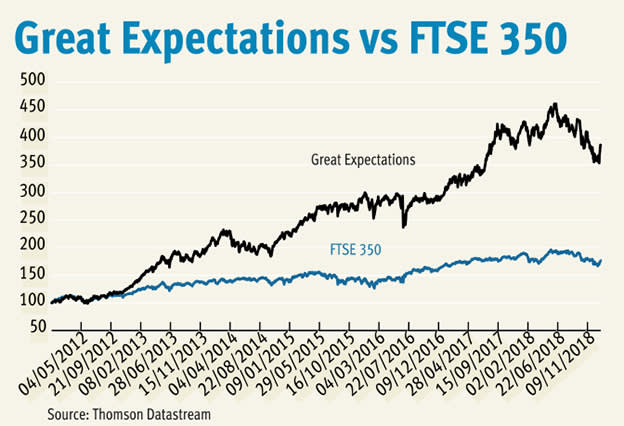

What a difference a week can make. My Great Expectations screen has been a real high flier since I started running it for this column in late 2011. However, when I conducted my stock screen review for the previous issue of this magazine it was having a terrible 12 months with a negative total return of 17.7 per cent compared with a negative 10.7 per cent from the FTSE 350. Fast forward a week, and the 12-month performance, while still disappointing, is better described as poor relative to the market than terrible: a negative total return of 9.9 per cent compared with a negative 7.2 per cent from the index.

2018 performance

| Name | TIDM | Total return (15 Jan 2018 - 10 Jan 2019) |

| Evraz | EVR | 55% |

| Spirax-Sarco | SPX | 16% |

| Anglo American | AAL | 6% |

| Victrex | VCT | -6% |

| Vesuvius | VSVS | -6% |

| Intermediate Capital | ICP | -9% |

| InterContinental Hotels | IHG | -9% |

| ComputaCenter | CCC | -10% |

| Persimmon | PSN | -12% |

| Redrow | RDW | -13% |

| Ibstock | IBST | -13% |

| Antofagasta | ANTO | -16% |

| Bellway | BWY | -19% |

| Renishaw | RSW | -21% |

| B&M European Value Retail | BME | -24% |

| Glencore | GLEN | -25% |

| Ferrexpo | FXPO | -29% |

| Kaz Minerals | KAZ | -43% |

| FTSE 350 | - | -7.2% |

| Great Expectations | - | -9.9% |

Source: Thomson Datastream

The Great Expectations screen focuses on share price and forecast earnings momentum (upgrades to forecasts as well as forecast growth). As such, it is not too surprising that the stocks highlighted by the screen have been so sensitive to the bounce-back experienced by markets over the past week.

Since I started monitoring the strategy seven years ago, it has performed very well overall against a backdrop of a generally bullish market. The cumulative total return since I started to run the screen stands at 287 per cent compared with 77 per cent from the FTSE 350, which is the index the stocks are chosen from. If I apply an annual 1 per cent charge to account for dealing costs the cumulative return drops to 261 per cent.

But despite the strong track record, the screen looks to me like one that could come a cropper in bear market conditions. Last year’s performance may have given a flavour of this risk. The screen has had one truly awful year relative to the market since I’ve run it, which was in 2016 (a 4.8 per cent total return versus 24.5 per cent from the FTSE 350). However, that outcome was chiefly a reflection of the fact the screen missed out on a stellar recovery in the resources sector, which turbo-charged the resources-heavy UK index during the 12 months, as opposed to a broad bear market.

The difficulties this screen faces in tough markets are also reflected in the scarcity of positive results this year. While the screen looks for share price momentum that is strong relative to the index, its requirements for forecast upgrades and forecast growth are based on absolutes (10 per cent-plus forecast growth and forecast upgrades of 10 per cent or more). This makes it tough for the screen to find positive results during times of heightened uncertainty. Indeed, only one stock meets all the screen’s criteria this year.

In past years when stocks passing all the tests have been few, I’ve resorted to including shares that have failed one of the screen’s tests as long as it is not the key upgrade test. This year, to bulk up numbers, I’m having to highlight stocks that have failed up to two tests, as long as neither is the key upgrade test. Even then, I only end up with six stock ideas. The screening criteria are:

■ EPS forecasts for next financial year upgraded by at least 10 per cent over the preceding 12 months.

■ EPS forecasts for the financial year after next upgraded by at least 10 per cent over the preceding 12 months.

■ EPS growth of 10 per cent or more forecast for the next financial year.

■ EPS growth of 10 per cent or more forecast for the financial year after next.

■ Share price momentum at least double that of the market over the past year.

■ Share price momentum better than the market over six months.

■ Share price momentum better than the market over three months.

■ Share price momentum better than the market over one month.

The six stocks passing the screen can be found in the table below. Of note is the fact that two of the stocks passing on the weakest criteria (failing two tests) are among the most heavily shorted on the market according to Castellian Capital’s short tracker – at the time of writing the tracker lists Plus 500 as most shorted and Anglo American as ninth most shorted. The risks associated with backing heavily shorted shares is a reminder of why the screens this column follows are regarded primarily of interest as a source of ideas for further research rather than off-the-shelf portfolios. Given only one share passes all the screen’s tests – Spirent Communications – I’ve focused my write-up below solely on it.

2019 shares

| Name | TIDM | Market cap | P | Fwd NTM PE | Av 12mth EPS Upgrade | DY | Fwd EPS grth FY+1 | Fwd EPS grth FY+2 | 12mth chg Fwd EPS FY+1 | 12mth chg Fwd EPS FY+2 | 3-mth momentum | Net cash/debt (-) | No. tests failed | Tests failed |

| Spirent Communications | SPT | £747m | 122p | 17 | 19% | 2.6% | 28% | 10% | 13% | 25% | 1.7% | $95m | 0 | na |

| JD Sports Fashion | JD. | £3.9bn | 396p | 14 | 12% | 0.4% | 9.1% | 11% | 11% | 13% | 1.0% | -£85m | 1 | />10% EPSgrth FY+1/ |

| 3i Infrastructure | 3IN | £2.2bn | 267p | 13 | 20% | 3.2% | -56% | -13% | 15% | 25% | 7.6% | £123m | 2 | />10% EPSgrth FY+1/>10% EPSgrth FY+2/ |

| SSP | SSPG | £3.2bn | 692p | 25 | 17% | 1.5% | 12% | 8.2% | 16% | 18% | 3.0% | -£343m | 2 | />10% EPSgrth FY+2/1yrMom/ |

| Anglo American | AAL | £23bn | 1,815p | 10 | 29% | 4.6% | -7.5% | 2.0% | 30% | 28% | 6.4% | -$3.4bn | 2 | />10% EPSgrth FY+1/>10% EPSgrth FY+2/ |

| Plus500 | PLUS | £1.7bn | 1,484p | 7 | 66% | 15% | 88% | -31% | 96% | 35% | 12% | $512m | 2 | />10% EPSgrth FY+2/6mthMom/ |

| EVRAZ | EVR | £7.0bn | 484p | 5 | 87% | 9.7% | 176% | -35% | 148% | 26% | -8.3% | -$3.8bn | 2 | />10% EPSgrth FY+2/3mthMom/ |

Source: S&P CapitalIQ

Spirent Communications*

Following several tough years, the stars seem to be aligning for telecoms testing company Spirent Communications (SPT). Industry enthusiasm for the imminent roll-out of 5G (faster mobile data) as well as the adoption of faster ethernet technology has caused a pick-up in trading at the same time as demand is building for two recently developed products: VisionWorks and cyber security testing. Furthermore, the group has a strong cash position, margins are rising, the valuation looks unchallenging and there’s takeover potential.

Over recent years, the real thorn in Spirent’s side has been its “connected devices” division, which tests the chipsets of mobile phone handset companies. This business has gone from contributing 30 per cent of group revenue in 2014 to 19 per cent in 2017. Demand dwindled as US and European handset developers, such as Nokia, Motorola and Erikson, lost market share. Meanwhile, the manufacturers in China and Korea that have taken share tend to source pre-tested chipsets from a shrinking number of big suppliers. The challenges faced by Spirent’s connected devices business have been compounded by the fact it is not the market leader, which has made it more vulnerable to the changes.

However, after the division fell into loss in 2016, Spirent took tough action, booking a $69m (£50m at the time) impairment charge and fiercely cutting costs. In 2017, connected devices returned to the black and contributed 8 per cent of operating profit with an underlying margin of 6.1 per cent. Still the group-wide underlying operating margin of 13 per cent remains well below the 2012 peak of 25 per cent (see chart below). Importantly, management believes connected devices has now been stabilised. What’s more, the division is benefiting from 5G-related work, which means it may even become the source of some modest positive surprises. The restructuring and improved backdrop may provide Spirent with a chance to dispose of the operation, which may well be positively received by investors given the uninspiring long-term outlook.

Technological changes are also having a positive impact on Spirent’s largest division, Network and Security, which accounted for 57 per cent of 2017 sales and 65 per cent of profits. For a few years, orders for ethernet testing have been lacklustre as customers have mulled the move from 100G to faster 400G technology. Finally, 400G is being enthusiastically adopted and orders are rolling in. Typically, such cycles last for about two years before abating.

The network and security division’s second half should also benefit from a pick-up in orders from the Asia-Pacific region (35 per cent of 2017 sales) following a resolution to issues related to the China/US trade war – specifically a temporary US ban on doing business with Chinese company ZTE. At the time of its third-quarter update Spirent said there had been a release of pent-up demand from China. Nevertheless, further negative developments from the ongoing trade war represent a major risk, in particular recent signs of US hostility towards Spirent customer Huawei. “Huawei is a 200lb gorilla,” says Liberum analyst Janardan Menon. “ZTE is a mouse compared with Huawei.”

The network and security division should also benefit from Spirent’s investment over recent years in its cyber security product. This tests customers’ security systems by bombarding them with malicious traffic. While this product faces competition from a similar product developed by rival Keyside, Spirent’s other newish offering, Visionworks, is currently the only one of its kind. Visionworks, accounts for about half of the Lifecycle Service Assurance division (the division as a whole is about a quarter of total sales) and is the only 'active' network testing system on the market. It allows networks to pre-empt problems rather than respond to them only after they’ve occurred. This should reduce clients’ costs and improve service levels. Orders are lumpy and the order process can take between 18 and 24 months to come to commercial fruition. But the level of uptake from big telecoms companies is beginning to look encouraging.

So following several testing years, the investment case for Spirent holds some genuine allure. This was underlined by the confidence expressed in a third-quarter trading update in November. A lot rides on the group’s final quarter when it typically generates about two-fifths of profit, so it was of note that management felt bold enough to say the group would “at least” hit expectations. The indication is that more upgrades could be on the cards when the company next reports (likely to be a full-year results announcement in early March). Indeed, the main reason for Spirent being highlighted by the screen is the upgrades that followed publication of the 2017 results, reflecting the significance of the final quarter of the year and its ability to hold surprises (see chart).

Upgrade potential (also downgrade potential) is enhanced by the fact that a relatively low fixed cost base means rising sales have a big impact on the bottom line. If things go well, there are grounds to hope underlying operating margins could rise faster than forecast. Over time there is potential for margins to head back up towards the 20 per cent level compared with 13 per cent in 2017 and 14.9 per cent forecast by broker Liberum for 2018.

Solid cash generation also means there is the possibility the group may pay out another special dividend following on from the 5¢ special payment last year. The company could also use cash to go on the acquisition trail, although potentially of more interest is the possibility it could be bid for itself – bid speculation is a recurrent theme. The announcement last November that the current chief executive plans to retire this year could prove a trigger for would-be suitors.

While the screen has picked up on positive share price momentum, Spirent shares have hardly run away. In fact, based on enterprise-value-to-forecast-cash-profits (EV/Fwd Ebitda), the shares are in line with both the 10- and five-year average, suggesting the shares have yet to price in major recovery upside. The cyclical nature of Spirent’s end markets, its lumpy orders and heavy end-of-year weighting to profits are all negative features for potential investors. Meanwhile, potential trade war strife is also a noteworthy risk. That said, after years in the doldrums, there seems a fair bit more to be positive about than there is to be negative about.

*Between the writing and publication of this article Spirent released a trading update to inform the market it expected to "exceed the market's profit expectations for the financial year 2018"