||

|---|---|---|---|

| Long | Short | FTSE 100 | |

| Since June 2007 | 194% | -7% | 4.1% |

| 10-yr | 111% | -1.7% | 22% |

| 5-yr | 67% | 8.1% | 19% |

| 3-yr | 13% | -26% | -6.6% |

| 1-yr | 39% | 30% | 18% |

| Source: Thomson Datastream/S&P CapitalIQ/FacSet | |||

Due to publishing deadlines, the Long and Short picks in the accompanying table below do not quite reflect the official momentum-monitoring period used by this screen. When I next update the screen the performance recorded will be based on the official selection of Longs and Shorts based on three-month performance to 15 June.

Full details of the Long and Short portfolios can be found at the end of this article and I’ve also taken a closer look at the top three Longs (the three best-performing FTSE 100 shares over the quarter).

BT

The share price of UK telecoms behemoth BT (BT.A) has gone stratospheric over the past three months. Following a dire 2020, in which the company cut its dividend and saw its share price plummet to multi-year lows, the company has benefited from several pieces of positive news.

Philip Jansen, a turnaround specialist appointed as chief executive at the start of 2019, is focusing his sights on building out the group’s fibre network “like fury”. Investors have warmed to the strategy. Enthusiasm has been bolstered by news that the company will be able to earn unregulated returns from the network while also benefiting from the super-deduction capital investment tax break which chancellor Rishi Sunak introduced to stimulate a post-Covid recovery.

Other positive news over the past three months includes a better than expected outcome to BT’s triennial pension review. This has helped calm nerves about the massive and cash-hungry pension scheme, which has an £8bn deficit.

Lower-than-expected 5G spectrum costs also helped sentiment, as has a decision to reintroduce a dividend. The group’s plans to pull back from its involvement in sports broadcasting has also met with a positive response from the market given the huge costs of sports rights.

There has been excitement on BT’s shareholder register, too. French-Israeli billionaire Patrick Drahi has emerged with a 12 per cent stake in the company through his telecoms group Altice. This makes Altice BT’s joint-largest shareholder alongside Deutsche Telekom (DAX:DTE). Drahi has said he is not interested in launching a bid for BT but believes there are exciting opportunities for fibre roll-out.

However, as well as BT’s plaudits, a number of analysts have become increasingly skeptical on the company’s prospects following the recent share price run.

The chief cause for concern is the prospect of rising competition as capital is poured into fibre provision. The threat not only comes from the other major player in the sector, Virgin Media. There is a growing fear that smaller fibre players will band together to create a more credible challenge, including to BT’s wholesale business. There is also the prospect that the 5G network could help these operators offer more comprehensive packages to customers. Meanwhile, BT’s balance sheet still looks stretched.

Entain

This is the second quarter in a row that Entain (ENT) has been among the top three blue-chip momentum picks. The international, online-focused gambling company owns the Ladbrokes betting chain in the UK and was formerly named GVC.

Entain’s shares have actually defied the odds to clock up strong gains over the past three months.

A significant cause of investor excitement centres on the company’s exposure to the rapidly deregulating US market through its 50 per cent owned BetMGM joint venture (JV). But over the past three months, as a group, listed US online gambling companies have lost about a fifth of their value. This reflects the market’s reaction to a number of events that suggest deregulation may be slower than anticipated, profitability may be lower than hoped and the ultimate size of the market may be smaller than many expect.

For its part, Entain’s JV has been expecting to capture about 20-25 per cent of a market worth around $30bn. It’s guidance has been for Ebitda margins in the region of 30-35 per cent after a 2-to-3-year payback period on customer acquisition costs.

But while the group’s forecasts may need to be revisited at some point, there has also been good news coming from across the pond for Entain over the past three months. Indeed, after a slow start, BetMGM seems to now be making impressive progress. It is winning share in established markets and taking a leading position in newly opened markets such as Michigan. This has made its market share expectations look very credible.

It’s not only the US where the group is making good progress. It is trading strongly in most of its other territories including its largest, the UK, which accounts for 35 per cent of the group. Investors are also warming to the group’s move towards operating only in regulated markets, which provide more certainty.

Regulation is a double-edged sword, though. As well as the recent perceived disappointment in the US, new German regulation is impacting trading there and the group could be affected by an ongoing review of the UK’s gambling regulations.

Despite the strong share price performance this year, there are reasons to think the shares may still offer some value. Based on assumptions of a forecast total addressable US market of $20bn, broker Numis reckons Entain’s current share price sits about a fifth below a fair sum-of-the-parts valuation. It also calculates that based on BetMGM winning a 20 per cent share of the US market, the venture is currently being valued at just over 8.5 times its 2027 cash profits. That looks low compared with rival FanDuel – 95 per cent owned by Flutter (FLTR) – that Numis estimates is valued at 14.7 times.

Intermediate Capital Group

Expectation-beating half-year results this month helped put a rocket under shares in Intermediate Capital (ICP), a fund manager specialising in credit, real estate and private equity. While the group’s owned investments performed well, it was its ability to attract other investors into its fund launches that really stood out. In what had been billed as a quiet year, Intermediate raised $10.6bn of new funds and finished the 12 months to the end of March with almost $60bn under management.

The success has got the company’s management thinking about what the future may hold. Guidance for fundraising over the next four years has been reset upwards to $40bn. At least $7bn of inflow is expected in each of those years. The company also produced good returns for its clients and generated expectation-beating performance fees.

Like most fund managers, the cost base is relatively fixed, so growth in assets under management tends to have an outsized benefit on profit. Another benefit of Intermediate’s model is that the specialist and illiquid nature of the investments it sources means it generally operates closed-end funds. This minimises the risk of money suddenly flowing out at times of market stress and also helps protect margins.

Long-term prospects look encouraging, too. Since the credit crunch there has been huge institutional interest in the kind of non-bank finance that the company specialises in. The low returns from traditional bonds have made the area particularly attractive and pension funds, sovereign wealth funds and insurance companies appear to continue to hanker for this kind of alternative asset exposure. Covid blip aside, the record for earnings upgrades over recent years stand as testament to these attractions.

| THE LONGS | ||||||

|---|---|---|---|---|---|---|

| Name | TIDM | Price | Market Cap | 3mth Mom* | NTM PE | DY |

| BT Group plc | BT.A | 192p | £19.0bn | 38.4% | 10 | - |

| Entain PLC | ENT | 1,803p | £10.6bn | 20.6% | 27 | - |

| Intermediate Capital Group plc | ICP | 2,289p | £6.7bn | 20.3% | 21 | 2.4% |

| AstraZeneca PLC | AZN | 8,340p | £109.5bn | 19.5% | 19 | 2.5% |

| Halma plc | HLMA | 2,735p | £10.4bn | 19.5% | 43 | 0.6% |

| Ashtead Group plc | AHT | 5,024p | £22.5bn | 18.6% | 27 | 0.8% |

| SEGRO plc | SGRO | 1,081p | £13.0bn | 18.5% | 37 | 2.0% |

| Lloyds Banking Group plc | LLOY | 48p | £34.3bn | 17.7% | 8 | 1.2% |

| Smurfit Kappa Group Plc | SKG | 3,895p | £10.1bn | 17.4% | 17 | 4.5% |

| Royal Mail plc | RMG | 590p | £5.9bn | 17.2% | 10 | 1.7% |

| AVERAGE | - | - | - | 20.8% | 22 | 2.0% |

| THE SHORTS | ||||||

|---|---|---|---|---|---|---|

| Name | TIDM | Price | Market Cap | 3mth Mom* | NTM PE | DY |

| Flutter Entertainment Plc | FLTR | 13,900p | £24.4bn | -17.6% | 38 | - |

| Antofagasta plc | ANTO | 1,529p | £15.1bn | -11.9% | 15 | 2.6% |

| Just Eat Takeaway.com N.V. | JET | 6,491p | £9.7bn | -11.6% | - | - |

| Fresnillo PLC | FRES | 861p | £6.3bn | -9.6% | 14 | 2.2% |

| Renishaw plc | RSW | 5,380p | £3.9bn | -9.6% | 35 | 0.3% |

| Ocado Group PLC | OCDO | 1,921p | £14.4bn | -9.1% | - | - |

| Royal Dutch Shell Plc Class B | RDSB | 1,360p | £108.6bn | -8.5% | 9 | 3.6% |

| Taylor Wimpey plc | TW | 166p | £6.1bn | -8.4% | 10 | 2.5% |

| Royal Dutch Shell Plc Class A | RDSA | 1,420p | £108.6bn | -8.4% | 9 | 3.5% |

| International Consolidated Airlines Group SA | IAG | 203p | £10.1bn | -6.6% | - | - |

| AVERAGE | - | - | - | -10.5% | 19 | 2.4% |

| Source: FactSet | ||||||